Overview of SAP FICO

Hello everyone! In today’s session, we will learn about the SAP FI module that is FICO module. Now before moving ahead with this, let me give you an overview of what SAP FI module is. SAP FI module has the capability of meeting all the accounting and financial needs of an organization. It is within this module that the financial managers as well as other managers within the business can review the financial position of the company in real time as compared to the legacy systems, that is a third party system, which oftentimes require overnight updates before financial statements can be generated and which are run for the management review.

Thank you for reading this post, don't forget to subscribe!

So for this purpose, SAP FI module was introduced, where it keeps all the records of their financial managers as well as the other managers within their businesses, and they are then compared with their legacy system of the business with the real time management system. Next, we’ll see the course content of this particular session.

First, we’ll see what is financial accounting, that is FI, and next we’ll see controlling, that is, managerial accounting. Now before moving ahead with that, let me give you a brief on the functionality of the SAP FI module.

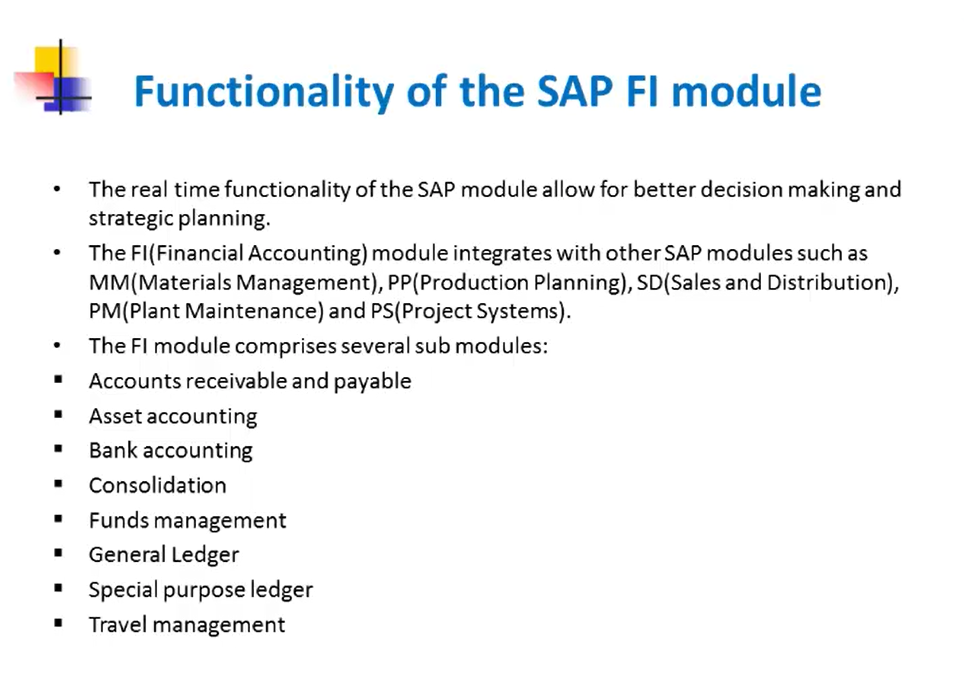

The real time functionality of the SAP module allows for better decision making and strategic planning. Now here, the FI module- that is the financial accounting module- integrates with other SAP modules such as material management, production planning, sales and distribution, plant maintenance, and project systems. So here, this FI module integrates with all the other SAP modules. Now here in SAP FI module, we have several submodules like account receivable and payable, asset accounting, bank accounting, consolidation, funds management, general ledger, special purpose ledger, and travel management. So these are the submodules of the FI module. We’ll see all of these modules in our further slides.

Now first, we’ll see financial accounting. Now let us see what is the content of financial accounting. In this, we’ll see general ledger, then we’ll see balance sheet. Under balance sheet, we’ll come across assets, then liabilities, and we’ll see what are equities. Then we’ll see income statement. Under that, we’ll see about revenues and expenses. So these are the topics which we’ll be covering under financial accounting section.

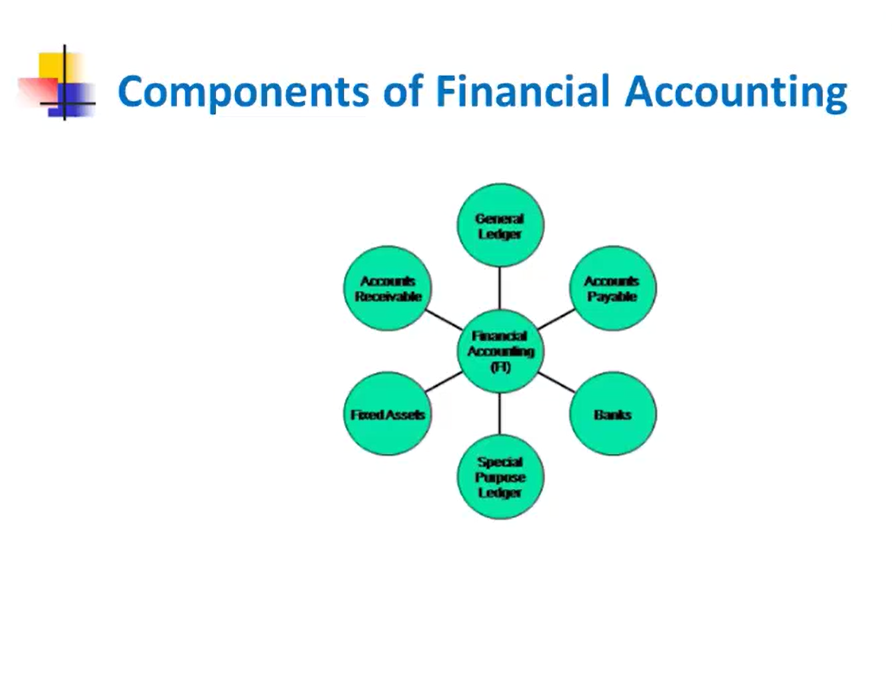

Now first, we’ll see what is financial accounting. Financial accounting is designed to collect all of the data needed to support the preparation of financial statements for external users. So it is a preparation of financial statements for external users. So it collects the data which has the information about the financial records for the external people, that is a third party system. Now in financial accounting, as we know, that will be having components such as general ledger, accounts payable, bank statement, special purpose ledger, fixed assets, accounts receivables.

So these are the submodules under FI, and under financial accounting, we’ll be covering all of these components.

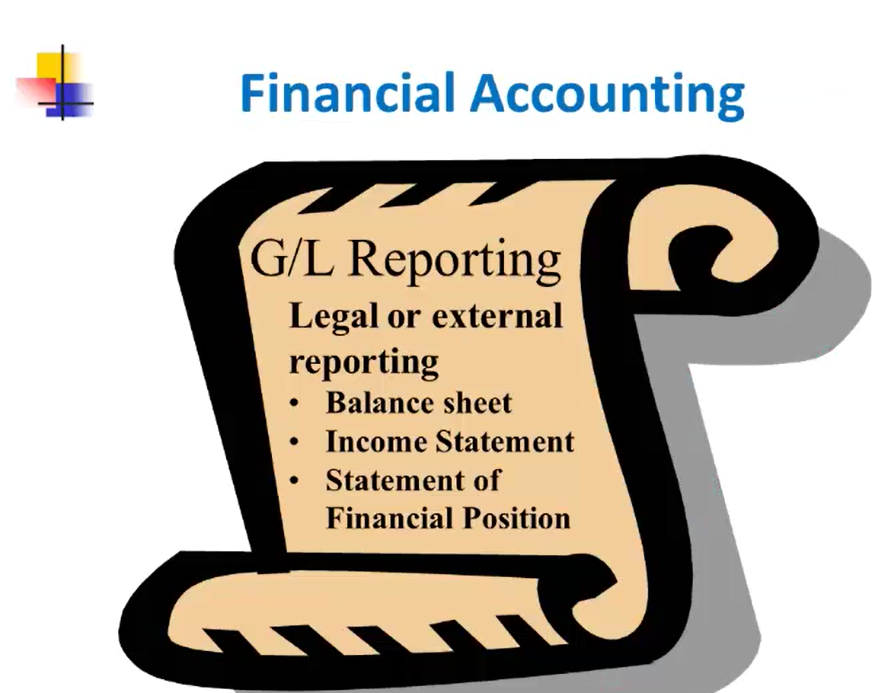

Under financial accounting, we have something called general ledger. Now what is a general ledger? It is a legal or an external reporting. It contains balance sheet, income statement, and statement of the financial position.

So it contains all the records of a particular employee related to their income statement, their balance sheet, their bank details, their financial position, and their external or legal reporting documents. So these things are maintained under G and L reporting that is general ledger reporting.

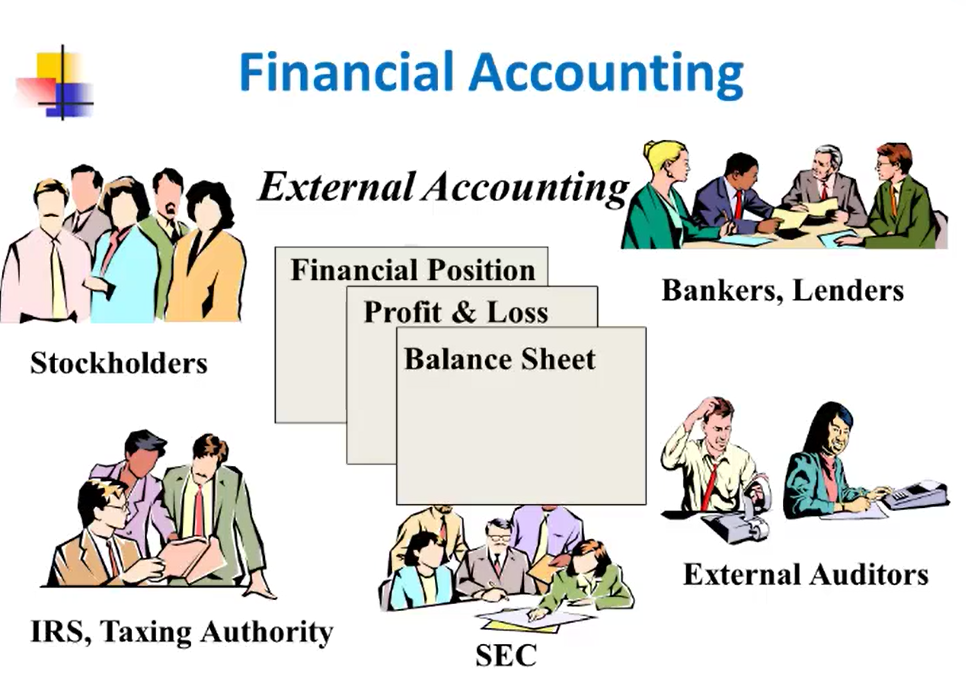

Next, we have external accounting, where we’ll be having external accounting on accounts of financial positions, their profit and loss statements, that is the income statements, and their balance sheet statements.

Now for external accounting, we require some banks and lenders, some stakeholders, some external auditors,and we have some taxing authorities for taxation, and we have a third party system, that is a legacy system or we say a secondary system.

So, in financial accounting, we maintain external accounting on basis of their financial position, their income statement, that is their profit and loss, and their balance sheet. So this graphical view represents the external accounting for a particular business, or we can say a particular company.

Now here, first, we’ll see what is a general ledger for a company. The general ledger provides a complete record of all acceptable business transactions from the viewpoint of an accountant. An acceptable business transaction has the following characteristics. First, it affects the final position of the entity. Second, measurable in a currency. Third, it affects at least two accounts. Fourth, it has a combination of liabilities and equity. So assets is equals to liabilities and equity, and it has debits and credits into its accounts in general ledger. So it provides a complete record of all of these assets, liabilities, and equities, which are acceptable via a business transaction from a viewpoint of an accountant, so this is general ledger.

Next, we have balance sheet. Under balance sheet, we’ll describe assets, liabilities, and equities. First, we’ll see what is a balance sheet. It is a statement containing assets and liabilities of a company prepared at the end of a financial year to show the financial position of the company. Now, once a company has a target to be achieved and they have prepared a memo for that particular target to be achieved, then at the end, they prepare a financial year report to show where the company standards are set or where the company position is set. So at the end, the company prepare a financial report at the financial year end to show the position of the company, that is to show where the company stands in the market. Now here, it contains a combination of assets and liabilities.

Now we’ll see what is asset. Assets are things of value that a company owns or controls that accountants have agreed to measure in monetary terms. Now assets may be cash, accounts receivables, plant and equipment, and the inventory that are the goods required for the company. So these are the assets, as in the things which are required for the company or you can say the assets which are owned by that company.

Next, we have liabilities. What are liability? Things that a company owes or must provide services in order to settle, that accountants have agreed to measure in monetary terms. Now liability means the things that companies owns on their own, or they must provide the services to their accountants. Now it includes accounts payable, notes payable, bonds payable, and unearned revenue. So these are some examples of accounts in liability.

And last, we have equity in balance sheet. Equity is a simple mathematical calculation which gives the difference between the assets and liabilities. Now it includes the monetary amounts collected with respect to all the preferred and common stock transactions, the aggregate net income reported since organization of the company, and a reduction for dividends that have been paid to the stockholders. So equity gives a difference between the assets and the liabilities, and it contains the information about the stock transactions, the aggregate net income of the company, and the dividends that have been paid to the stockholders. So it contains all of these information in a balance sheet, and a sheet is prepared for that company to show where the company position stands at the end of the financial year.

Now last point in financial accounting is income statement, that is the profit and loss statement. So we will see about revenues and expenses. What is an income statement? It is a statement prepared at the end of the financial year providing the expenses occurred and income received for the entire financial year. It means that we prepare a statement at the end of the year, which has the information about the expenses that occurred in the company or the income, that is a profit that the company has gained.

First, we’ll see the revenues that are the incomes. The monetary amounts collected from customers in settlement for goods purchased from our company or services rendered by our firm to them during the current fiscal year. It means that the income that the company has gained or the profit that the company has gained by selling the goods purchased from the company or by providing the services to their firm during the fiscal year, that is the current fiscal year. All those things are calculated from the viewpoint, and an income statement is prepared. So this is for profit statement, that is the revenue.

Now we’ll see the expenses which have been occurred in the company. Expenses means the amounts paid to the vendors in settlement for goods purchased by our company or services rendered to our firm by other companies during the current fiscal year. So the revenues and the expenses together make the income statement for that particular organization and for that particular company.