Asset Accounting 3

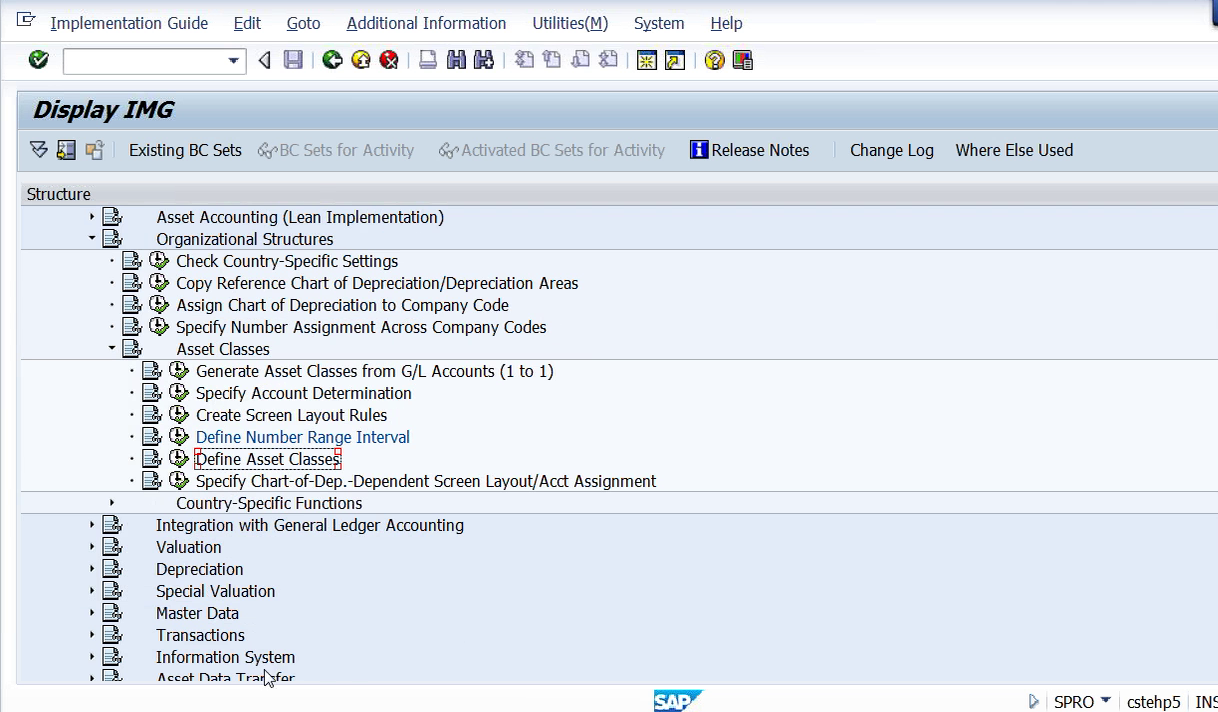

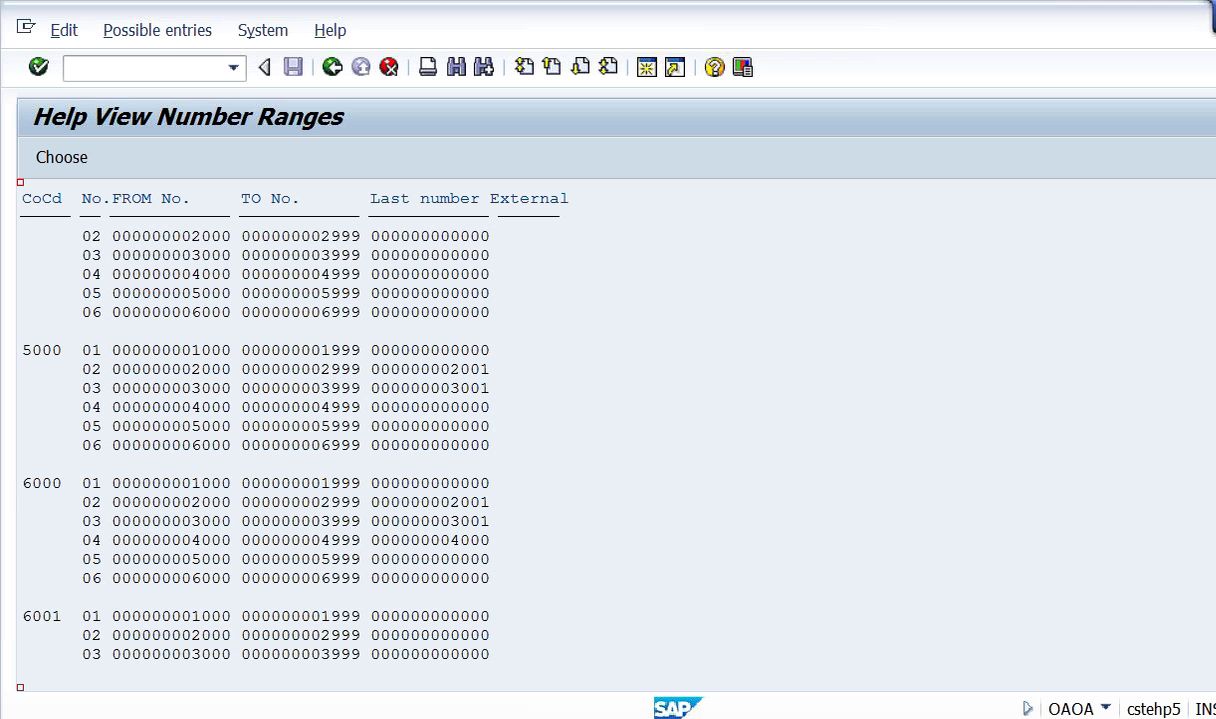

So yesterday, we have created account determination screen layout rules. So DRAUBULA, and select the screen layout tools we have created yesterday. And after creation of screen layout rules, define number range interval. This number range interval is going to be used for the purpose of creating asset master records. For each and every asset master record, we need to have a number. For that purpose, we need to create it. And we have created 1 to 1,000, 1,001 to 2,000, 2,001 to 3,000 and 8,001 to 9,000, this I’m going to use it for the purpose of AUC. And 1,2,3 And when you create, when you do practice, you take 04, 05, 06 because first numbering I want to use for land. This is for buildings. This is for plant and machinery. Like that when you create vehicles, furniture and fixtures, for that also you can create. And, AUC is not a complete asset that’s why I’m just giving the last number right for this. And, then once we complete, now we need to create asset class.

Thank you for reading this post, don't forget to subscribe!

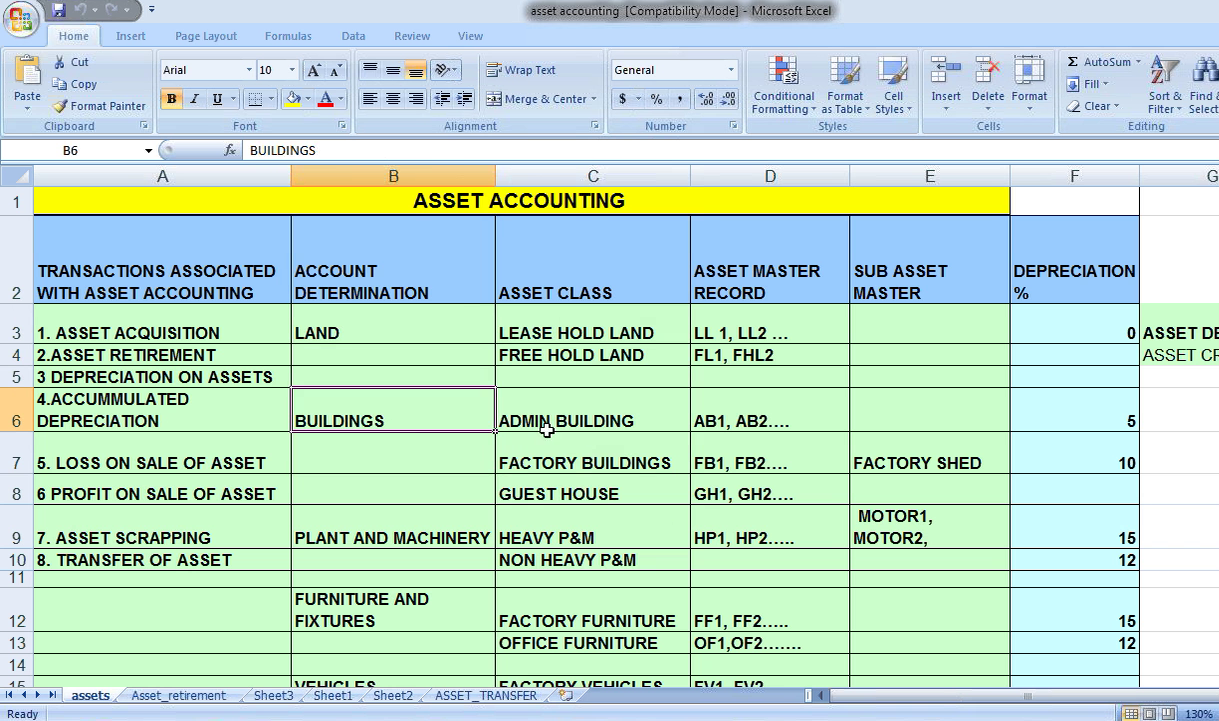

What is meant by asset class? So here, what we have done, see, this is the account determination that we have already created. Then asset class, we are going to create now. So for land, I can say leasehold and freehold.

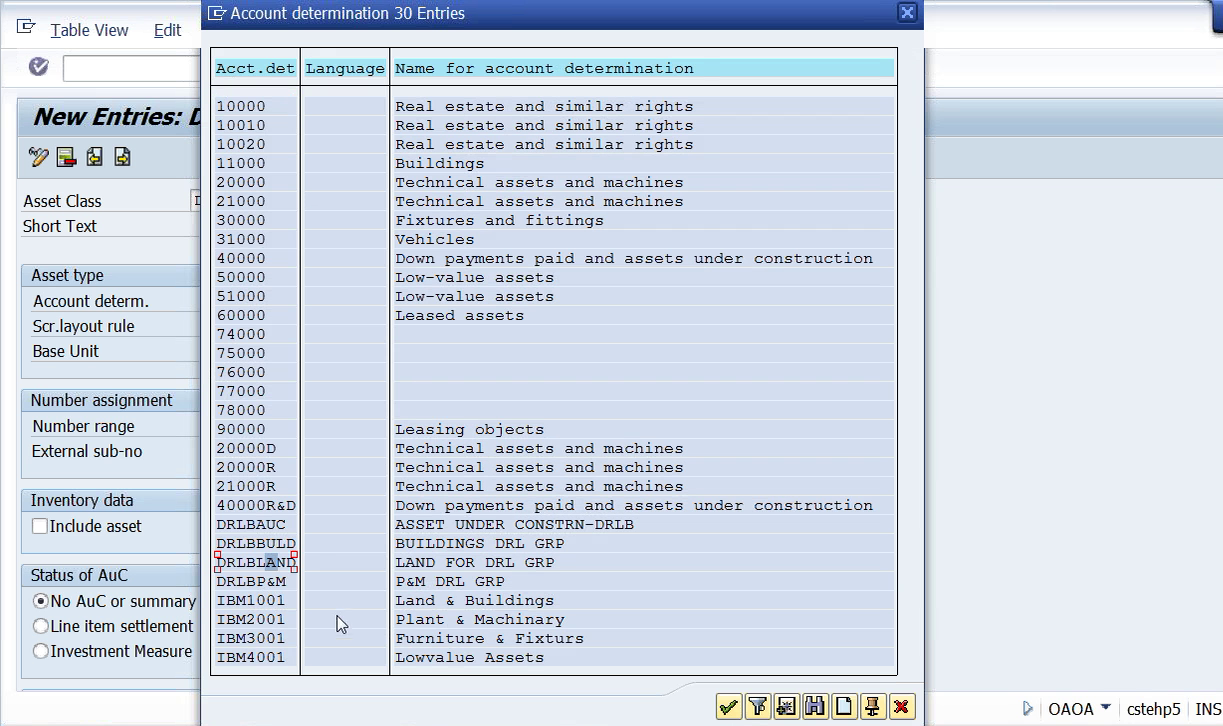

Buildings, admin, factory, guesthouse like this. Plant and machinery, heavy plant and machinery, non heavy plant and machinery. So this is what now I’m going to create. And certain some notes I have given, certain rules and, the things. Here, asset class is defined with reference code determination. Let us see this. So I’m going to define asset class. So asset class, leasehold land, freehold land. Admin, factory, guest house. Like this, these are the asset classes I’m going to define. Go to new entries, and even here, system accepts only 8 digits. So leasehold land. Lease hold land means land taken on lease. So since we are going to take the lease for, say, 50 years, 100 years like that, so we have to show leasehold land in our books of accounts. So this is leasehold land, say DRLB, Asset class, what I do is DRLBLHLA I’m using abbreviation. In real scenario, of course, we use numbers. Here, we use numbers. Account determination. So what is meant by account determination? See, leasehold land is as a class. For this, land is account determination. Similarly, for DRLBLAND we have already created account determination. That account determination, I need to link up here. See land, DRLBLand.

Screen layout rule. So we have created screen layout rule. DR, DRLA. Screen layout rule for land. Number range. So I’m assigning number range 01. The number is whatever we have created. So this is asset class for land, this one, leasehold land. Similarly, freehold land also have to create. Click on next entry. Freehold land, DRLB. Freehold land means land on which no lease is there. Land belongs to us. So DRLBFHLA land. Same even account determination for this land only. Screen layout rule, same screen layout rule. Number range, same number range. And here no AUC because for asset under construction we use line item settlement. For all others other assets what I do, I take. One more thing is you can use your inventory data. So inventory data means asset is included in the inventory. Generally, for furniture fixtures, etc, we use this. That is, plant and machinery, we use this one. Next button. So we have created, 2 asset classes. Now buildings is account determination. For that asset class is admin building, factory building, guest house like this. So I’m creating admin building. Admin building for DRLB. DRLBADBU. For this account, determination is DRLBBUILDING. See, DRLBBULD and screen layout rule we have created. DRBU and number range 02. Here, drill down, you’ll get it, of course. See, this is the company code. So DRLB 1234. So I have to start here For building.

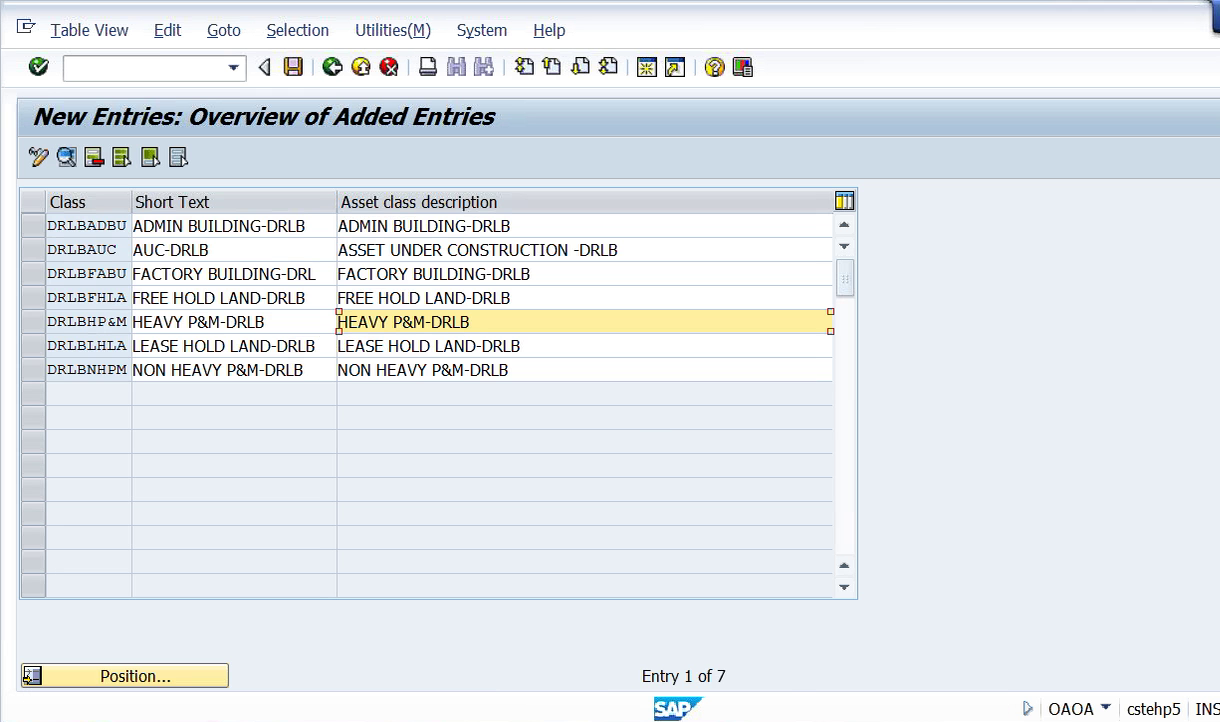

Next button. Admin building. Then factory building. FACTORY BUILDINGS-DRLB. Here, DRLBFABU, factory building. But account determination is same, DRLBULD. Screen layout, same. Number range, same I’m using. For total account determination level, I’m using the number range. Next. Factory building, admin building. So lease hold and free hold and okay guest house. I’m leaving it. I’m not creating. 2 are sufficient. Next, plant and machinery. So heavy plant and machinery, non heavy plant and machinery. So HEAVY P&M-DRLB. DRLB heavy plant and machinery. Account determination, DRLB, plant and machinery. Screen layout rule, plant and machinery. Number range, I’m using 03. Including the asset plant and machinery. Next, non heavy plant and machinery. NON HEAVY P&M-DRLB. So DRLB will be non heavy plant and machinery. Right. So what I’m telling you, as I told you, we use generally numbers here. But here, for the purpose of, our convenience, I’m using abbreviations. Account determination so plant and machinery screen layout rule.

Next is AUC for asset and recurrence section. Asset and reconciliation. DRLBAUC asset under construction. Account determination, DRLBAUC Screen layout rule also, we have created DRAU, Number range, 09. So these are the 7 asset classes we have created. And all these are all asset classes.

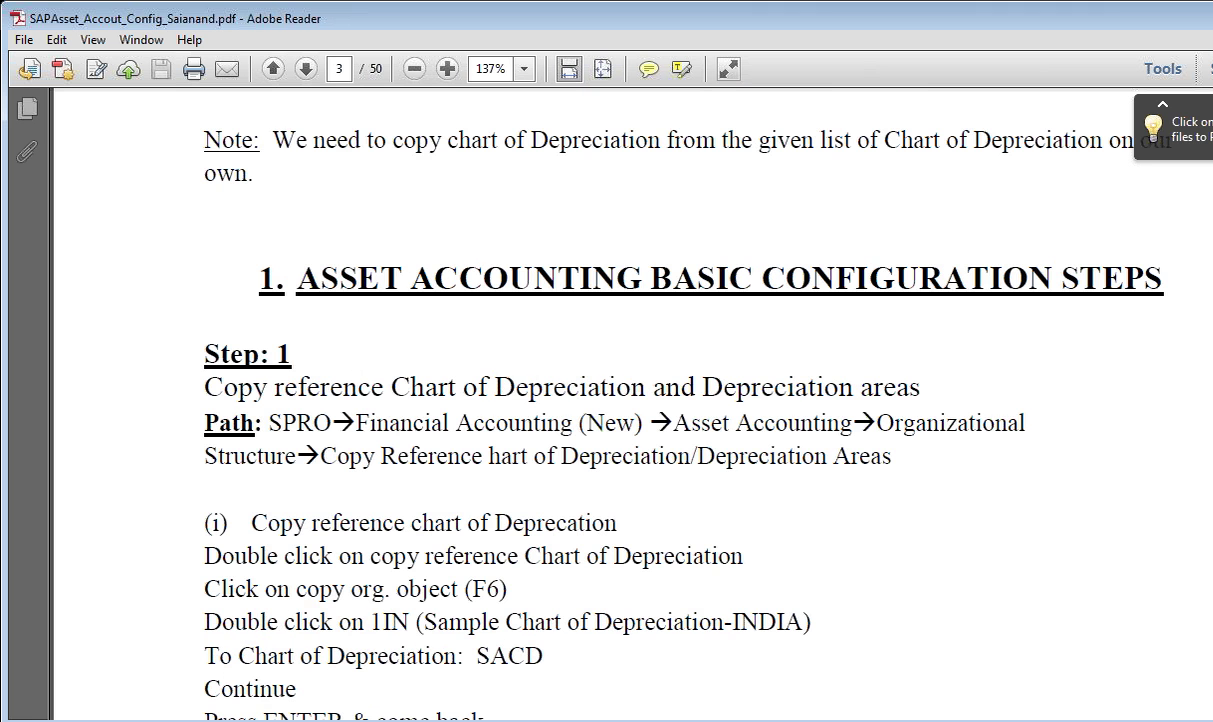

Admin building, factory building, freehold land, leasehold land, heavy plant and machinery, non heavy plant and machinery, and this AUC. Come back. See, in this cell created as a class, 1,000, 1,010, 1100, 2,000, like this. Even in real scenario, okay, depending upon the time requirement, we use alphanumeric number, numeric number as per our convenience, we’ll create it. So as a class, we have created. Specify chart of depreciation, country specific functions. So next next, what we need to do is, next, we have to create GL accounts then we have to create the GL accounts and integrate the same with asset accounting. So here you have to plan for our GL accounts. So what are the GL accounts to be used? So my plan of using GL accounts is these are the GL account we are going to create. So this already have given all these things in your notes also. Let me show you. Asset accounting. Alright. This table is also there. See, this is the configuration steps.

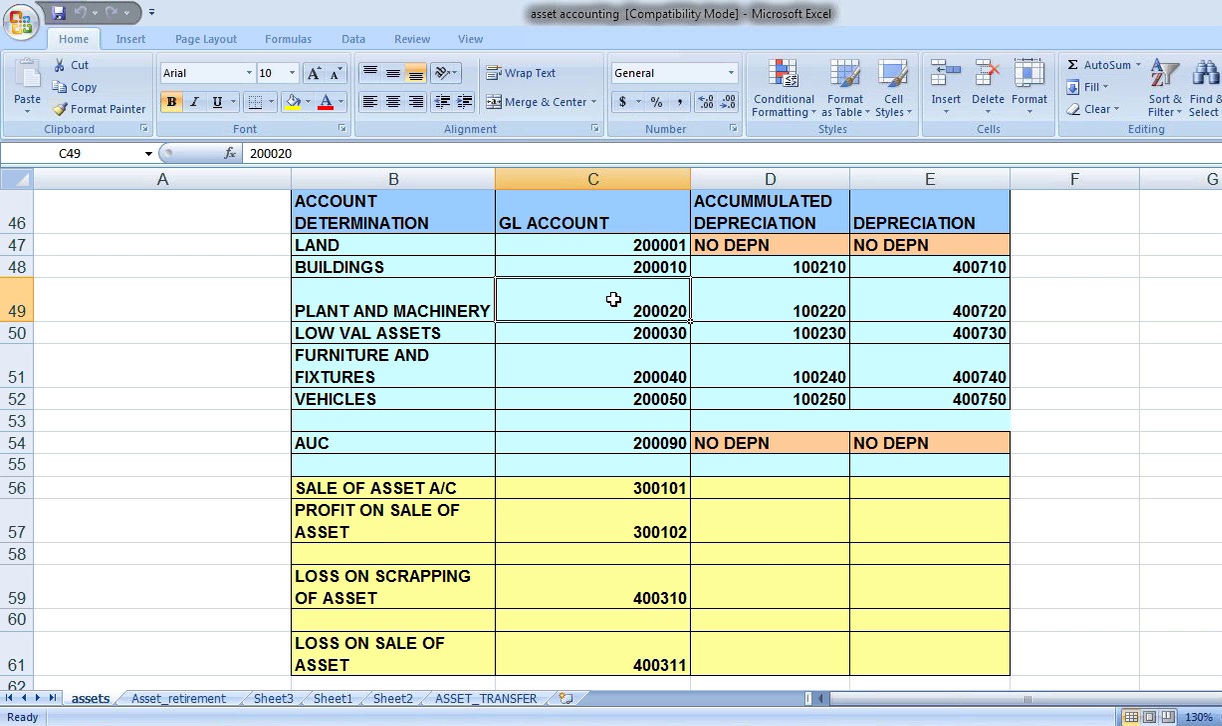

So we have done all these things. Now we are going to create GL account that I think that is the 9th or 10th step. So this is asset classes creation. 8 define asset class. So number 9, these are the GL accounts. So better you create GL account for all. But for me, I have created land, building, plant and machinery. So I’m taking only these 3. Land, building, and plant and machinery. Now what GL accounts we require? We require, number 1, GL accounts for land, building, plant and machinery. So we have already created account determination for this. Here, with same account determination name, I’m using GL account. The total land, whatever we acquire, we sell or anything, debit or credit should go to this GL account. So for land, this one, buildings, this, plant and machinery like this.

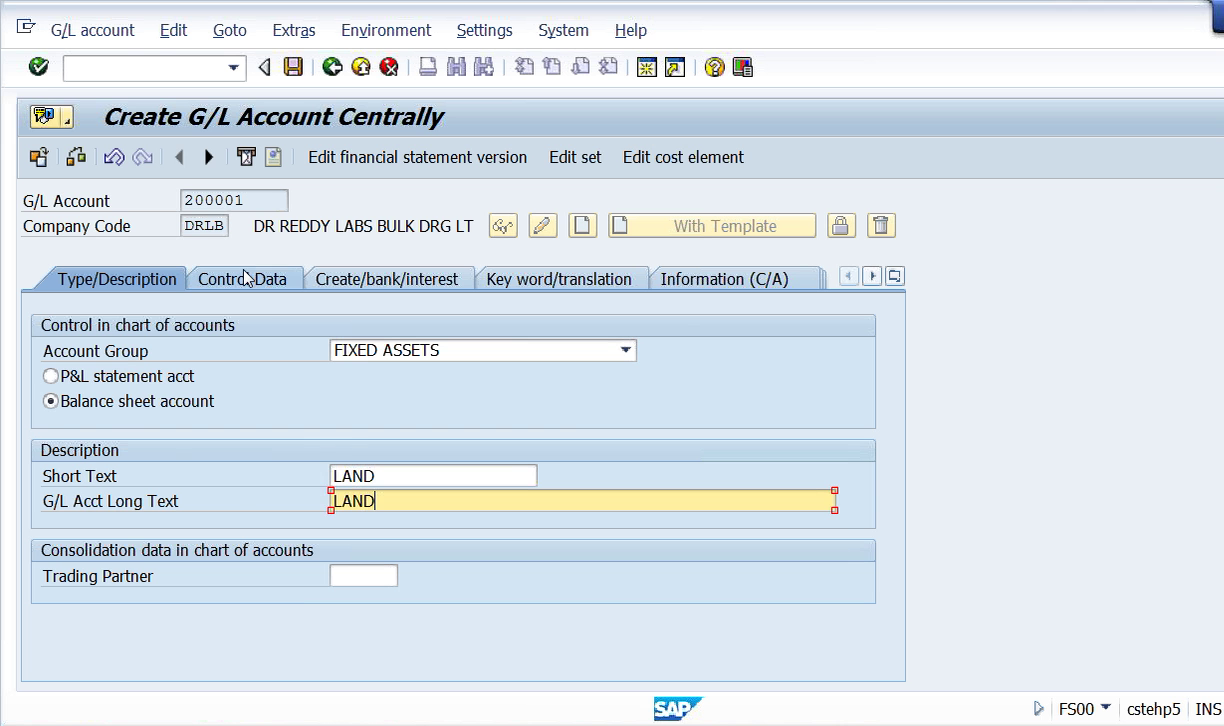

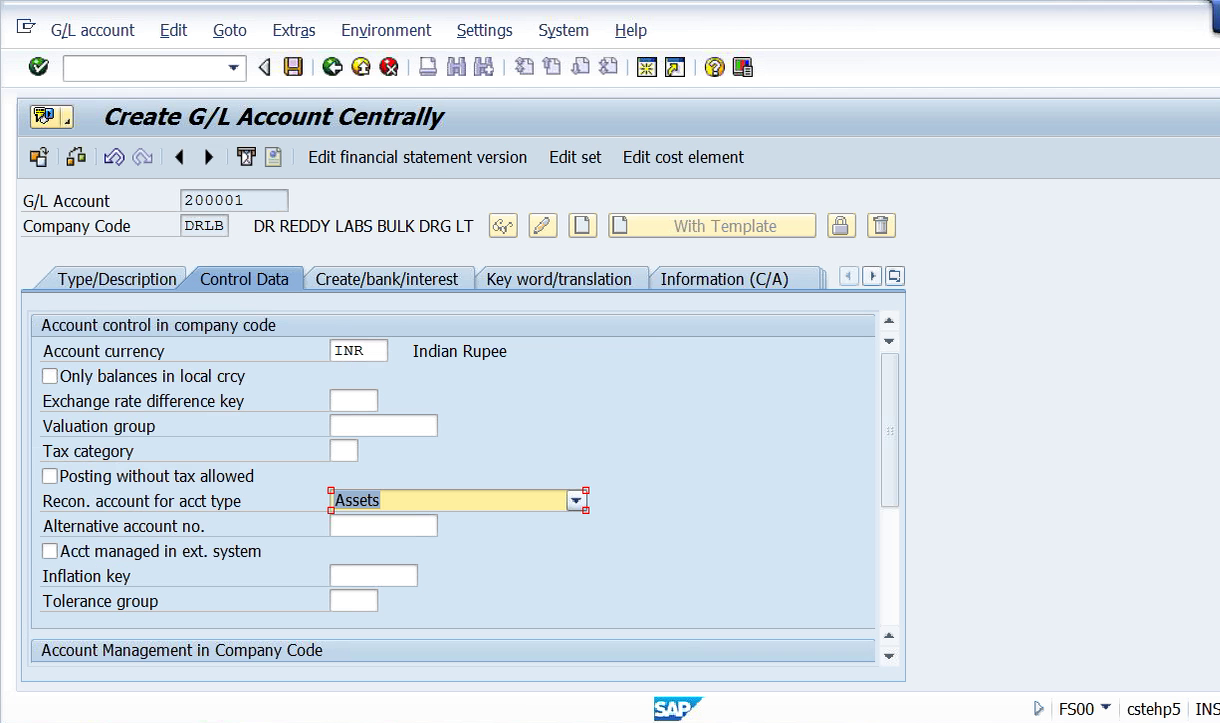

Next, accumulated depreciation. Now what is meant by accumulated depreciation? Why should we accumulate? Means the accounting entry for the purpose of depreciation is that depreciation accounted are to accumulated depreciation. Generally, people say that depreciation account return to asset. That’s a general mistake done by several people is that depreciation account return to asset, but it is not like that. We need to maintain accumulated depreciation in the books of accounts. Accumulated depreciation is nothing but the depreciation which is accumulated over a period of years. So in the balance sheet also, the presentation should be the total historical value of the asset, less depreciation up to last year and the depreciation in the current year, then totally we reduce it, and we’ll show the value in the balance sheet. So for that purpose, we need to accumulate the depreciation, and we have to show the same in the books of accounts. Now so we we don’t have any depreciation on land. Land is only appreciation, no depreciation. So that’s why no depreciation. No accumulated depreciation, non depreciation. Buildings. Yes. This is the GL account I’m going to create. And GL accounts are assets, land, billing, etc. They are the fixed assets. So that’s why if you observe our asset account. Next on group. See fixed assets. Fixed assets start with 2 lakhs 1 to 2 lakhs 100. So that’s why I’m picking up asset numbers from here. So 2 lakhs 1. I have to create now GL accounts for all these things. So what I will do, I’ll create GL account for these accounts, then AUC also I’ll create. 2 lakhs 1. So fix reset. I’ll create one more session. Alright. We know that FS00 is a GL account. 2 lakhs 1 for our company code DRLB. Click on create. So here, GL account is nothing but there is a recon account. Why recon account? I’ll tell you later.

So here it is fixed assets. This is balance sheet account. There’s no doubt for this. Fixed asset is balance sheet account because assets are represented in the balance sheet. Assets and liabilities both. So here I’ll take land. In the control data tab, we have to take assets because here asset is a recon account.

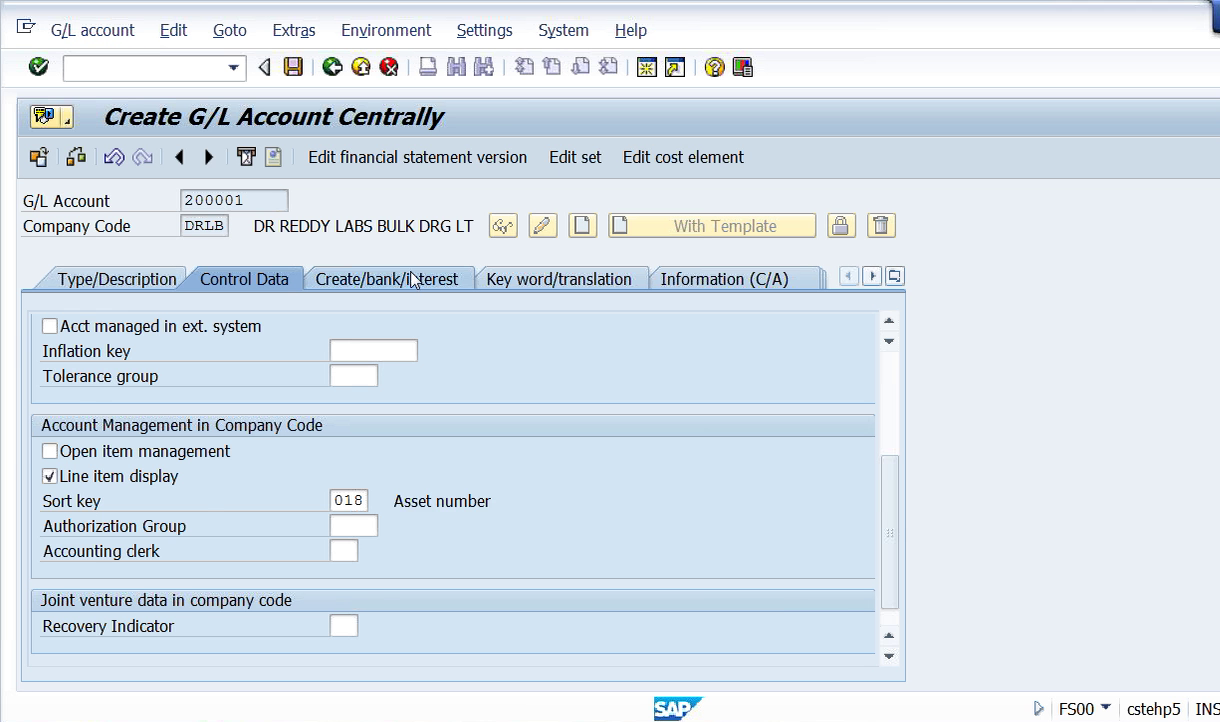

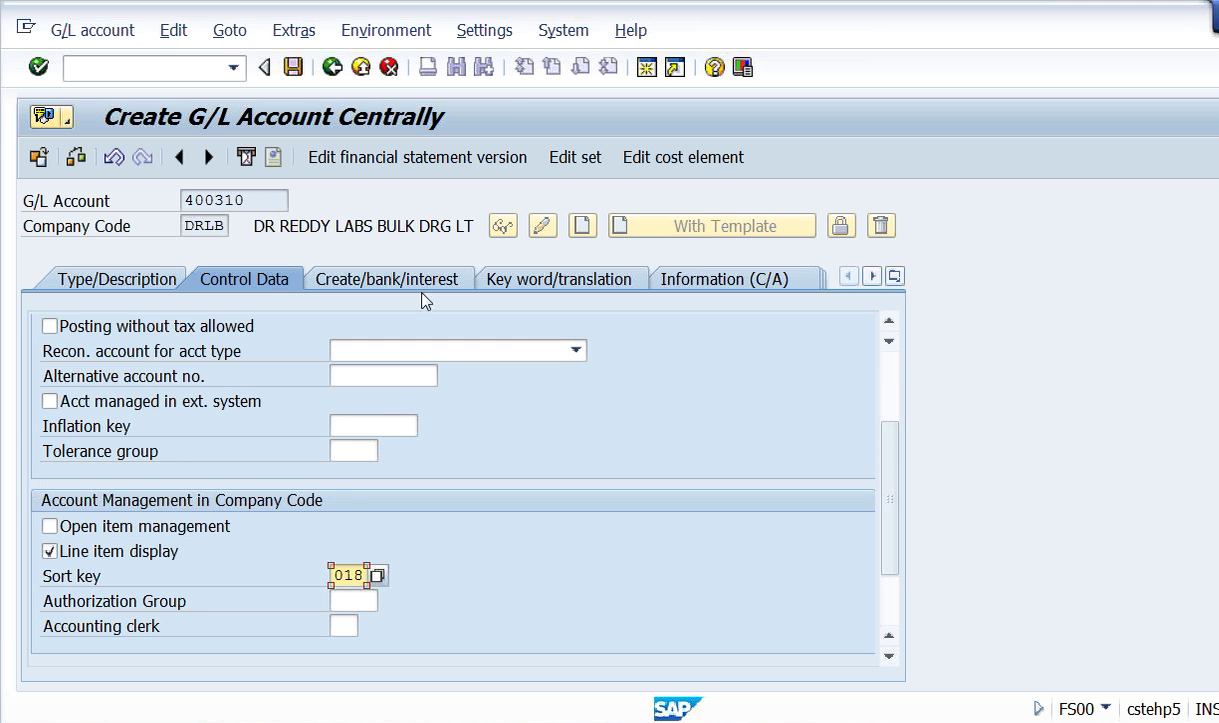

So you know what is meant by recon account, and sundry debtors, sundry creditors, all those things are Recon accounts. So Recon accounts are those account to which the accounting entries posted only through sub ledger. Now what is the sub ledger here? Subject ledger is nothing but asset master record. So asset master record, we have an asset explorer. So that asset account will be there for each and every asset. That will be the recon account, there is a sub ledger account. If you post to that account, automatically, it will be posted to GL account. But, anyhow, that we’ll see later. So this is the recon account. We take 18 asset number, sort key is 018 through asset number. Check line item display.

And for field status group, you can take G067 because it’s a recon account. So for creating the fixed assets, fixed assets, name of the asset, and, here the crux is this, it should be a recon account. Anyhow, this is same, and this is asset number wise we are going to sort out in the GL account. And here, GO67 because this is a reconciling account. Save it. So we have created land with lease hold or free hold. Both will be posted to this. Now So 2 lakhs 1. Just I’m leaving some numbers and taking 2 lakhs 10 for buildings. In future, I don’t know if I want to use it, that’s why I’m just leaving some gap. I’ll take the template. 2 lakhs 1. Company code DRLB. So for that, the description is GL account for buildings. That’s why just everything got copied. So buildings, then plant and machinery. Plant and Machinery, Save it. So when you create, you create furniture and fixtures. Everything you can create.

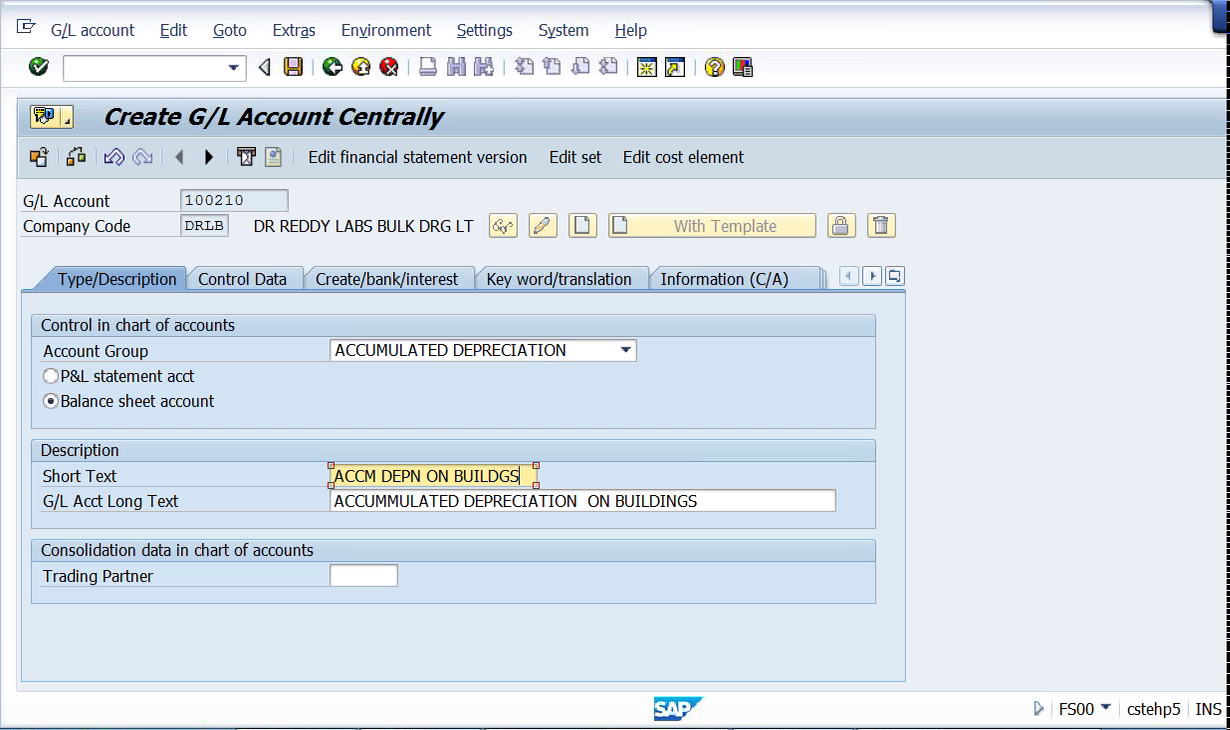

Then coming to AUC also, I will create 2 lakhs 90. Here one thing I forgot. When we have created the asset class, define asset class. For AUC, AUCDRLB, we need to check line item line item settlement. This is very important. This I’ll tell you when we go for the AUC and AUC creation, this we will see in controlling. So 90 AUC. First, we have created this class, this asset, GL account. Then accumulated depreciation. So no accumulated depreciation on buildings. balance sheet account. ACCM DEPN ON BUILDGS.

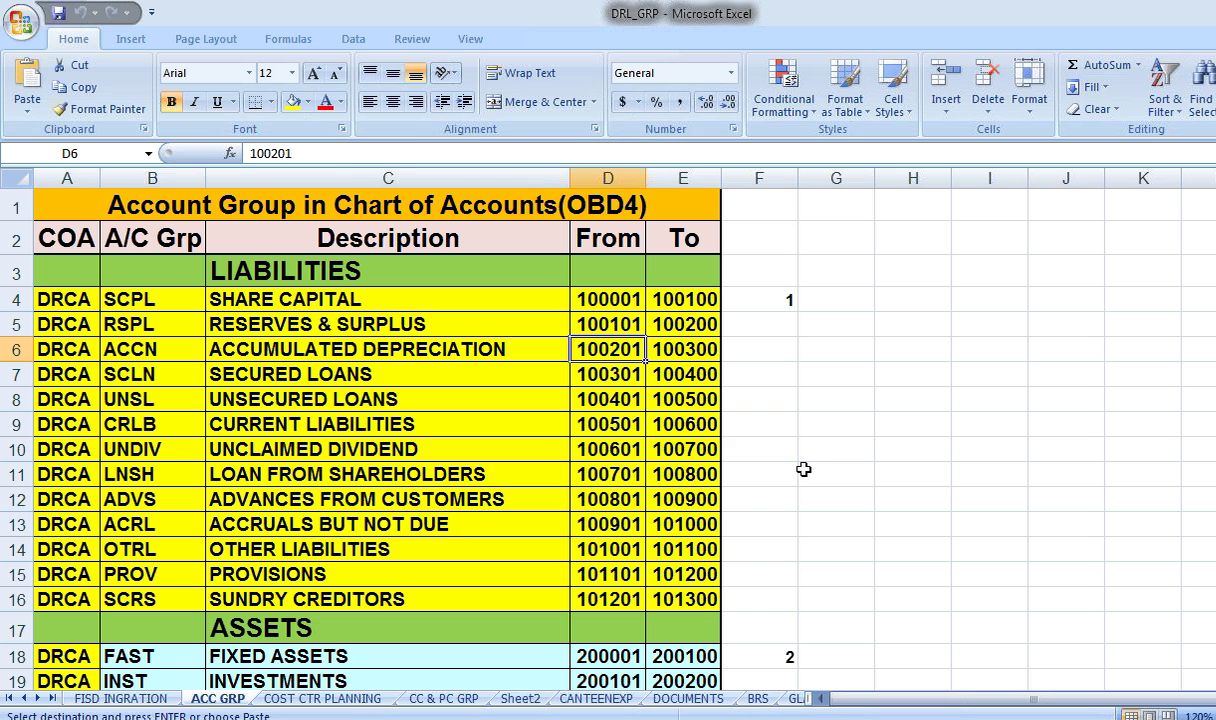

Same way, this also recurring account assets because we are going to create depreciation for each and every asset, accumulated depreciation. Line item display, same 018G067 plant and machinery. On buildings we have created this. Plant and machinery 1 lakh 220. Here, how I got these numbers? See when you are, going through the account group, see accumulated depreciation.

So 1 lakh 201 to 1 lakh 300. But here, 1 lakh 2 lakh 1, I have not taken. 1 lakh 210, I have taken because 201, there is no accumulated appreciation on land. That’s why that number also for the sake of symmetry, I have left it. So now 100210 we have created. Then coming to 100210, Create template. Now accumulated depreciation on plant and machinery. So whenever we create GL account with template, don’t forget to change the narration, the text part. Here we have created these 2 and no depreciation on accumulated.

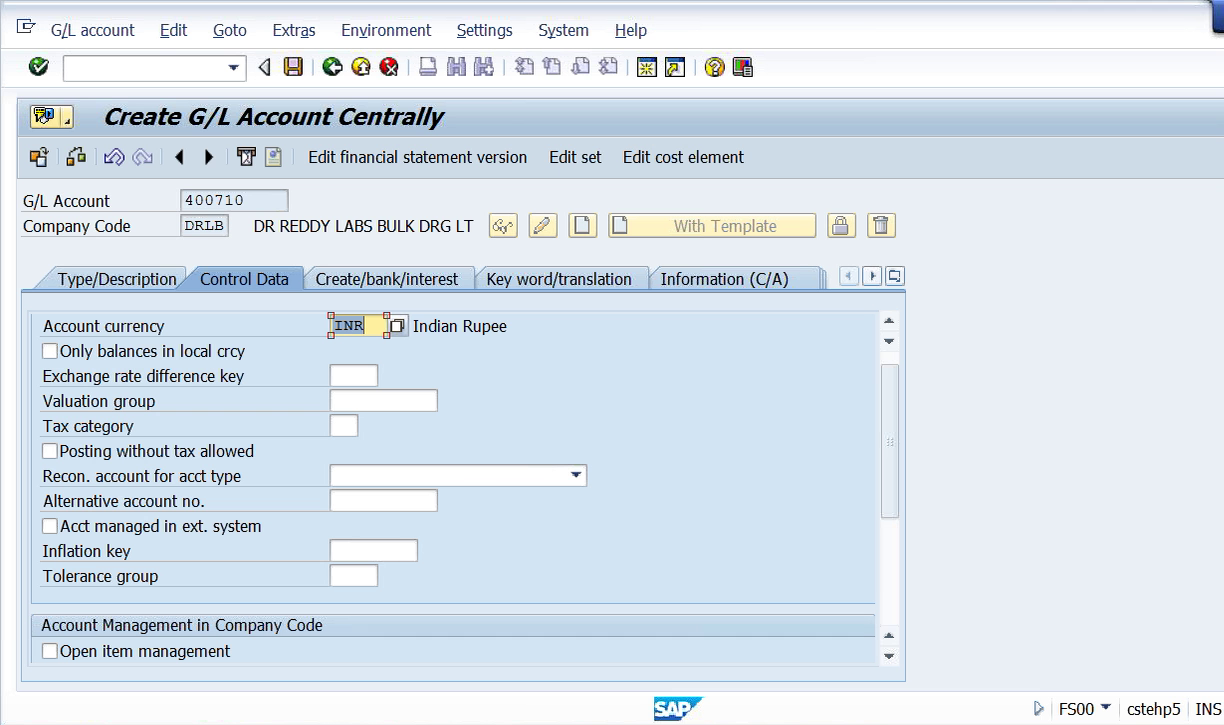

Next, depreciation. So difference between depreciation and accumulated depreciation, I think if you are a B.COM graduate, I think, you know about it. So accumulated depreciation is nothing but the liability for us and, there’s a balance sheet account. But depreciation account is nothing but there’s an expenditure. Every asset is subjected to depreciation as per the rates that are specified in the respective countries companies act. So here, what I’m going to do, let’s create 400710. In the same way, just you have the 400701 onwards, depreciation will be commenced. But since the first one is not there, so 400710, 100210, 2 lakh10. Like that, I’m just maintaining some symmetry. This is depreciation on buildings. Starting with 4 means expenditure. Depreciation. P and L account. So I say depreciation on buildings.

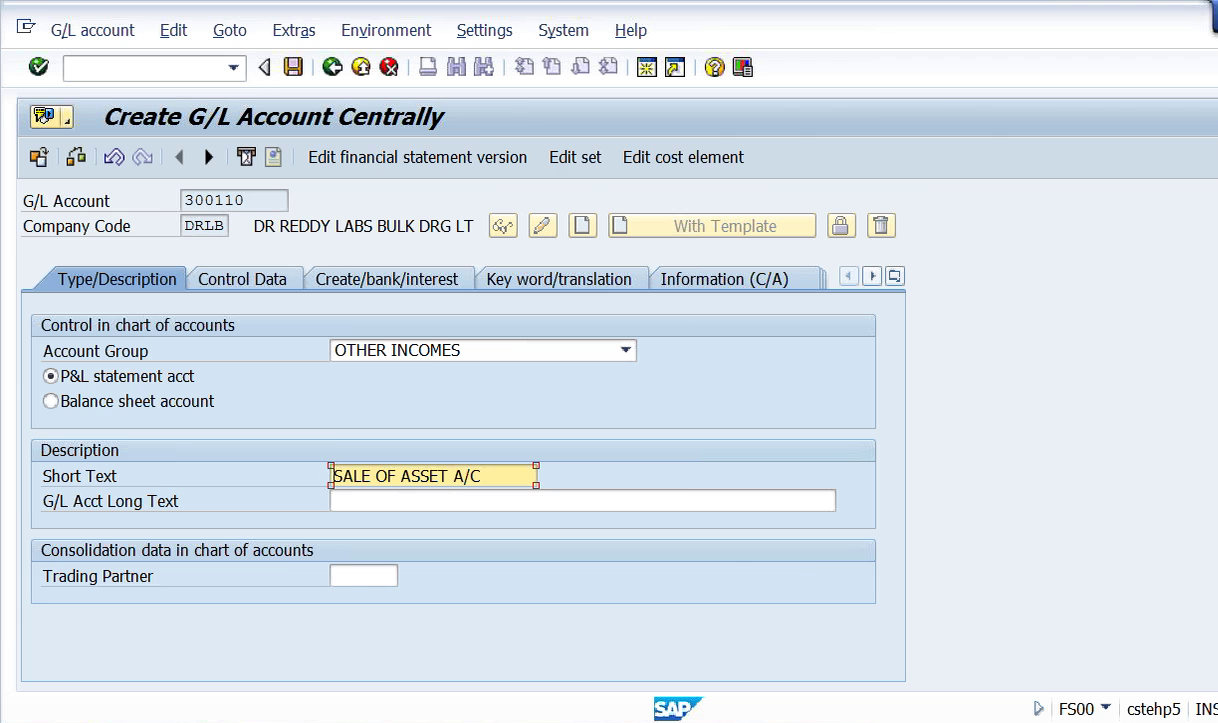

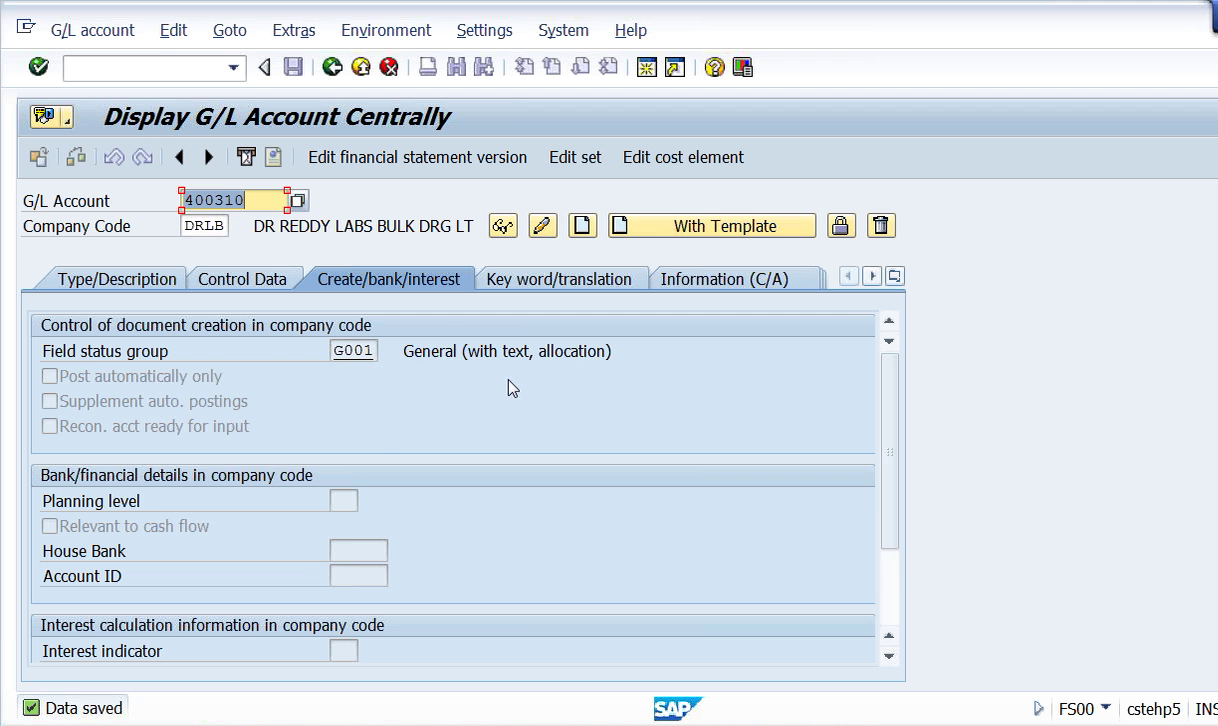

So here so this is expenditure account. My P & L account. That’s why I did not change it. Just line item display. Sort key, you can take same. That is asset number wise. See asset number wise sorted out in the GL account for that purpose. And here, field status group G001. So this is 400710. So this is depreciation on plant and machinery. Save it. So what we have done, we have created land, buildings, plant and machinery and for this accumulated depreciation and ordinary depreciation, all these things we have created. Now apart from that, we are going to create 4 more accounts. That is nothing but sale of asset account. What is meant by sale of asset? The importance of this account, we’ll come to know only when we execute the sale of asset account, then you’ll understand that the purpose of sale of asset is, say, whenever we are going to sell the asset, bank account return or customer account return to asset account because asset is going out. But, here, what is the purpose of sale of asset account? It has got some significance. So when we retire the asset, when we come to the retirement of asset, then I’ll let you know. But we have to create one sale of asset account. This is just like, I’m taking on income side, but other income I’m taking here. So sale of asset account. 300101, we have already. Quantity rebate, we have, other income, we have created 300101, 300102 also, I think we have created, client discount. So what we’ll do is, 310311.

So here also, what we do is sale of asset account 300310, I’ll give. I’ll make it. This is sale of asset account. So there’s importance for sale of asset account that let us see.

So this is other income, group is other income. P & L account only. Sale of asset account. Here, I can take 001 also. Here, while creating the GL account, sale of asset account, here parameters also you need to remember. Under create bank or bank interest tab, field status group is G052, fixed asset retirement. So this is very very important. G052, you have to choose. So what is G052? Account for fixed asset retirement, this you have to specifically remember. Why I’m taking 052? Accounts are fixed asset retirement. So this also, I’ll tell you once we go for the retirement. Retirement means asset retirement. Generally, we call it as sale of asset is called retirement, retirement of an asset. Now save it.

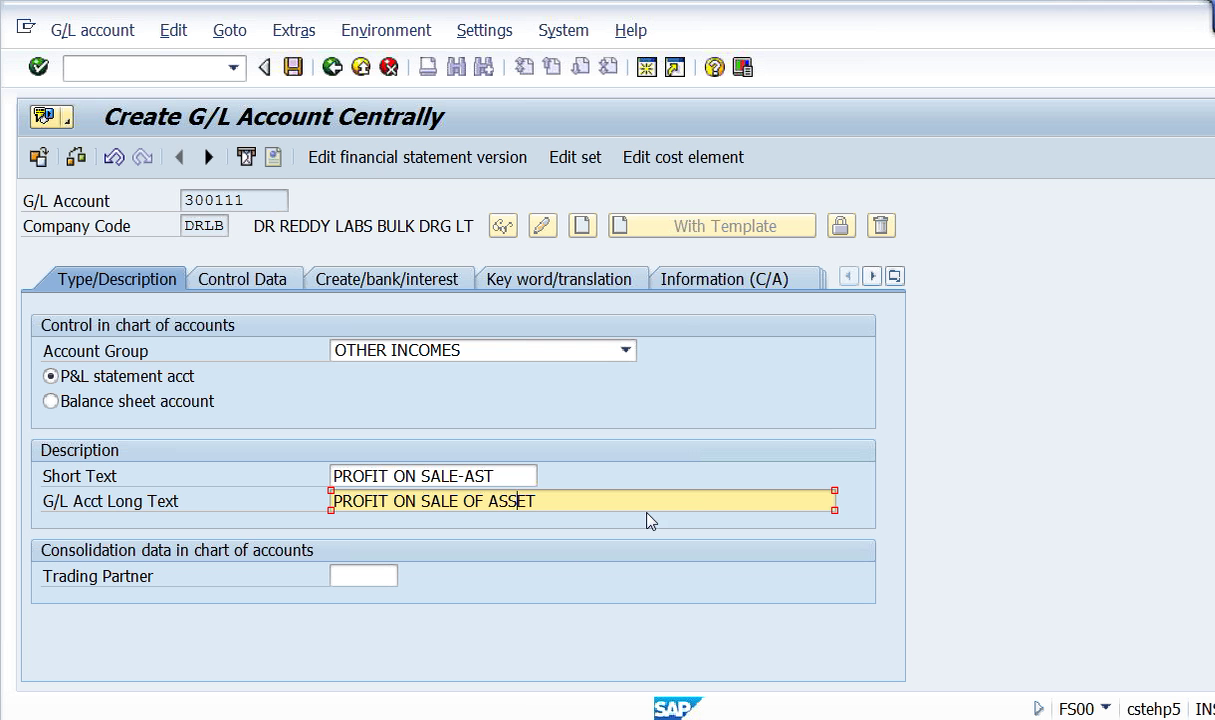

And then 300111. 300111 is profit on sale of asset or gain on sale of asset. This is also other income, P and L account. Here, this is profit on sale of asset.

In control tab, nothing different, check line item display. Field status group can take G001, So nothing special in this. So this is nothing but profit on sale of asset. So what are the profit that we are going to get, that will be posted to this account. Once we create all these GL account, next is the Herculean task. The very big task is assignment of GL accounts with asset accounting. That is a bit typical step you need to go through.

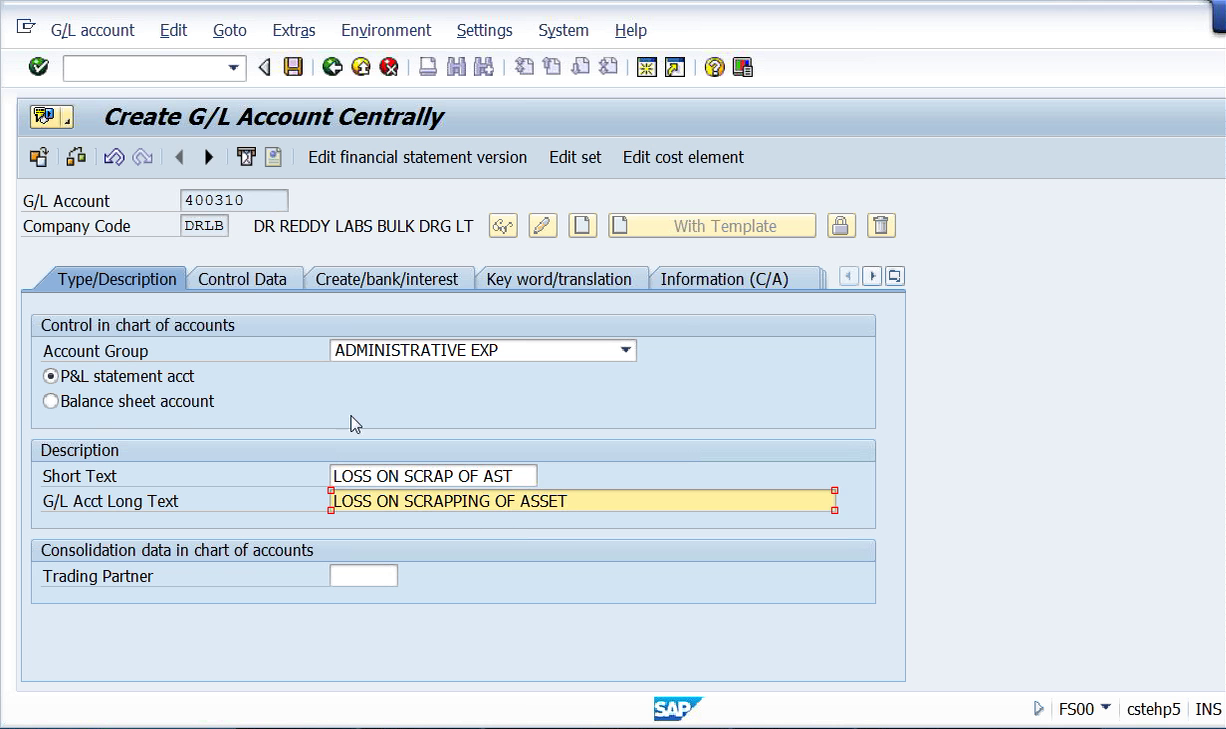

Now, loss on scrapping of asset. When you are going to get a loss, that is when you scrap an asset after the end of its useful life, so the loss whatever we get, we want to post to this account. Next is loss on sale of asset. In case, if you are going to get loss on the sale of asset, That should be posted to loss or profit. Loss is given 400311,. Profit is given 300111. So, whenever we sell an asset, then at the time, we may get loss or profit. So, if loss, I should post to this account 400311. Loss on scrapping goes to 400310. So GL account is 400310. 400310 means it comes under administrative expenses only. Like, P & L account because that is loss on scrapping of asset.

So when we get loss on scrapping of the asset because what happens? So once the asset life is over, if you are scrapping it, we have to post to that account. You may say that we may get profit also. See, we may get the money when you sell the scrap. So, generally, what we do is that whatever the plant and machinery that is there, anything that is scrapped, they’ll not sell immediately. All the assets that are scrapped will be thrown into a backyard of the company, and, once in 6 months or once in a year, we’ll call some vendors, those who buy the old iron etc., and the scrap of material, everything, that will be collected and, that will be sold at a time. But until then, at this juncture, it is only loss.

Now what is the next account? Loss on sale of assets. So because when we sell it, you may get loss or profit. So we have created loss on sale of asset account, profit on sale of asset, loss on scrapping of asset, loss on sale of asset. And sale of asset account, nothing but that will be used for the purpose of retirement of an asset. The importance of this we’ll see later. So now the next step is, now whatever the GL account that we have created, all these things we need to integrate with asset accounting. In fact, this is a big step.