Asset Accounting Overview

So, my next topic is Asset Accounting. It’s kind of part of FI, but sometimes it’s treated as a separate module. So far in FI, we have covered GL, AR, AP. And in cost center, we have covered Cost Element, Cost Center, Profit Center, And Internal Order. Now I want to cover Asset Accounting or it’s called Fixed Assets. It’s under Accounting, Financial Accounting, and then you have Fixed Assets.

Thank you for reading this post, don't forget to subscribe!

I can use a PowerPoint document. It’s a very good document to go over to give you a basic understanding of what is Fixed Asset Accounting.

So, I guess you are clear on the AR, AP that they are like subledgers under GL. So, in AR and AP you have a reconciliation account which is a GL account and that is the link between the sub ledger AR, AP and your main ledger the GL. So, all the transactions are at the sub ledger level like your vendor invoices, customer invoices, but the total is at the GL level, the total is updated at the GL level. So same thing with Fixed Assets, all the transaction data is at the sub ledger fixed assets and the total amount is at the GL level through reconciliation account. So, the same concept that as we have with AR, AP in terms of the sub ledger and the main ledger. But instead of customer and vendors, we have assets. So, assets, we will go in the presentation, but assets can be your vehicles, your building, your equipment, anything that you have in your office like furniture, computers, your building, your labs, these are all the fixed assets.

So why are they Fixed Assets? Let’s talk about that. Let’s say we are paying our telephone expense, telephone bill, so that we know it’s an expense and we expense the whole thing immediately, the same month when we receive the bill. Some things, let’s say, if we buy a server, computer server that cost us, let’s say, $20,000. We cannot expense the whole thing in the same year because we’ll be using it for more than 1 year, let’s say if we are using it for 4 years. So basically, in that case, we cannot expense the whole amount in the first year. What we have to do in accounting is called to ‘capitalize it’. So basically, you add the whole thing, the $20,000 to your balance sheet. So, the accounting entry can be debit asset and credit your liability or credit your vendor and then you pay your vendor then that liability is removed. But you don’t want to expense the whole 20,000, you want to book it first as an asset on your balance sheet, the whole 20,000 and then, you basically expense it based on its useful life. So, if its useful life is, let’s say 4 years, then you divide the total cost by the number of years. So, we will divide 20,000 by 4. And that amount, we will expense it or in accounting terms called ‘Depreciation’. We’ll depreciate that amount per year for the next 4 years, in that case if the life is 4 years. So, the first year, we can only depreciate or we can only expense the ¼ of the amount because its life is 4 years. So that’s the basic concept of Depreciation, that you don’t want to expense the whole thing, the first year or the first month. You want to distribute the expense, to the useful life of that asset. So that’s why you want to book it to your balance sheet. Let’s say if it’s like we said, server, so we can have one GL account for this type of asset. We can call it ‘equipment’. So, we can have one GL account for equipment, and that asset will be linked to that GL account. So, when we buy it, we will debit this GL account. And then when we continue to depreciate it, for that reason, we will need a contra asset account, and it’s called ‘Accumulated Depreciation’. And we will go over that when we will post depreciation. You will see that.

So, basically, when we create an asset, for each type of asset, we need two GL accounts. One account will have the actual cost of it, let’s say, 20,000. So, one GL account will have 20,000. So, we will have to create another GL account for Accumulated Depreciation, that account will track how much we have depreciated so far, and that account will have a credit balance. So, let’s say we bought this equipment for 20,000, we will debit equipment GL account for 20,000. And on month end, let’s say we are depreciating it for $5,000 for the first year, so that depreciation entry is also automatic. We just have to configure it, but we will also run that. So, with the depreciation run, it will debit 5,000 to depreciation expense. And what account should it credit? It will not credit the main equipment account, it will credit the accumulated depreciation account for the equipment. So, depreciation will be tracked by that account. So, it will debit depreciation expense, credit accumulated depreciation. And once we see that in SAP, then you will have a better understanding of how it’s working. So that’s the basic. And let me go over to that PowerPoint, and then you will have some more information. So, let’s go to the first slide.

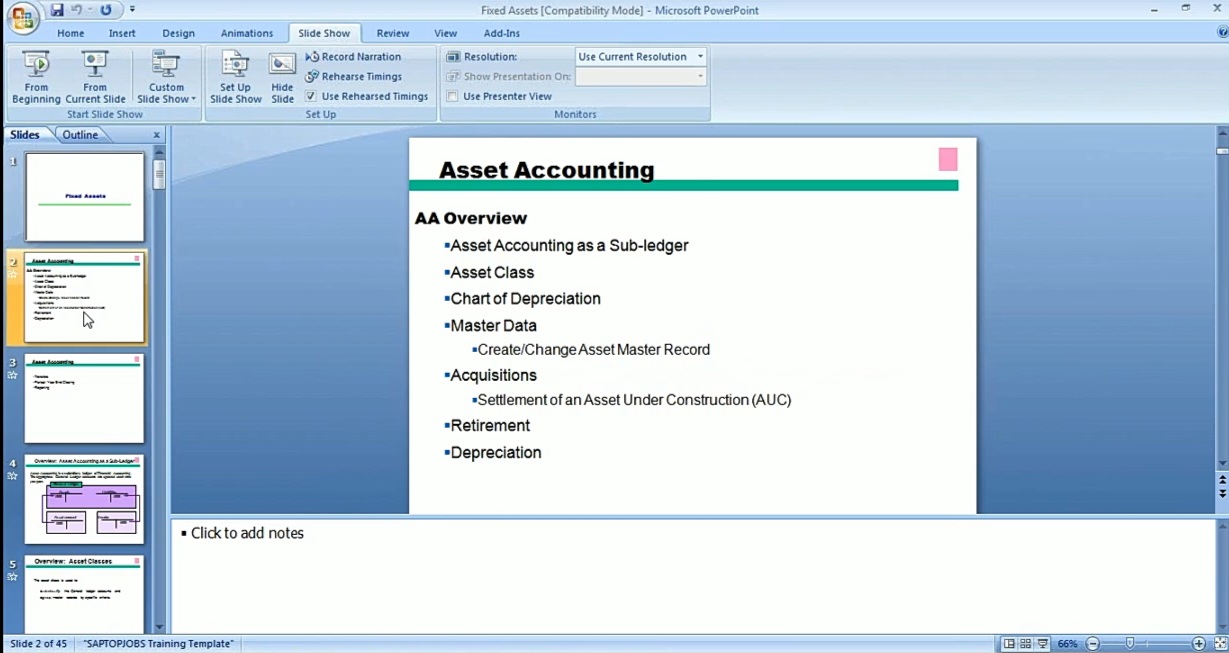

Like I said, Asset Accounting is a subledger under GL. And in this, we will go over what are Asset Classes, what is a Chart of Depreciation for Assets, and then Master Data, Acquisition of Assets, Retirement of Assets, and then Depreciation. We’ll go over these topics. So, this PowerPoint will just give you an overview, and then we will go in SAP first configure asset accounting, and then do these transactions. Transfer, you can also do some transfer, transfer one asset to the other, Period End Closing and Reporting.

So, like I said, Asset Accounting is a subsidiary ledger of financial accounting. The prepaid GL accounts are updated each time you post. So, let’s say when we acquire an asset, when we are getting an asset, we will debit asset and credit vendor. So, and behind the scenes, it will be updating the GL. So, asset account will be linked to the GL account, and then the vendor will be linked to the liabilities or AP account.

In our case, we have created accounts payable account in the GL. So, whenever we post a vendor invoice, that GL is automatically updated. Just like that, you know, with asset accounting, when you post an invoice, it will debit asset and credit vendor.

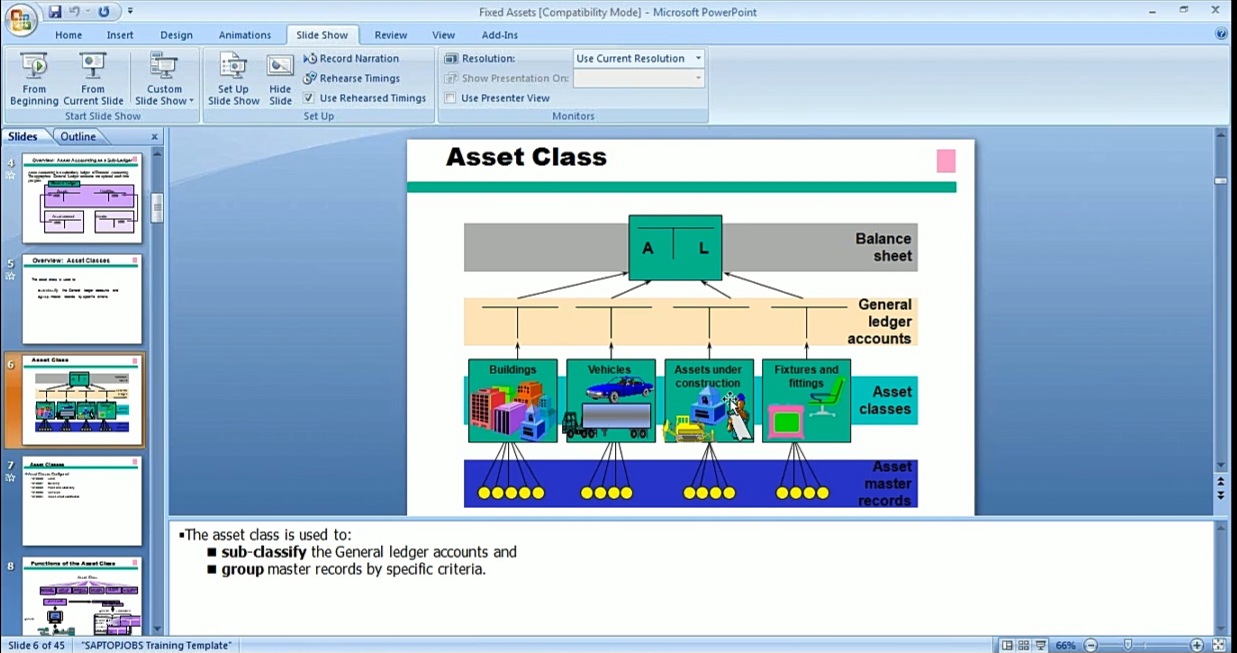

So, let’s go over to the next topic. What are Asset Classes? Asset Classes, basically, you want to group your asset into asset classes. Otherwise, you might have thousands of assets. The way you group them is by Asset Classes. So, we can have one group for buildings, one for vehicles, one for asset under construction, and one we can have for fixtures, furniture, or equipment. And it’s up to us, you can have more than this if we have different type of assets. But, normally, 4 or 5 is a good number, for your asset classes.

And, let me just give you some more information on asset under construction. We can only start depreciation when an asset is in service. We cannot depreciate during its construction phase. So, let’s say if we order an equipment, but it needs 10 different parts. And so right now, we got first part, and we are ready for the second or third. So, at that point, it is called ‘asset under construction’. We cannot start depreciation on it until we receive all the parts and it’s ready for service. At that date, we will start the depreciation. But before that, it will be dumped into a class called ‘asset reconstruction’. So, when we place that asset in service, only then at that time we can start depreciation. So, these are some of the examples of that.

And, yeah, in this case, these are the few examples but like I said, it’s up to you how you want to define your asset classes. Let’s go to the next one.

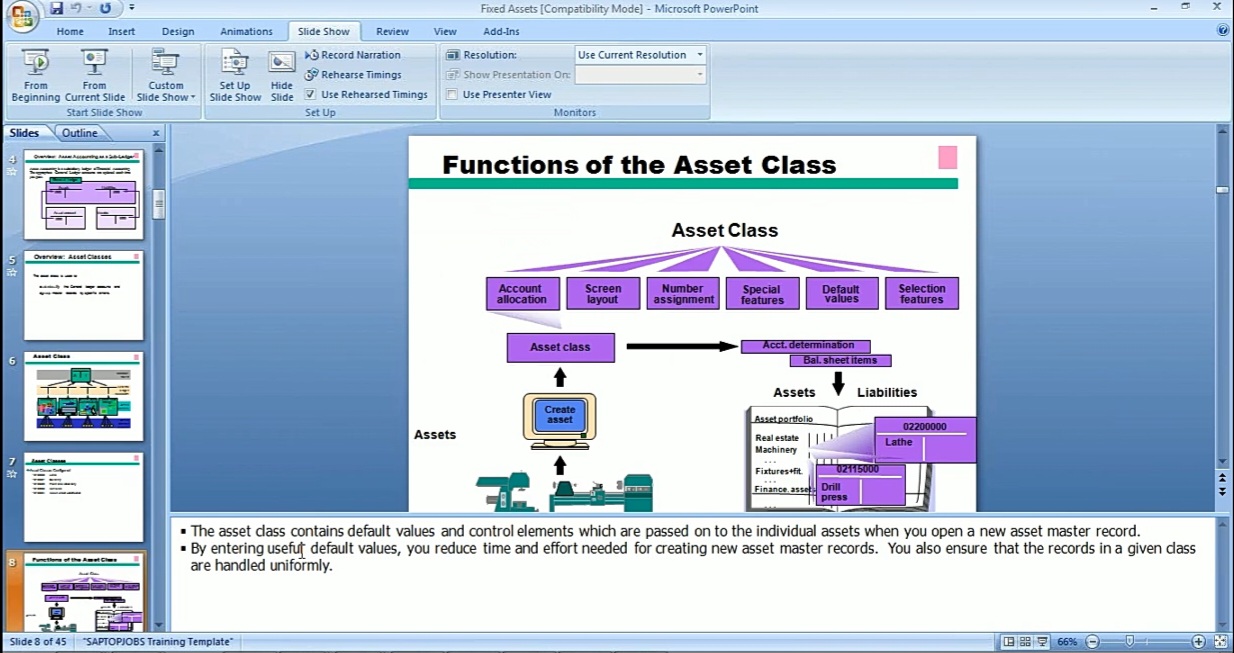

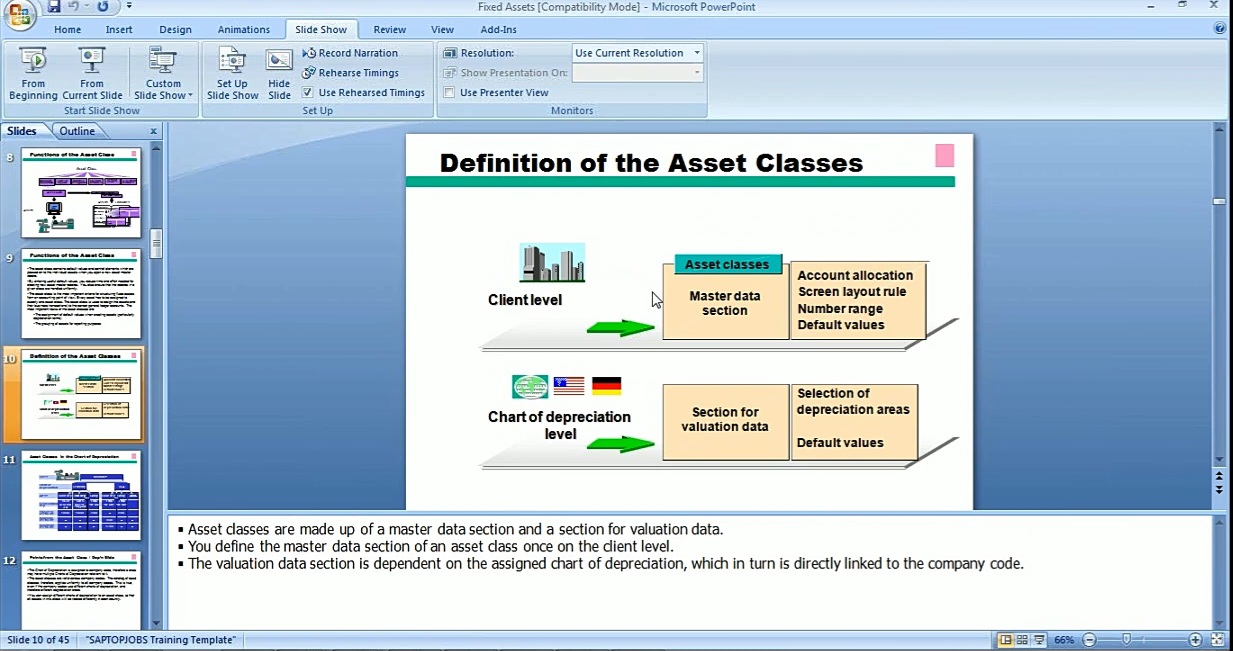

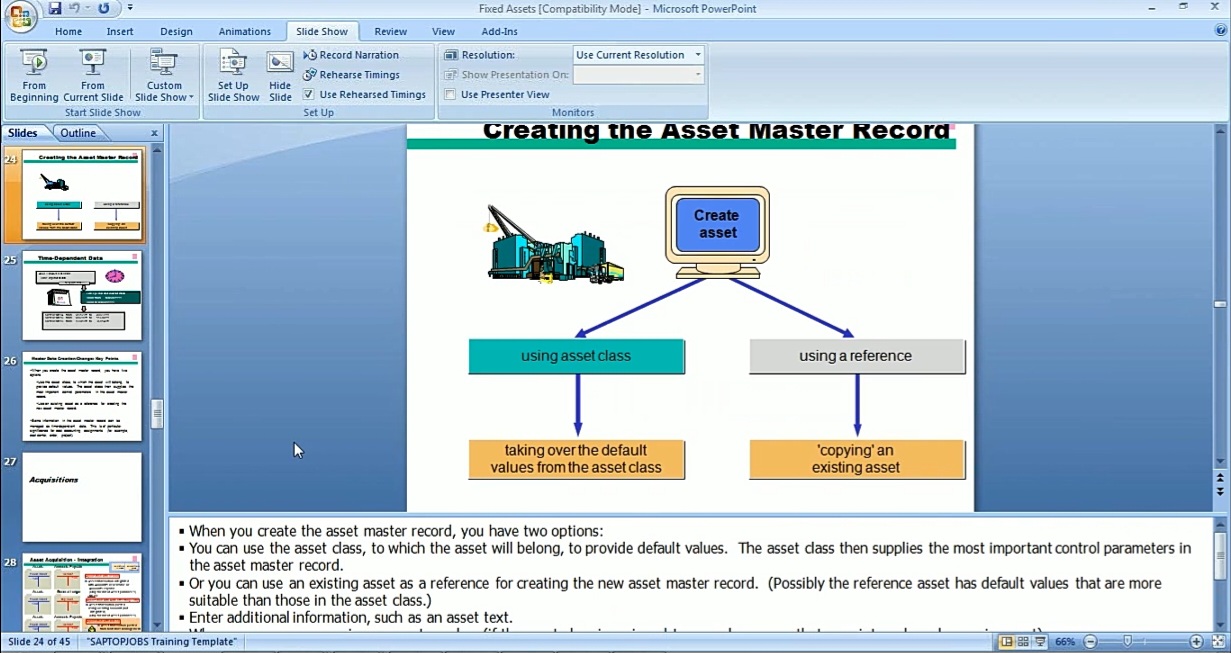

It’s just giving you a cycle when you create an asset. Basically, first thing you have to do when you are creating an asset, you have to first define, what is the asset class for that. And that automatically, that asset class is linked. Each asset class is linked to a GL account. So, let’s say in this example, we will have one GL account for land, one for building, one for plant. So, when I go and create an asset, first, I choose the asset class, and this asset class is automatically linked to a GL account. And some other information that you can enter by default in the master record that you don’t have to enter all the time. Like the life, we can have a preset, we can enter a default life. If we know it’s computers, we can enter 3 or 5 years. So, we can enter default values too, but we can also always change that. So, one thing that is important is, some information is at the Company Code Level, some at the Depreciation Level, and one at the Client Level.

So, Asset Classes; when we create asset classes, it will be available to everybody that is using that client in SAP. So, it’s not at the company code. You know, some information like we were searching for our cost element group, that was at the chart of account level. So, some information like Asset Classes, are at the client level. So, if we create a new asset class, it will be available to everybody who is using that client. But some information is at the Depreciation Level. So, in Fixed Asset, like in GL we have the Chart of Accounts, in Fixed Asset, we have Chart of Depreciation. And this is the first thing we will need to create when we will do the config. And when we will create an asset, we will see asset classes of everybody because it’s at the client level.

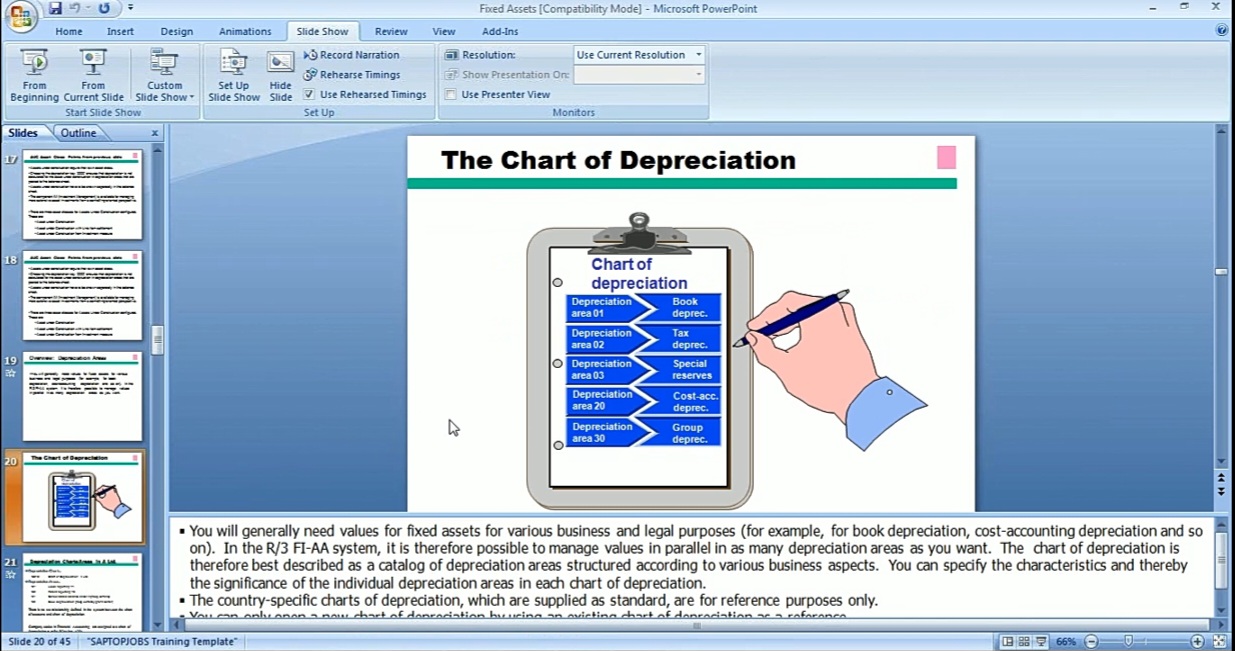

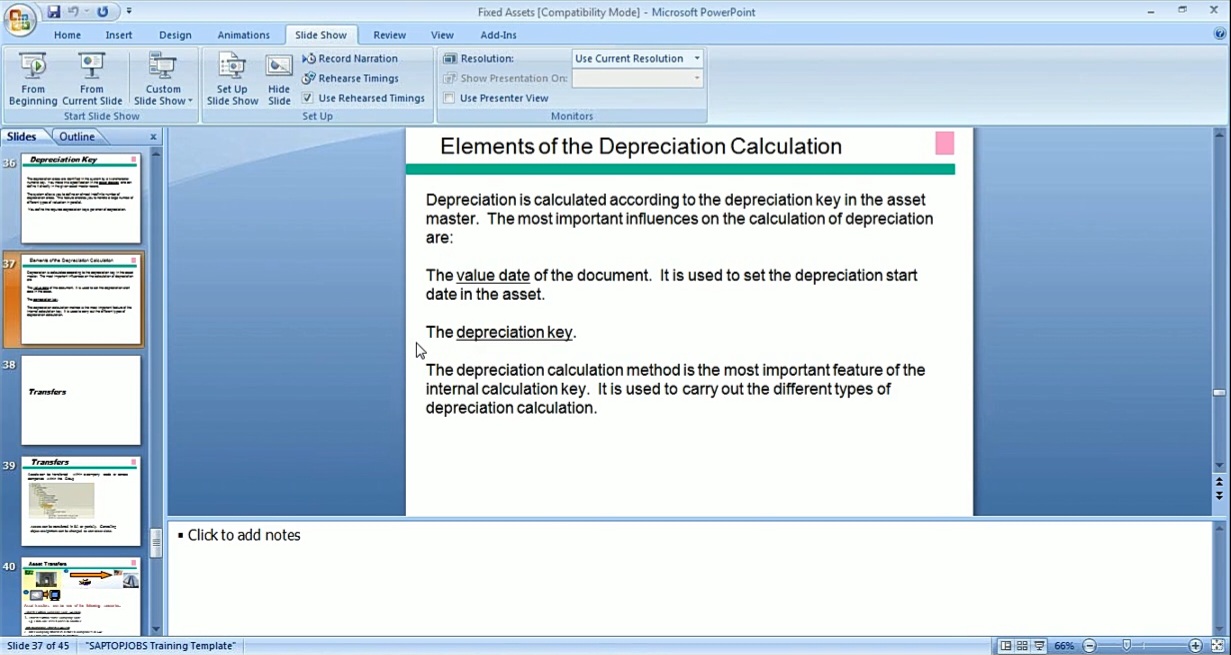

Now this is just giving you some, information. Let’s say machine is an asset class. Let’s say if we are a company in the US, what happens is each company code needs to be assigned to a Chart of Depreciation. So, what we will do in our case, we will assign our company to a US Chart of Depreciation. And that chart of depreciation will have Depreciation Areas, Depreciation Key. So, let’s talk about Depreciation Areas. In accounting, we need multiple depreciation areas. The reason is we have one type for our financial that are prepared under SEC requirements that are for the stock market for Wall Street. That’s under one requirement. We call this a Book Depreciation. One we have for tax; For IRS, there are different laws for doing the depreciation, for Asset Life. They have their own laws. So, for that, we need a different depreciation area. We can call it Tax Depreciation. And we can have another one in a different currency or a different requirement, so we can have multiple depreciation areas.

Under each depreciation area, we have a Depreciation Method called Depreciation Key. So, there are multiple methods available to us, to depreciate. The most widely used is called a ‘Straight-Line Depreciation’, where you just take the life of the asset and divide the total cost by the life. But there are some other methods that we can also use. In that case, we will just use a different Depreciation Key for that, like declining balance and, you know, there are some others also. If it’s some asset, like the number of units you have used based on that. But most widely used is Straight Line Depreciation. So that in SAP is called Depreciation Key. So, Depreciation Area is like a book. We can have one set for our financials that we will send to the to the SEC, we have one set for that, we have one set for tax. Those are called Depreciation Areas. And Depreciation Key is the Depreciation Method. And then we can have a default life also, that we can say, okay if this is a machine, I want 10 years or 8 years. And, you know, you can define and you can also have a minimum and maximum useful life. But these are optional. And you can enter individually in each asset, or you can enter at the at the Depreciation Area of this class. So, it comes up automatically when you create a new asset. So, basically, this is a very important diagram to get an understanding of what Asset Classes are. Asset Classes like I said are available to everybody in your client. Whether you have different Chart of Depreciation or not, it is available to everybody.

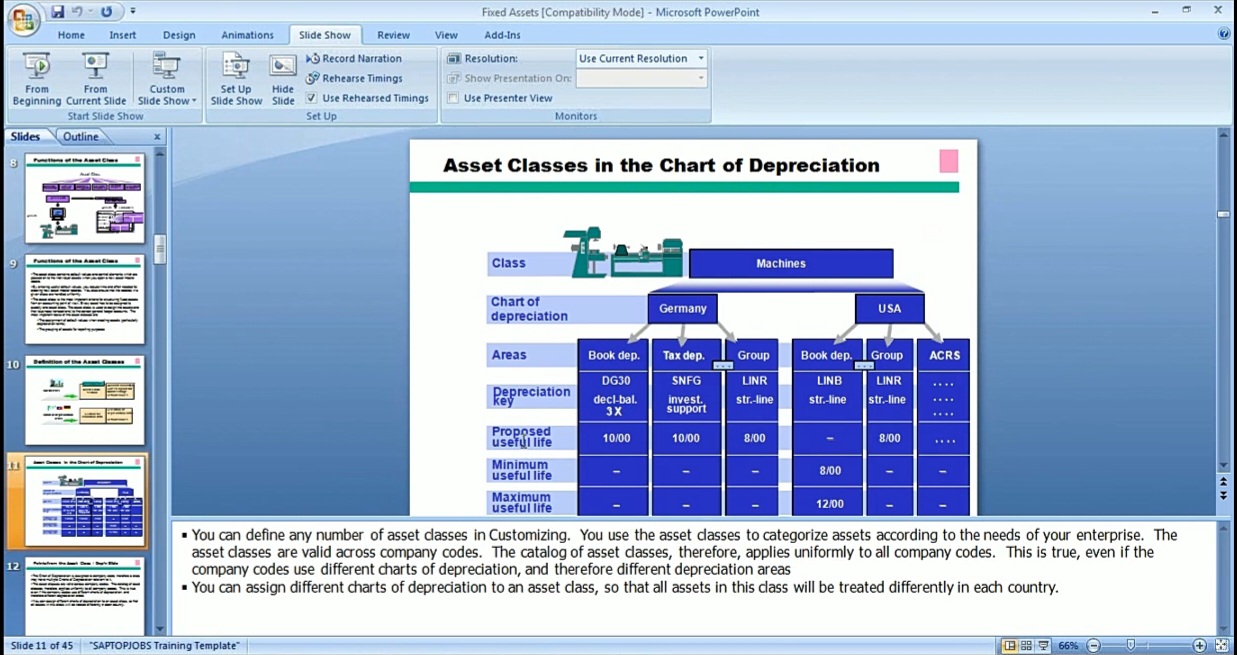

So, Chart of Depreciation is assigned to company code. Therefore, a class may have multiple Chart of Depreciation relevant to it. Just like controlling area, you have to assign it to a company code, and one controlling area can have many company codes. Just like that, one Chart of Depreciation can have multiple company codes assigned to it. The asset classes are valid across company code. This is true even if the company code uses different Chart of Depreciation and therefore different Depreciation Areas.

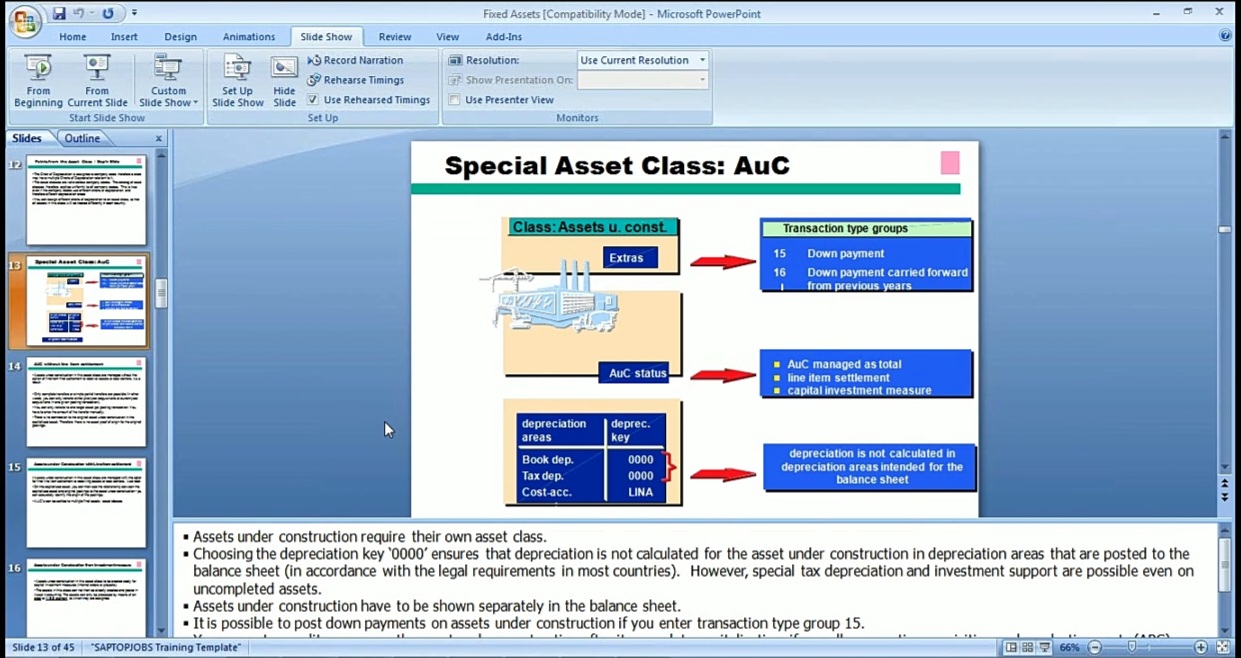

Like I was talking about Asset Under Construction, or AUC, where if you are constructing a building during its construction phase, you cannot start depreciation.

So, for that, we can have a different asset class called AUC, and we will just collect cost in it. And for that, we can use a depreciation key 000, which basically does not depreciate. You can run depreciation, but it will not post anything. So that’s why we can have a separate class for AUCs. And when they are completed, when they’re ready to be in service, then we can move the cost from the AUC GL account to wherever they belong. If they are building, if they are equipment, so we move it there so we can start depreciation. But in that asset class, we normally use Depreciation Key 000, so it does not post any depreciation for that Asset Class.

This is just talking about the settlement you want to do from your AUC as it is completed. For Depreciation Areas, you will generally need values for fixed asset for various business and legal purposes. For example, book depreciation. So, you will always need book depreciation. Others are optional, if you want separate for cost accounting and, taxation for MACRS, ACRS. So those are optional if you want, but at least you need one, which is for your book depreciation, and that depreciation will post to your GL. Other depreciation areas might not post, like tax depreciation, it might not post to your GL. It will be just for your running reports, to see how much is your depreciation under your tax area.

This is just talking about let’s say, normally, depreciation area 01 is your book depreciation. And this depreciation area will post to your ledger, to your GL. We can have 02 for tax and 03, 04 or 20, 30 for some other purposes also. But this is a requirement. Depreciation is 01 is a requirement.

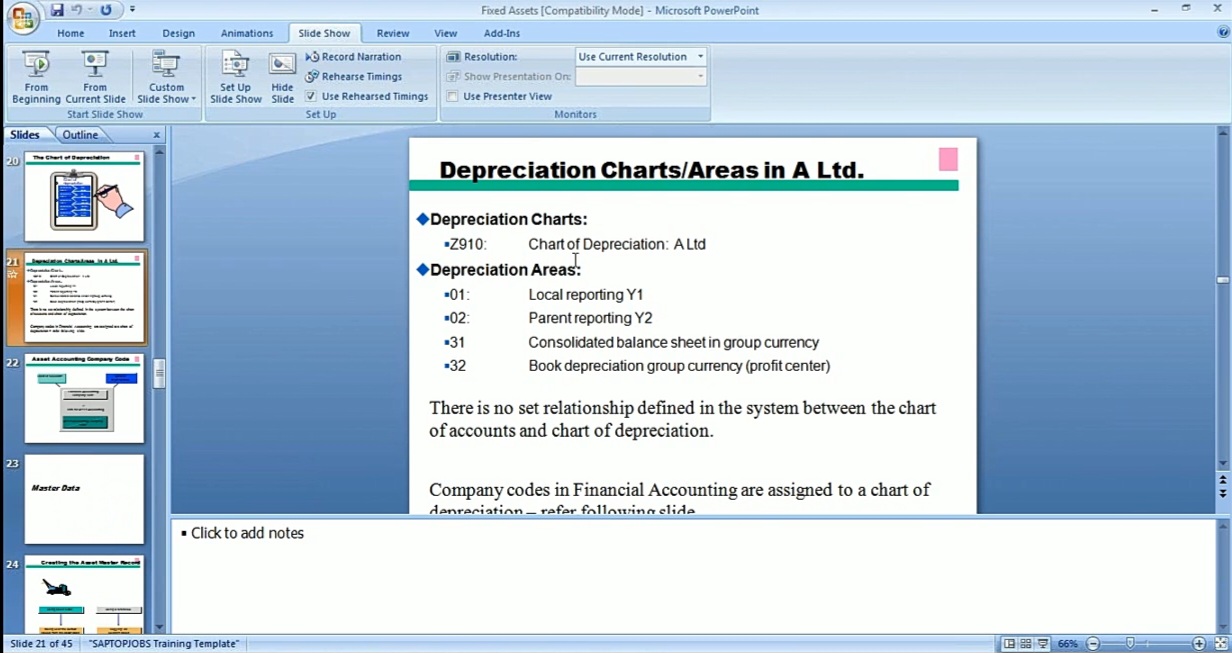

So, this is just giving you an example of how it’s doing. You have chart of depreciation, and then you have the areas; local reporting, parent reporting. So, let’s say you are a company in Europe and your parent company is in the US, in that case, your local reporting can be in your local currency, and then you can have another Depreciation Area for your parent reporting, and it can be based on the US laws. The depreciation method can be based on the US law. So that’s why it gives you flexibility to have multiple depreciation areas so you can see the result by using different depreciation types.

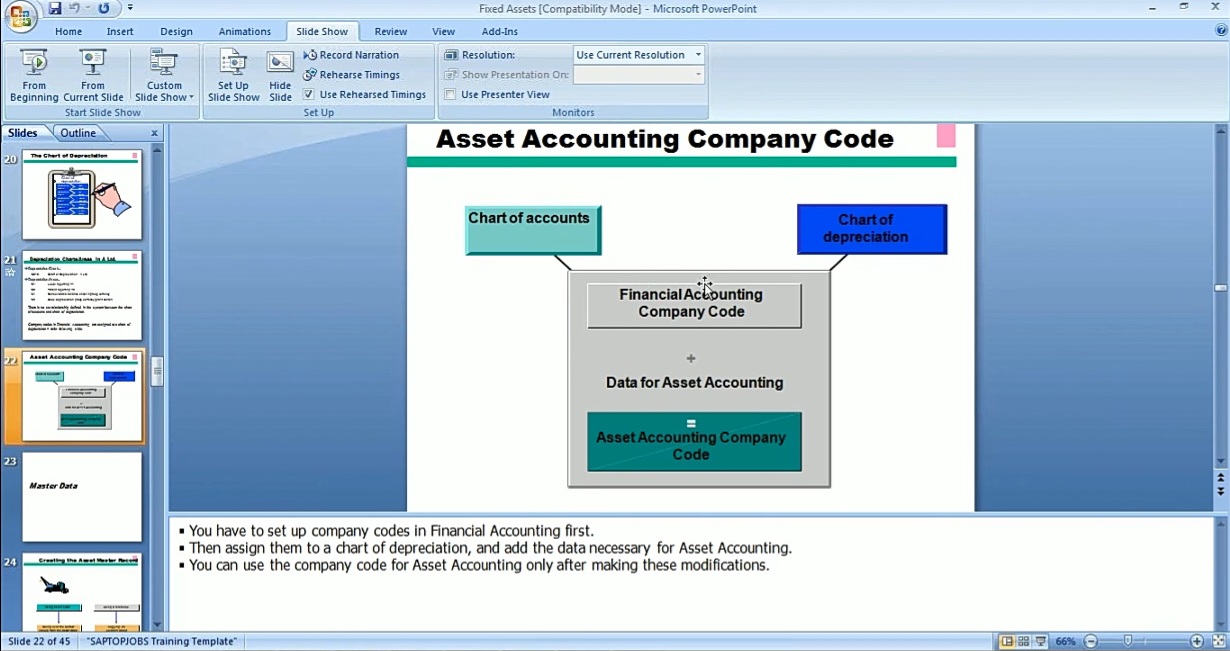

So, this is your company code.

So, your company code is assigned to a Chart of Account and also a Chart of Depreciation.

So, let’s go over to Master Data.

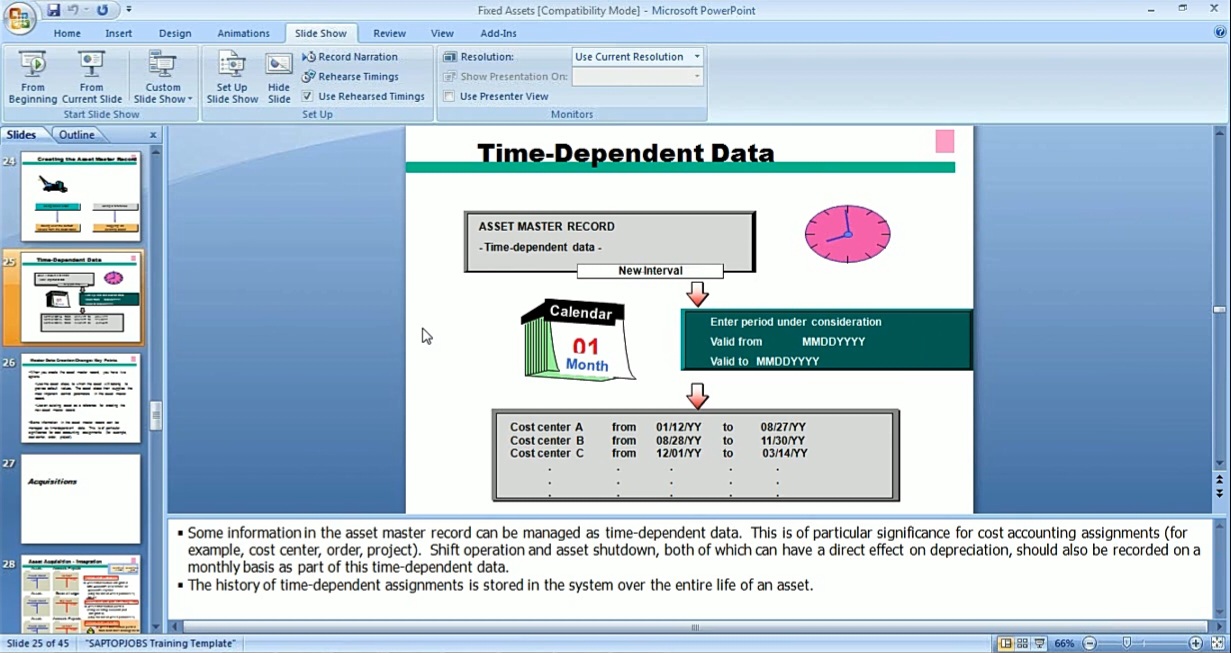

So, like we saw in the vendor, just like vendor, assets is the same thing. You can create a new asset, you can use a reference one if you want to copy some information, or you can enter a new one with new information. And in that, you need to enter a Cost Center, and this is the cost center that it will post depreciation to.

So, depreciation will be charged to that cost center that is in the master data of the asset.

This is just giving you some key points. We will use that when we will create an asset.

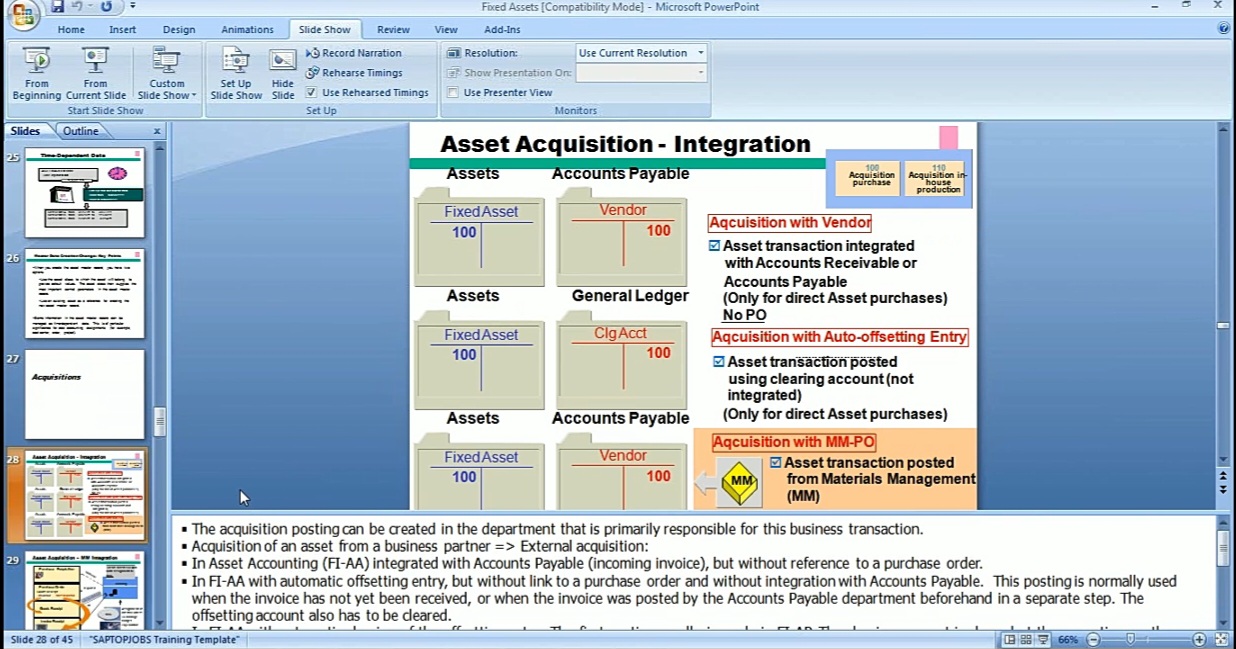

Here, it’s just giving you a diagram of asset acquisition. We can use this option, that we can post a vendor invoice and we can post that to an asset. So that like we discussed, it will debit the asset and credit the vendor. We won’t be using the other two, but we will be using this, the first step, acquisition with vendor, a non PO invoice. We’ll be using this.

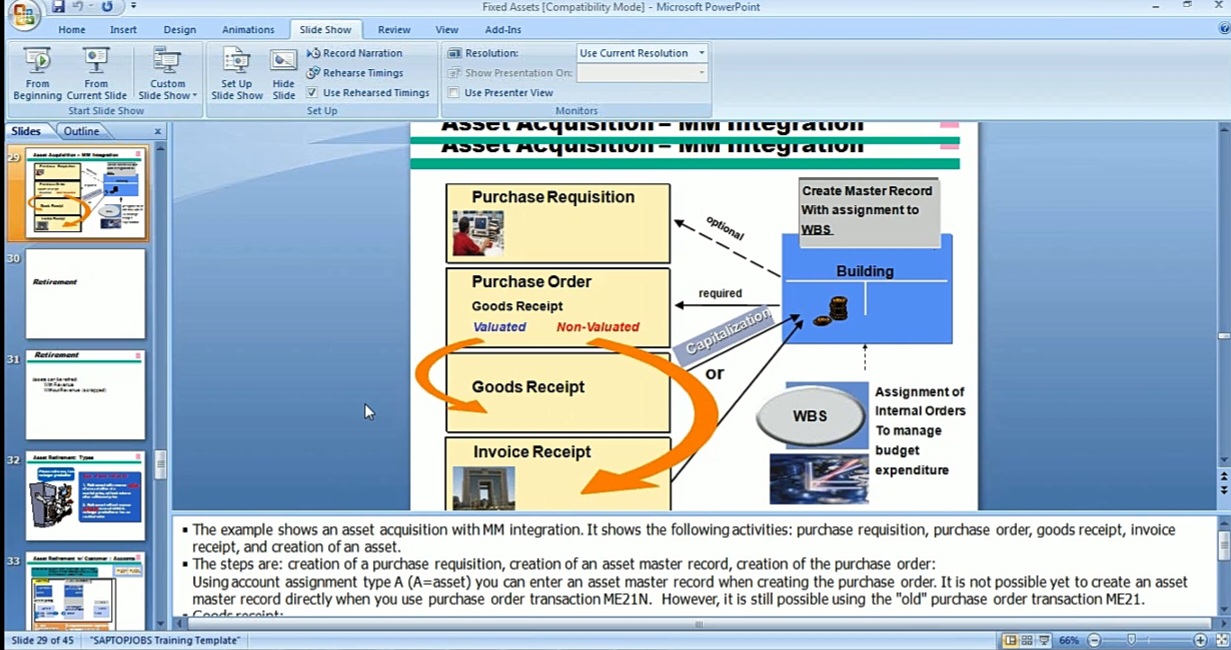

It’s just talking about MM Integration. If we have MM configured, in that case it goes through the Purchase Requisition, Purchase Order, and then Goods Receipt, and then Invoice Receipt. This is not necessarily asset acquisition, it can be true for any of the expenses also. So, yeah, this is very important diagram. Because for our expenses we did the FB60, vendor invoice. That is called a non PO invoice. But in most of the companies, they don’t want to use FB60 because there is no approval before it. So, they want to do it through the purchase order. So, in that case, there’s a different transaction for that, but the process starts within MM in that case. It starts with purchase requisition, you get the purchase acquisition approved, and then you convert that to a PO, and then you send that PO to the vendor, and then the vendor will send you the stuff. It could be an asset, it could be just an expense item, but let’s say in this case, it’s an asset. So, you do the goods receipt first, and then after that, you receive the invoice, and then you enter the invoice. So, this is true for any type of expense, whether it’s an asset or not, any type of item that you’re ordering can be, if you want to do it through the PO process, then it’ll be PR, PO, Goods Receipt, and then Invoice Receipt. So, we can do the same thing for assets also.

And we can also retire assets, one option is when they’re scrapped, when they are of no value to us, if you’re not using them like equipment when, you know, if the life is over and it’s not working, we can scrap it so we can remove it from our books. Or we can also sell them, and we receive some money with revenue or without revenue, we can also do that.

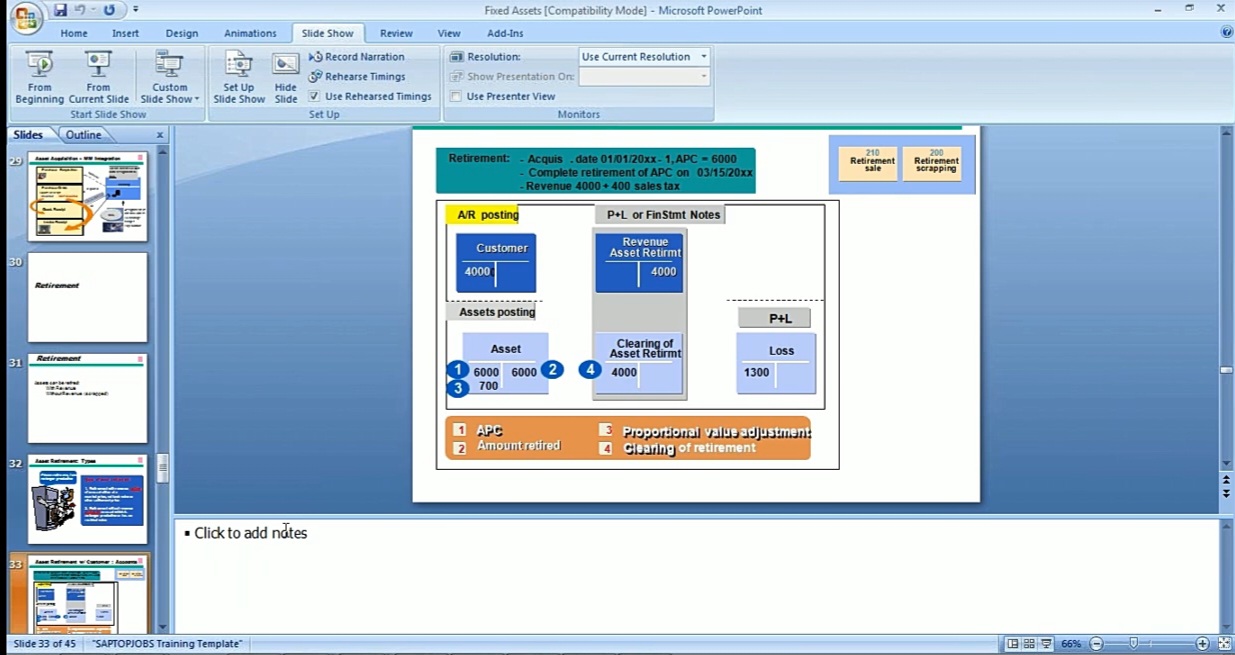

This is giving you an example of retirement, with revenue, without revenue, and we will go over retirement also. We’ll create an asset, receive it, and then we can retire to see how we’ll do that.

And then after we acquire it, then we have to start depreciation. So, when we run depreciation, normally, we’ll do Ordinary Depreciation, that is run every month. We can also have Unplanned Depreciation or Special Depreciation, if we have some circumstances that the value has gone down faster than that. I mean, normally, we don’t do that, but there’s an option to run Unplanned Depreciation also or Special Depreciation. But we’ll be covering the ordinary depreciation run that we will do. And like I mentioned, Depreciation Key is like, it’s a depreciation method. So, each method has its own deprecation key, and that we can choose for our assets.

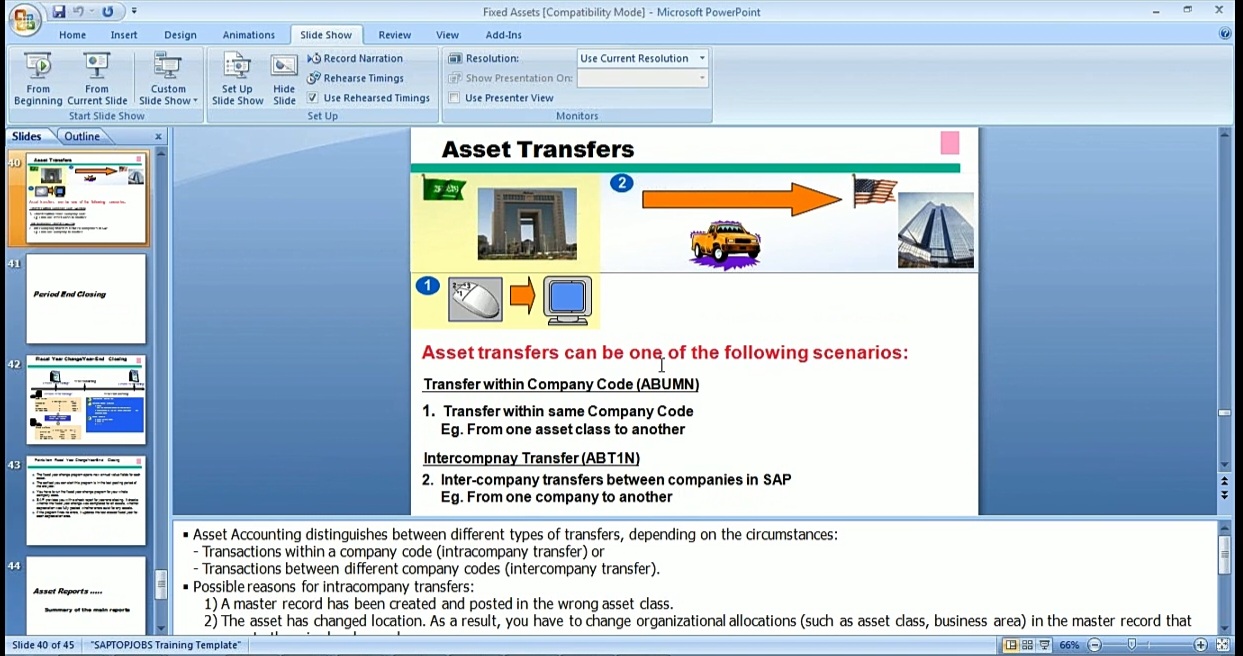

And this is giving you how it calculates, based on the date when we received the asset, and based on that date, it calculates that. We can also do transfers. You know, one reason is that we want to transfer, let’s say we booked one asset to the wrong asset class. In that case, we will have to transfer it to the correct asset class. Or if we moved an asset from one of our companies to another company, in that case also, we will need to do an asset transfer. So, we can do asset transfer within the company code or outside a company code, and these are the other two transactions.

Within a company code transaction code is ABUMN, and outside the company is ABT1N. Normally, you know, this is a transaction that is used a lot to move assets.

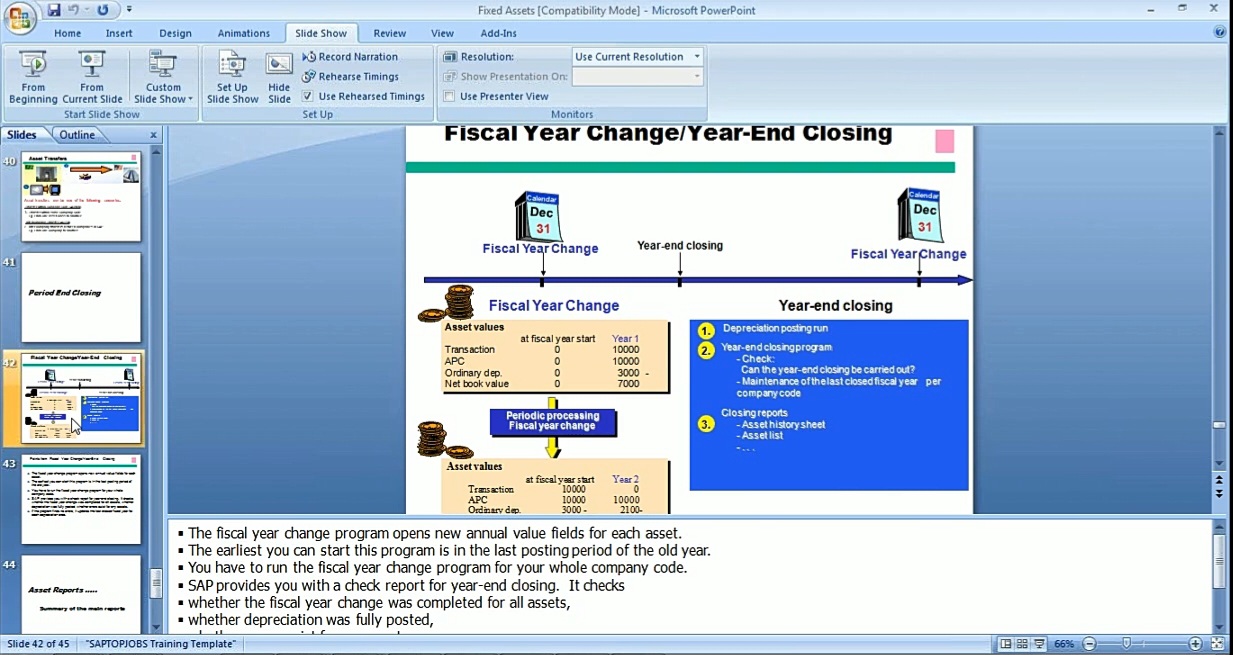

So, in Period End Closing, there are a couple of transactions that are done end of the year.

The next year is, we have to do a fiscal year change when, let’s say when we are at the end of 2010, we will have to do a fiscal year change for 2011. And so, the values can be transferred. And so, the fiscal year change is done before the year end close. That’s one transaction we have to run. I’ll show you when we will come to that.

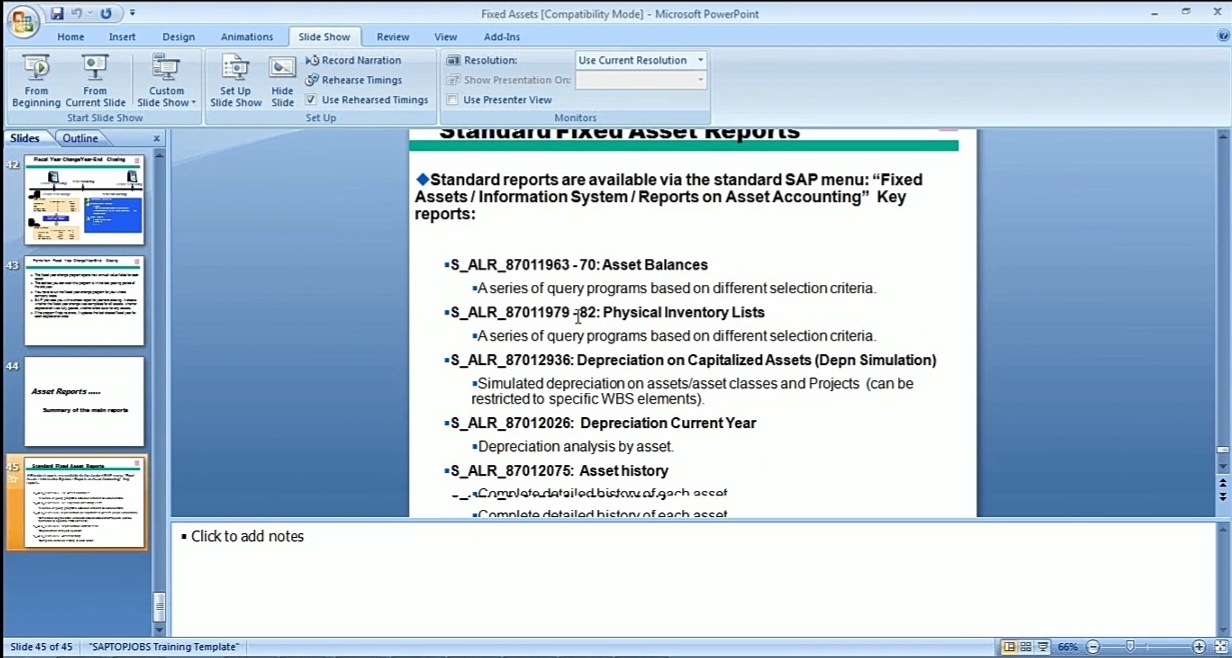

And there’s some asset reports we will run for our assets, and these are the names of some of the reports that we can run.

And so, this basically is a basic overview of what we will do in fixed assets.