Bank Reconciliation Statement 1

Now next, we’ll take up bank reconciliation statement. Again, bank reconciliation statement I think most of us have studied it in BCom long back. We don’t even remember the the full form of the BRS also. So BRS means bank reconciliation statement. First of all, my first question is, why do I reconcile bank account at all? What is the necessity for reconciling bank account?

Thank you for reading this post, don't forget to subscribe!Now, statement we used to call bank book and bank pass book. So previously, we used to use bank passbook. Nowadays, of course, we don’t maintain any passbook, banker will send us the bank statement. Anyway, we are not going to maintain any cashbook for bank. So here, in case of real scenario, what we do is, there is a book maintained by the company that we call it as cash book. We can call it a cash book or bank book. Cash book is maintained for exclusively cash items. Bank book means the checks that are issued by the company. Now as per your bank book, all the bank transactions are routed through this bank book. Forget about your electronic statement, every transaction of check issued or RTGS or bank transfer, everything will be routed through that bank book. At the same time now, there’s a bank statement. Bank book is the bank transactions maintained by company itself. Every bank entry, the checks received or checks issued will be routed through this bank book maintained by company.

Now bank statement. This is maintained by bank. Nothing but our transactions, banker will give you statement, as on 31st October, your balance available is this much. Now when you compare the balance given by the banker and the balance that you maintain as per your bank book will never tally, will never match to each other. Why? There are several reasons for that. The main reasons are:

- Cheques issued by company and not debited by bank: Say for example, as soon as we issue a check, what do we do? We credit it. Credit means in our bank book, vendor account return to bank account. This means immediately the amount will come down from whatever the balance that you are filling it. Now if you see the same entry here, it takes a minimum of 10 to 15 days for the bank to record this transaction. The cheque, say for example, if you are going to issue a 100 rupees cheque issued by company, now immediately I’ll reduce 100 rupees from my bank balance. But similarly, in the bank statement, it will not be reflected. Say, if I’m issuing this cheque on 20th of October, on 31st of October, the check whatever I issue to my vendor, he has to deposit into bank, that has to come to my bank account. There they have to debit my account, then they have to send the funds. It takes a minimum of maybe 1 week to 10 days. So there is a difference between balance as per the bank statement and balance as per my bank book.

- Cheques deposited by company but not credited by bank: Here, what I do, whenever I receive any cheque from my customer, I deposit it. As soon as I deposit it, what I do, I’ll be debiting it. Means, I’ll be increasing my balance, bank balance will be increased. So the cheque, whatever I deposit, that has to go to my customer account. There that amount should be transferred and it should be credited to my account. So it takes maybe 1 week or 10 days. So until then, it will not be reflected in the bank statement.

Not only that, one more thing. Say, for example, the banker directly debited certain expenses, say bank commission or some other expenses, on behalf of that he is incurring, he debits and I don’t have that information. So what should I do? I’ve not yet taken bank charges into my books of account, so that’s why the banker will be debiting it, but we don’t take that into the books of accounts. So these are the reasons which makes there is a difference between bank book balance and the bank statement. So we need to reconcile it. When you reconcile here, I’m taking only one cheque here, one cheque received, one cheque payment. But in real scenario, you’ll be issuing hundreds of cheques receipts and hundreds of cheque deposit from your customers. So how many cheques that we have deposited have been cleared and credited to my account, how many cheques which we have issued to the vendors are cleared and debited to my bank account, all those things will be given in the bank statement. And I need to prepare at the month end what are the cheques issued but not debited to my account, cheques deposited into bank but not yet credited to my account. So out of 10 maybe 5 cheques are credited, out of 10 cheques issued, maybe 5 cheques that are debited to my account. Rest of the things are shown as cheques issued but not debited, cheques deposited but not credited in that list. Finally, we’ll be reconciling the balance between the bank statement and the bank book. And during this process, so many entries which we have not taken will come out, then those entries we’ll be booking it. Here, a bank reconciliation statement is nothing but balance as per the bank as on, say for example, on 31.10.2013, balance as per bank book means the book maintained by me is 1,000 rupees.

But ultimately, at the end, the balance as per the bank statement is, say for example, 1100. Then what is the difference? The difference is nothing but cheques issued but not debited in the bank statement. So I’ve issued cheques, 500 rupees worth of cheques I have issued but they’re not debited. So what should I do? In order to arrive at the balance, I have to add it. Similarly, cheques are deposited in the bank but not realized, say 300 rupees. In my books of accounts, I have already taken that is added already. Since I have added, that balance is not matching, that’s why here I reduced it. Similarly, bank charges directly debited by the banker, 100 rupees. So here, the banker has sent me a statement stating that, boss, this is your balance, that is 1100 he told me. Now then I have finalized. Why’s there a difference? Because as per my books, it’s only 1,000. How is it 1100? So finally, when I have taken all these things, now this is the balance as per the bank statement, 1100. So add or less whatever you do, after doing that, you’ll get balance as per the bank statement. So this is correct. So these are the reasons for not reconciling the balance maintained by bank book, the balance maintained by the bank. So during this process, we come across new entries. Our entries which we have not taken will be taken to now books of accounts. And by the end of the bank reconciliation statement, we prepare a statement, cheques issued but not debited. Similarly, cheques deposited but not credited to our account, and that list is going to be prepared. Whatever I have discussed is business process. Now this we can configure even in SAP. Again, here, we have two things, one is Electronic Bank Statement (EBS), the other one is Manual Bank Statement (MBS). Now what is electronic EBS and what is MBS? Actually one more thing here, it is not necessarily all the issue of cheques, it may be RTGS or maybe bank transfers. Even now so many companies are using issue of cheques etc because they want to buy some time. If I’m going to transfer funds, it’s a huge funds, I can transfer as per the agreement. Otherwise, what I can do, to buy some time, I issue checks. Even very big companies, say, we are doing some one of the cement company support currently in our company, and customers are not transferring the funds, they’re issuing cheques only to the company. Company has to deposit those cheques and so it takes some time. So the customer is buying some time, maybe 1 week to 10 days. So that is the process. So in case of Manual Bank Statement (MBS), the banker will send you a word document with your debits and credits, the total transactions will be sent to you in maybe an Excel sheet or a Word document. But in case of Electronic Bank Statement (EBS), he’s not going to send you a Word document in a physical form. He’ll send you one text file. Once you upload the text file into SAP, the system will prepare the bank reconciliation statement and a reconciled statement it will give you. But in our practice or in our session, we cannot go through the EBS because the file format is going to be, if I’m not wrong, MT940 or CASH20. They are nothing but the text format numbers, international format numbers. I’ll show you.

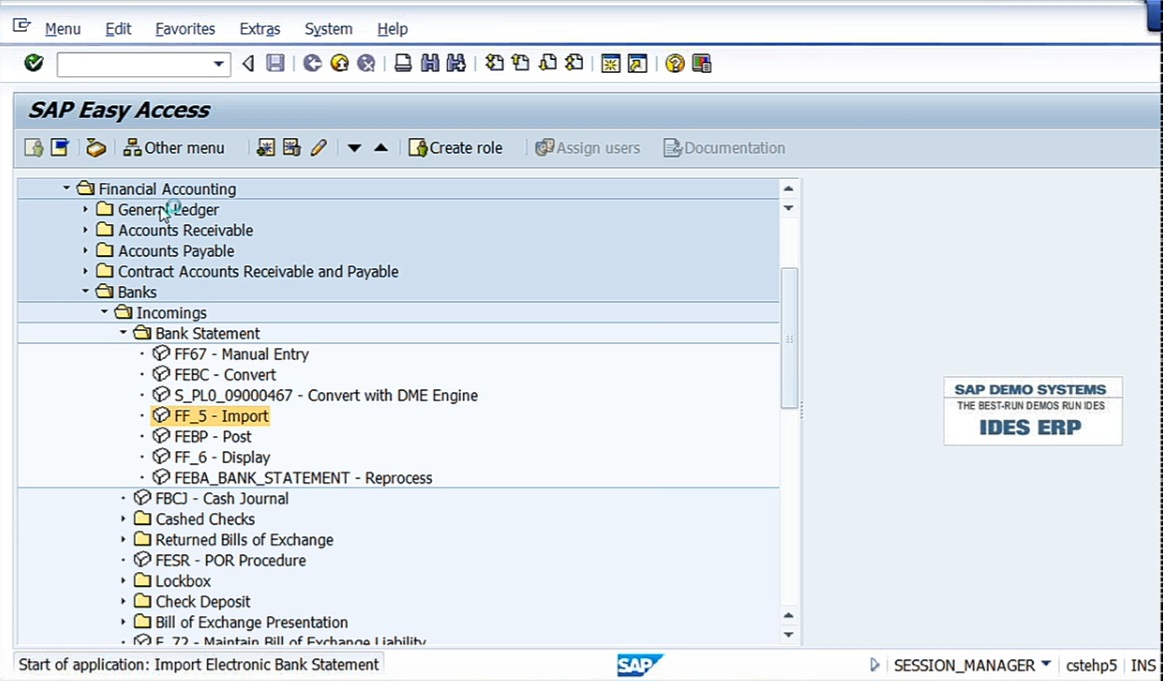

Go to SF_5 – Import. The text format has to be kept in our desktop and we have to upload it.

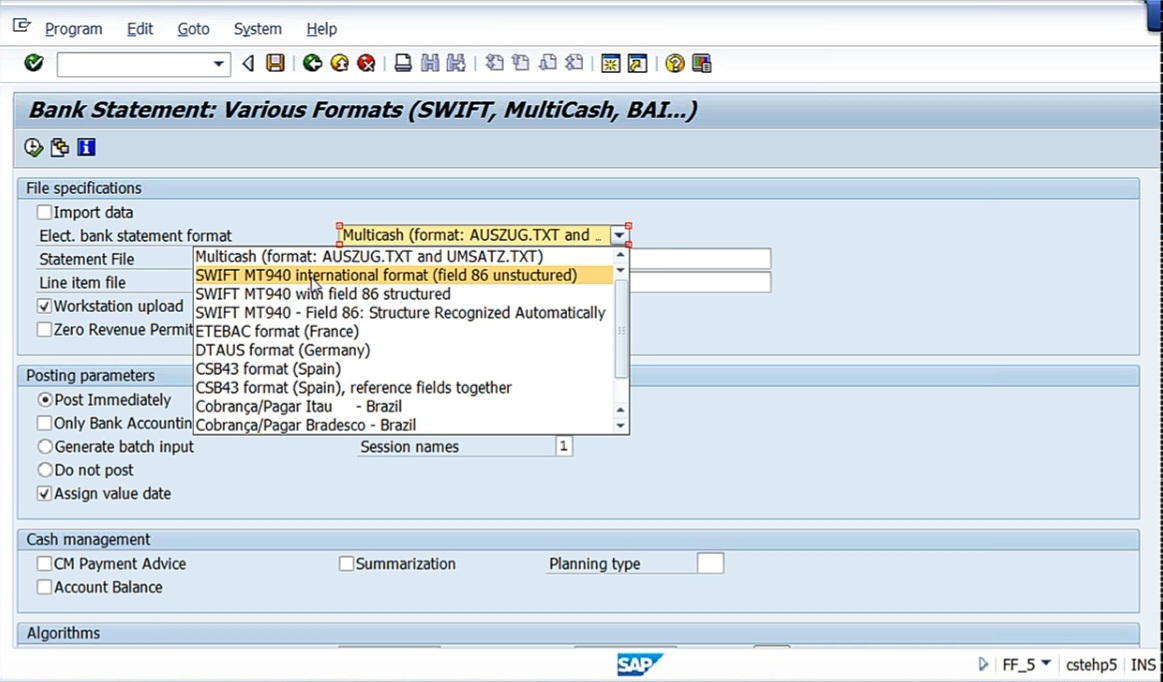

Electronic bank statement format: MT940 international format, Swift MT940 with field 86 structured, 86 structured recognized automatically. And, one more format, CASH20. So MT940 is the famous statement. So you have to use that statement of file, whatever you get, that will be kept in My Documents or Desktop, and you have to upload that. System will ask you, so from the desktop you have to pick it up. Post immediately, everything in this will be posted. So the process, whatever we are going to see now, we are going to see only MBS manual bank statement. But we are going to see the total configuration whether it is EBS or MBS. And for electronic bank statement, total configuration we’ll do it. Additionally, one or two steps you have to do for a manual bank statement, but we are going to execute manual bank statement only. So, here we have so many other steps also, but it is a bit confusing, but there is no other way for us. You need to first of all, you need to pay attention and then try to follow carefully. Even we have so many, configuration steps, around 7 to 8 configuration steps are there. We’ll go one by one.

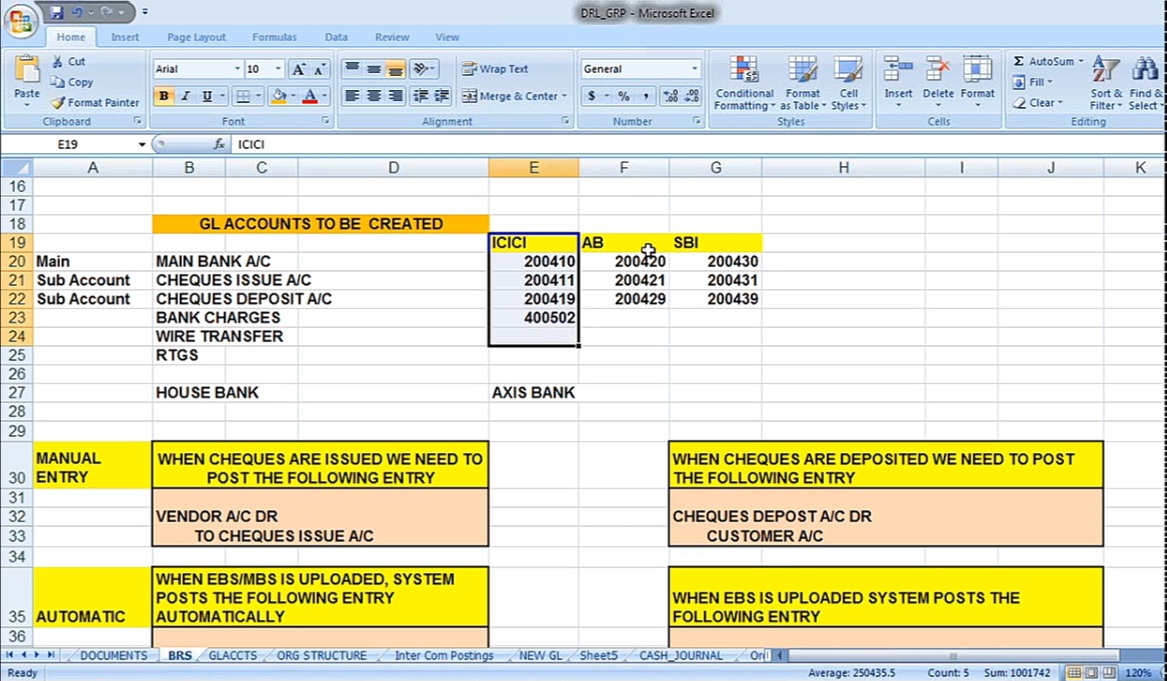

So we have to create GL accounts for the banks like this, and we need to maintain that symmetry.

This is for the purpose of at the end, we are going to create masking of GL account. What is meant by masking we’ll see later. And for that purpose, the last number should be matched to each other. Then coming to the accounting entry, when we are going to issue cheques. Say for example, cheques issue account, say we are maintaining ICICI Bank. Cheques issue account 20411.

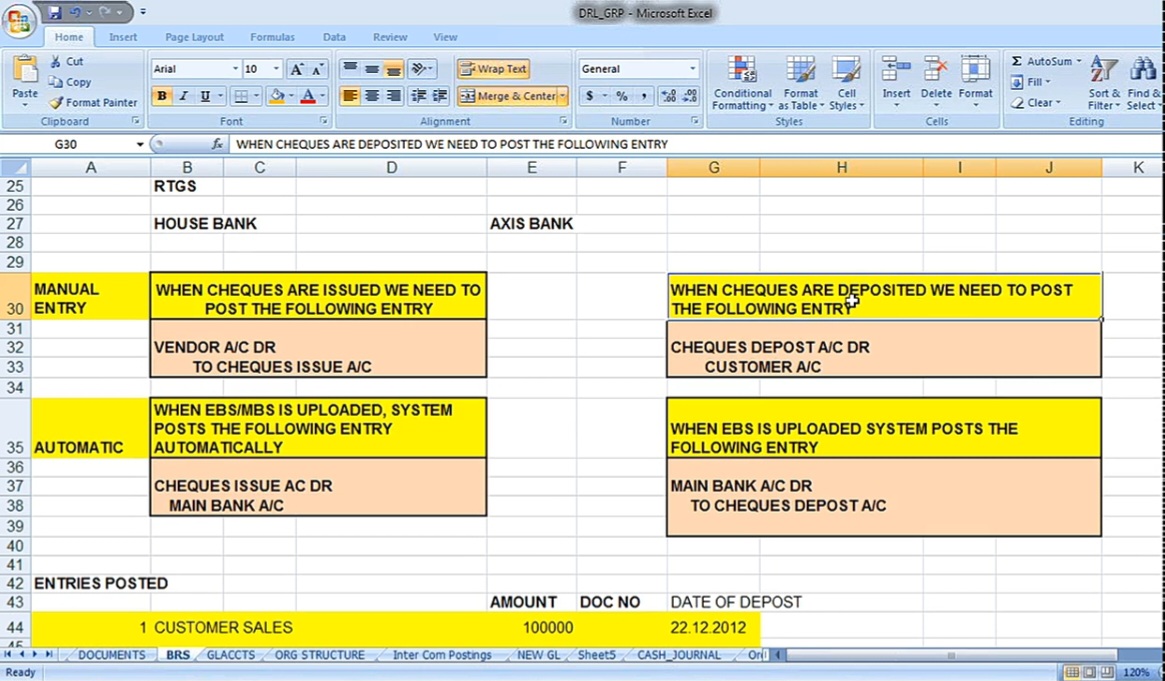

So manual entry, when cheques are issued, we need to post the following entry.

What is that entry? Vendor account return to cheques issue account. See, generally, if you don’t have this BRS concept, what we do vendor account return to main bank account, just vendor account return to bank. Now what we are going to do, when cheques are issued, we need to post following entry vendor account return to cheques issue account. Here, cheques issue account. When EBS or MBS is uploaded, the system posts the following entry automatically. What is meant by uploading? So here what we are going to do is we are going to upload. I told you we are going to receive a manual bank statement or electronic bank statement from bank. If it is a manual bank statement, I need to enter all the transactions from the bank statement manually to the SAP system. If it is an electronic bank statement, we are going to get the electronic format that is in MT940 or CASH20 or something, another format is also there. That we need to upload into the SAP system. What happens when we upload when we upload? System is going to identify what are the cheques that are already issued that have been credited, what are the cheques that are deposited that have been cleared. So all those things system will nullify and create a statement like cheques that are issued but not debited in bank, cheques deposited but not realized. That list will be prepared by the system. Whatever the list that is required for the purpose of bank reconciliation statement, we get it.

Now, when EBS or MBS is uploaded, in case of MBS, we manually enter the total transactions that are given by the banker into the SAP system. So in such case, the entry will be automatically posted. What is that entry? Cheques issue account returned to main bank. See, now whatever the cheques that has been issued here, once EBS or MBS is uploaded into the system and if the cheques has been cleared. So whatever the cheque that has been issued to the vendor, if that is cleared in the bank, that is nothing but that is debited to our account, vendor receives the money. In case the cheque is cleared, then only system will post this entry. Cheques issue account, see in manual entry it is credited. Now in automatic entry it is going to be debited, and main bank account is going to be credited. See, I told you that when EBS is not there, whenever we issue cheques, what we have done, vendor account returned to bank account. Now here also final entry is going to be the same, vendor account returned to bank account. In between, this cheques issue account has come. That is when EBS is uploaded and in case if the cheques has been cleared in our bank, then in such case, the cheques issue account will get nullified, and it will be credited to main bank. That means whenever we are going to issue a cheques, that is not going to affect immediately. That affect will come only when EBS is uploaded. That is when in the bank statement, whatever the information that is given by the banker, it should inform that this cheque, whatever you have issued to your vendor, that is cleared. So that message will come in your electronic bank statement. What are the cheques issued but cleared? If it is cleared, then only this entry will be passed. Otherwise, entry will not be passed. Entry will not be passed means whatever the entries that are not passed, the system will generate a statement cheques issued but not cleared. If it is cleared, then entry will be reversed. Means, cheques issued account will get reversed and main bank account will be credited. Means, now our amount will come down from your bank account only when cheques is cleared in our bank account. Until then, it will not be cleared. If MBS or EBS is not there, we directly debit vendor account returned to bank account, that is nothing but main bank account. But here, because we are introducing or we are making payment through the electronic bank statement. Here, we are creating one subaccount like cheques issue account, cheques issue account is going to be credited when we have issued the cheques. Whenever it has been cleared in the bank, when we upload it, system automatically generates an accounting entry nullifying this, and then it will finally credit main bank account. That is your account is going to be credited means not bank account in the bank statement credit, our books of accounts. That is amount is going out only when EBS is uploaded. This is one thing.

Second one, when cheques are deposited, we need to post the following entry: Cheques deposit account return to customer account.

So this is nothing but whenever we receive cheques from the customer, we do bank account return to customer account. But here, main bank account, we are not doing it. Here, cheques deposit account, we are debiting it, customer account, we are crediting. But when this will get nullified, whatever the cheques that has been deposited by us in the bank, if it is cleared and if you get the message in the text file that we are going to receive from the bank, if that is uploaded into the system, then system will automatically pass an accounting entry stating that main bank account will get debit only when the cheque is credited to our bank account. Now ultimately here also the same. See here, cheques deposit account is debited here, cheques deposit account is credited here. That will get nullified. Ultimately, what is remaining? Main bank account is debited, customer account is credited.

But the second entry will be generated automatically by the system only when the cheques that has been deposited is credited to our account. What happens if it is not credited? Say for example, on 25th October, I have deposited 1 cheque, 100 rupees cheque. That will be cleared. And another cheque I have deposited on 28th. That is not cleared, that is not credited to our account. Out of these two, first cheque whatever we have deposited on 25th, if it is cleared and you get the information in your MBS or EBS, and if that is uploaded into the system, then the system will pass an accounting entry stating that main bank account will be debited because debit means what? Whenever our we are going to receive money, we debit the account. And most of the non commerce student will have a very big doubt that what does it mean? Credit means we receive money, debit means we lose money. Most of you, this may be ringing in your brain. But don’t think from the bank bank point of view, think from the company books point of view. Always you have to look from company books of accounts point of view only. That is nothing but whenever we receive cheques or cash, we debit it because we debit what comes in, credit what goes out. Apply only those principles. Whenever I speak about our bank book, it means this. Bank statement means the statement maintained by the banker. Exactly reversal of whatever we do in this one. So here, whenever we are going to receive bank statement from the bank and if that is uploaded, the cheques whatever we have deposited, if it is credited to our bank account, bank statement, then in such case, system will post main bank account is debited to cheques deposit account. So, actually, when we upload, then only main bank account will get updated. Until then, it will not update. So you’ll get more clarity on this once we execute the BRS, and the system automatically generates the accounting entries, then you’ll have more clarity.

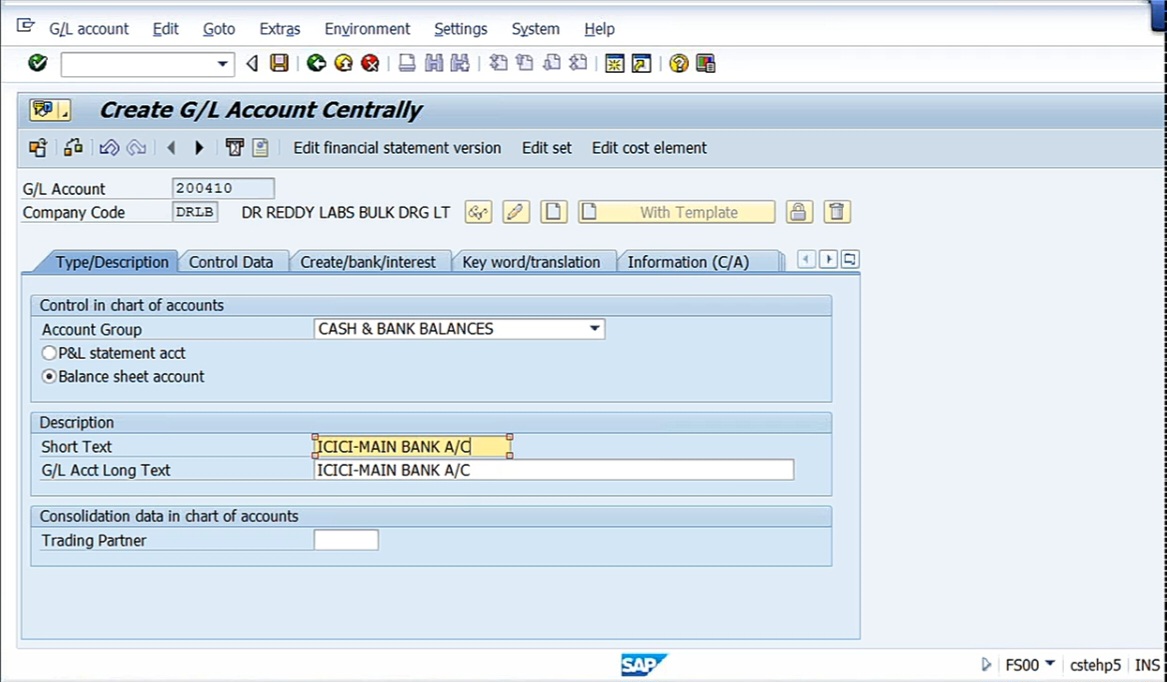

So we are going to create first a GL account. Then certain configuration steps are there that also we’ll do. So first of all, create the GL accounts. In FS00 company code DRLB. So I’m taking 200410, ICICI Bank. Cash and bank balances, balance sheet item, ICICI main bank account. Why should I say main bank account? Nothing but that is the main, because we have sub accounts, cheques issue account, cheques deposit account.

Parameters are the same: only balances in local currency, line item display, sort key 001. Under Cash/bank/ interest, field status group G005 – bank accounts (obligatory value date).

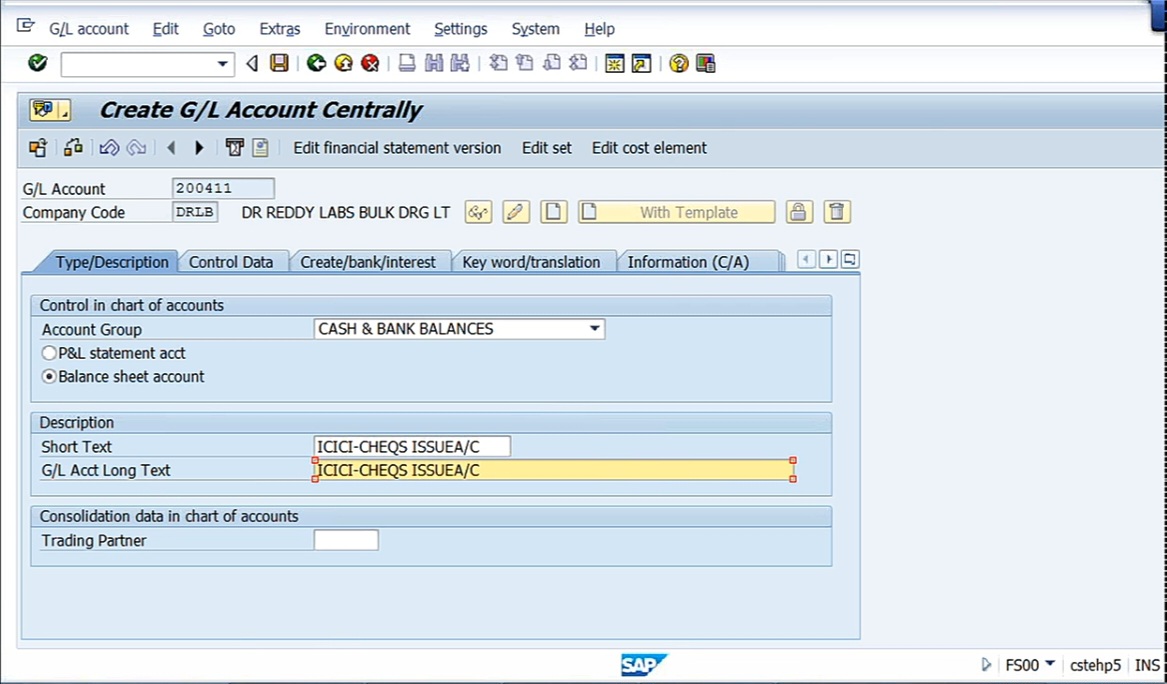

Next, 200411. Cheques issue account.

And here, one thing you have to remember is it should be open item management. What is meant by operator management? It means we are asking the system to take up the managing of the open items, we are leaving it to the system. The clearing of the open items will be done by system. Other parameters are the same. You should not forget this open item management. Without this, the system will not execute. Let’s save it.

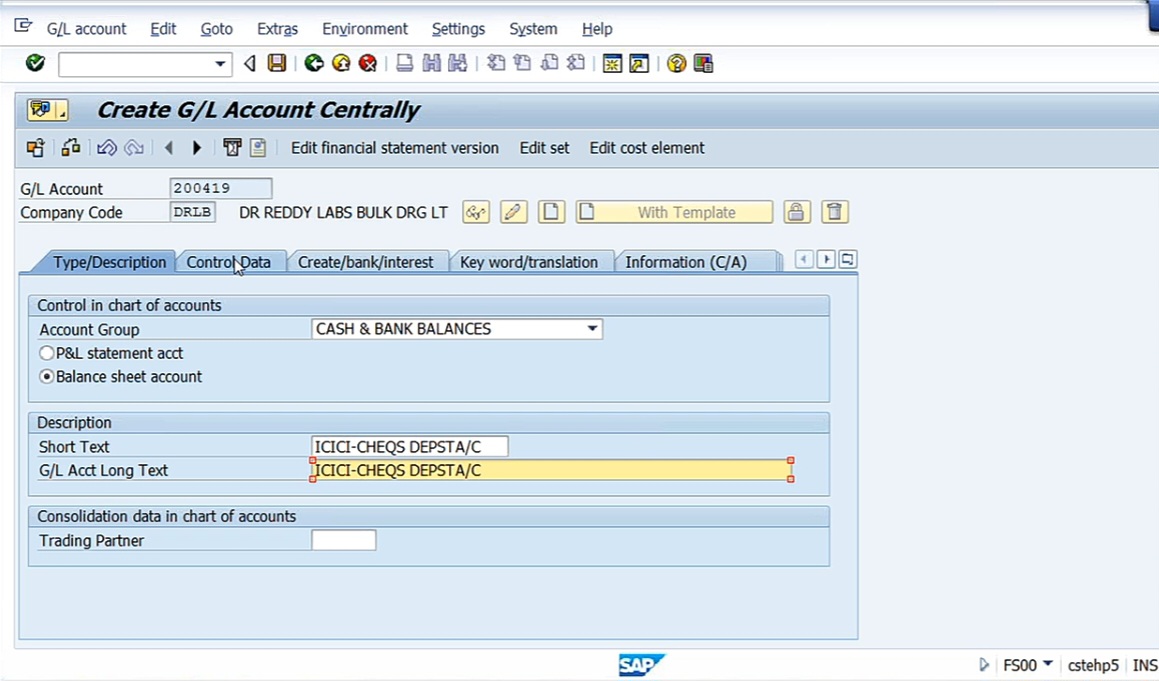

Next, 200419. Same cash and bank balances, balance sheet account. This is cheques deposit account.

Only balances in local currency, line item display, open item management. Field status group G005. Because why we have to maintain open item management is, I told you that the system automatically posts the second entry. That is whatever the entry that you post, system is going to maintain, clear the open item. That’s the reason, clear the open item, open item management. Means we are asking the system you manage the maintaining of the clearing of the open items. So management of the open items will be done by system. Then these 2 are sufficient.

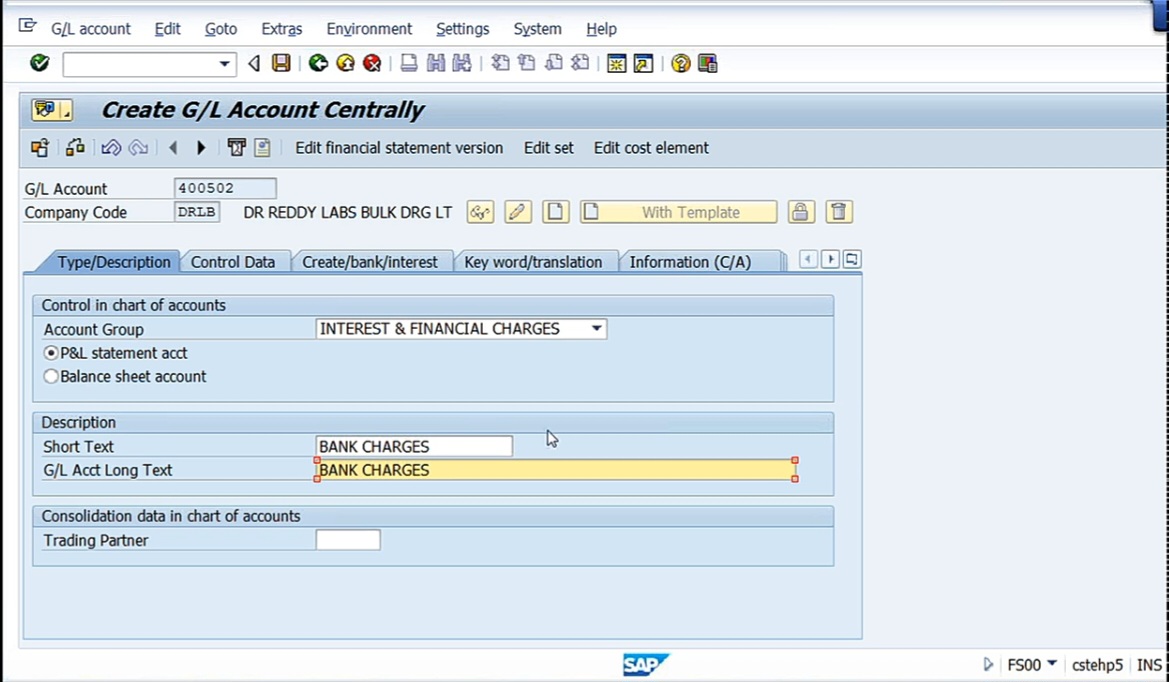

Next, I’ll create 400502. This is interest and financial charges, P&L account. That is nothing but bank charges.

Just take any other expenditure account, nothing special here. Not only balances in local currency. Check line item display, sort key 001, select G001 as field status group. So we have created four accounts for ICICI Bank.

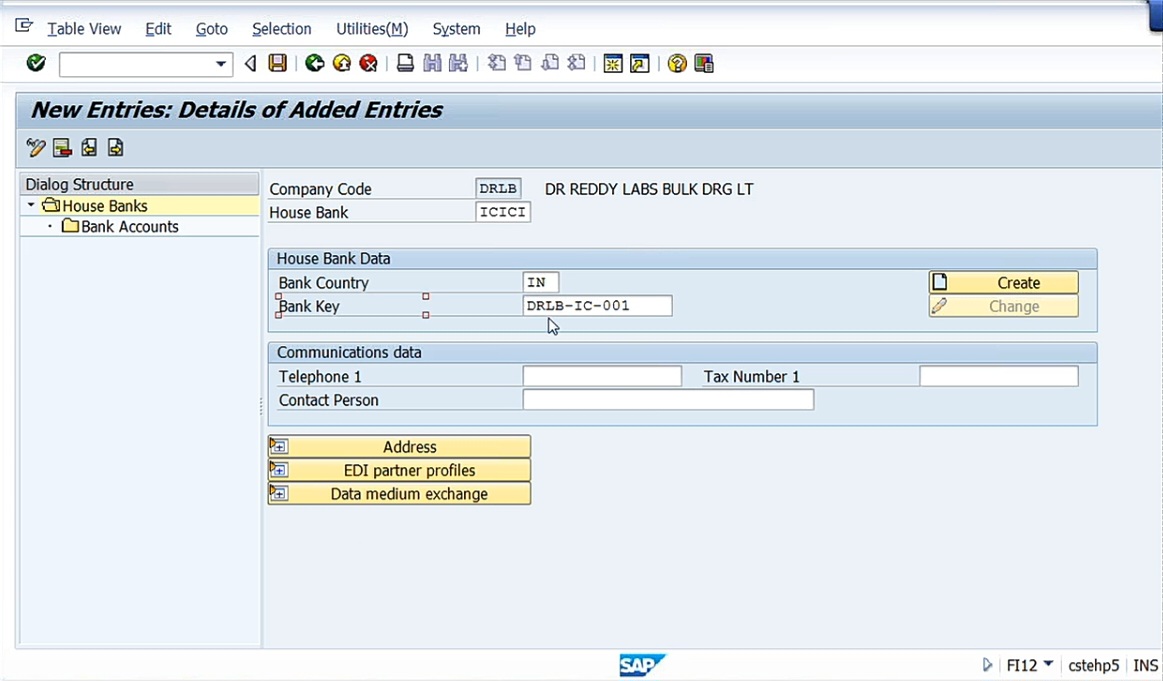

Next step, I think you know how we create house bank. We have already seen creation of house bank in case of automatic payment program. Though the number of steps are a bit more, it is not difficult, you have to execute one by one, that’s all. Go to Bank Accounting, Bank Accounts, Define House Banks. So first of all, for the main bank account, I need to create house bank. So define house banks. Company code, DRLB. So we have already created 2 house bank accounts before. We are going to create new one. Click on ‘New Entries’. House bank, ICICI. Country, India. Bank key, DRLB-IC-001. I think I can use the same number also.

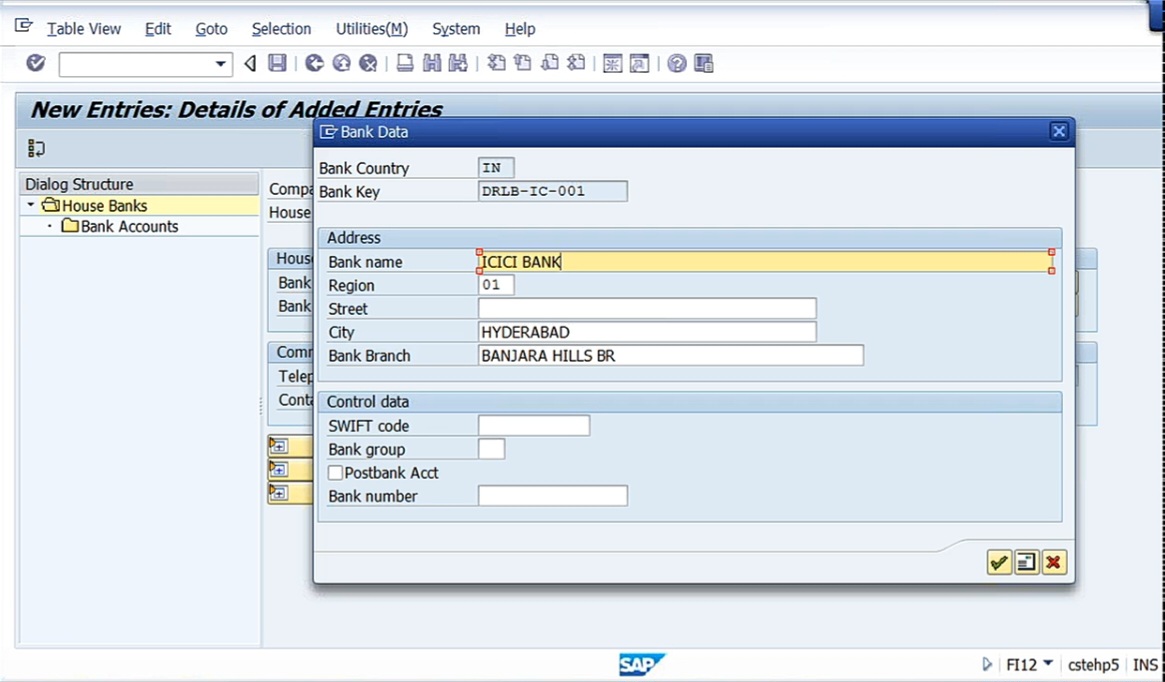

So click on create. Bank name, ICICI bank. Same branch, so Banjara Hills branch. City, Hyderabad. Region also we can take Andra Pradesh.

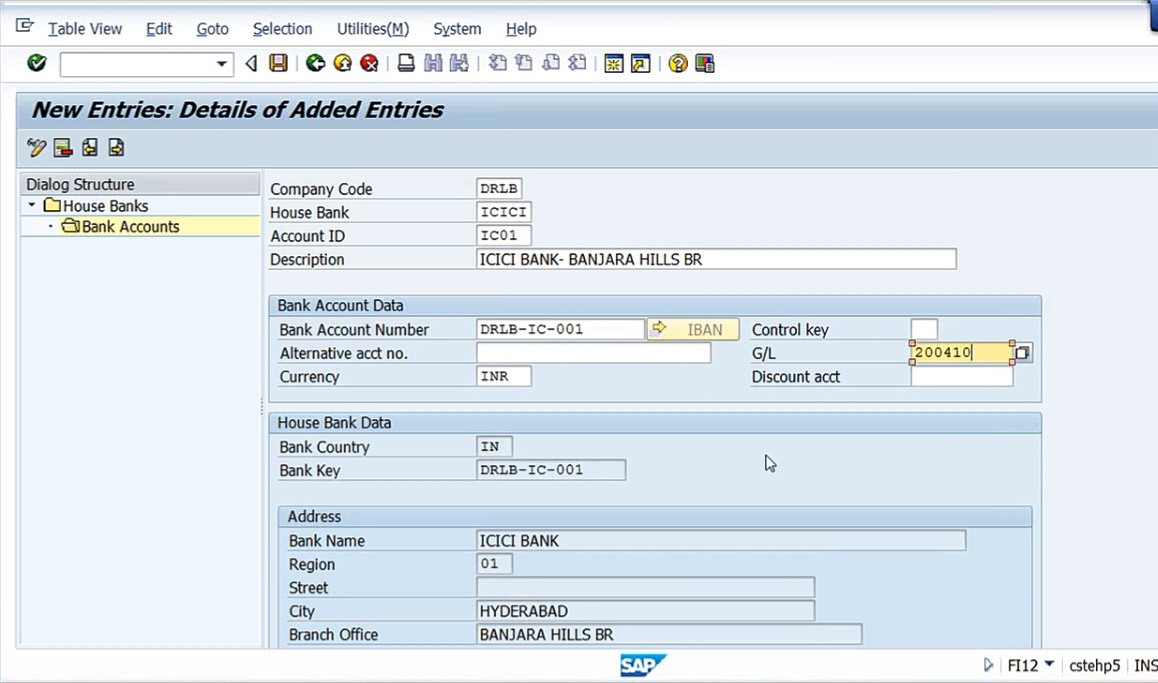

I think maybe after separation of Andhra Pradesh, we may get here a new state, Telangana, 29th state. And in such case, you know, of course, our SAP India will be observing the changes, observing the political changes, and they’ll create a new state and they will send it as a patch. So what all companies has to do, they have to download that patch from SAP, and you have to apply the patch. Then automatically, the new state will come there like Telangana. Next, go to Bank accounts,clock on ‘New Entries’. Fill account ID, IC01 see 01. Description, ICICI Banjara hills branch. So bank account number. Let’s imagine that this is the same bank. Bank account number also, same number. Currency, INR, GL account, 200410.

Save it. So we have created the house bank.

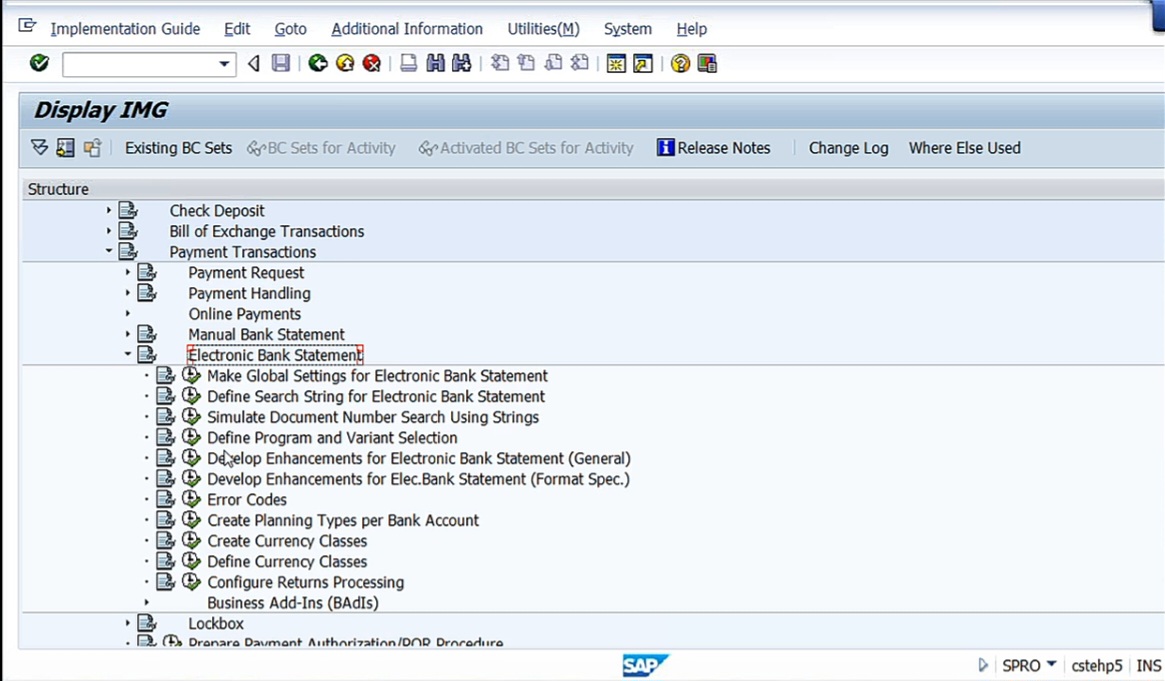

Go to Financial Accounting (New), Bank Accounting, Business Transactions, Payment Transactions. We have Manual Bank Statement, Electronic Bank Statement. First, we’ll take up electronic bank statement.

Though we see electronic bank statement, all these steps are necessary even for MBS. So that’s why after we do this one, manual bank statement, one step is there (Create and Assign Business Transactions), that also we’ll do it. So then only we can execute MBS. Because for MBS, all these things are very much required.

Here, note:

- Cheques issued out to Vendors will be credited to 200411. So whenever any cheques are issued, we have to credit it to the cheques issued account.

- Cheques issued from customers are to be debited to this account, 200419.

- When bank statement is uploaded into SAP, the following entities will be posted automatically. Whatever I have explained to you earlier, it is given.

So entry 1, for cheques issued out. Based on the cheques cleared in the bank account, the following entry will be automatically posted. ICICI- cheques issued account is debited, ICICI main bank account credit. What I told you, the same thing. So first, you need to understand this, then we can go for the configuration. The configuration, first, make global settings for electronic bank statement. So here, what I’m going to do, go to Electronic Bank Statement, Make Global Settings for Bank Statement. And here, you’ll find around 7 steps there. Chart of accounts, DRCA.

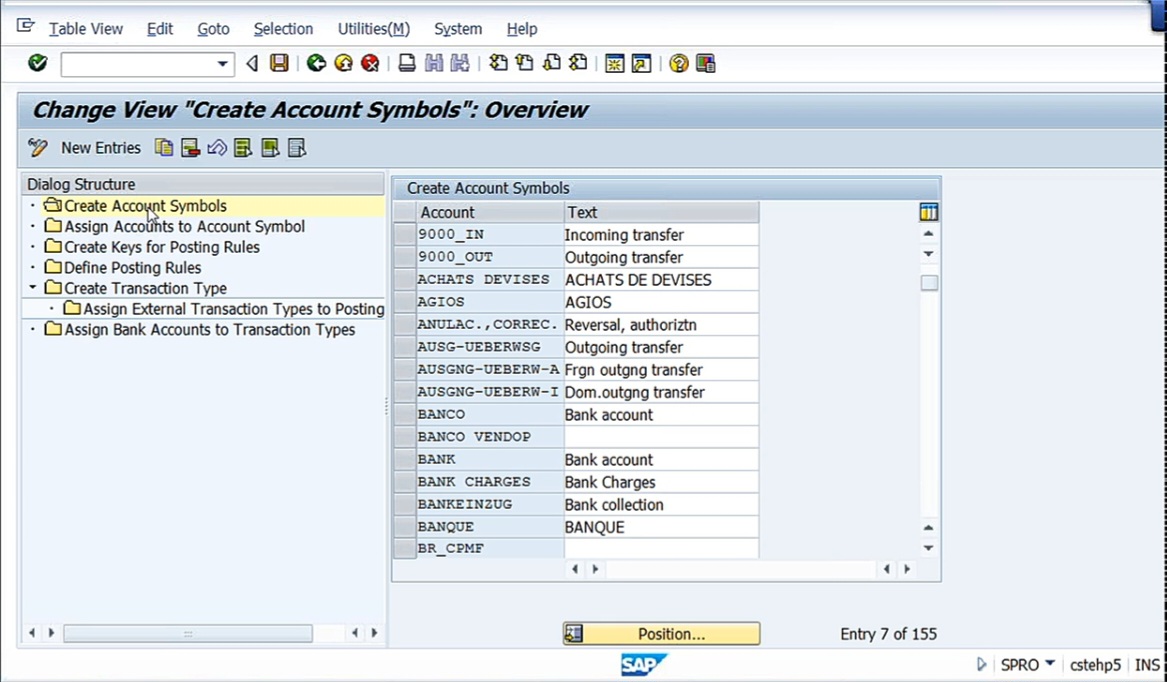

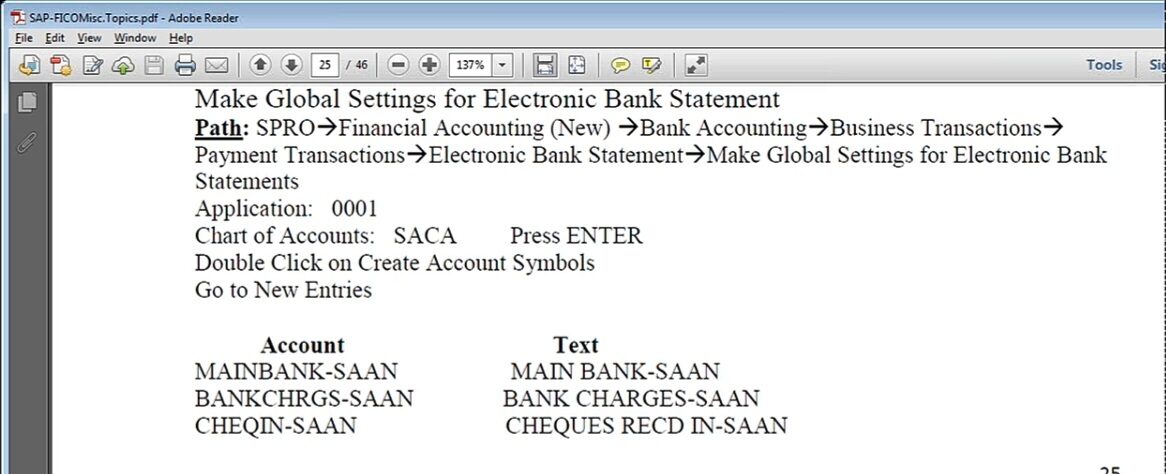

All these steps, you have to do it. So it may be a bit confusing in the beginning for you. But anyhow, let us see. Here, first of all, I need to create account symbols. What is this account symbols? See here. Here I have given you.

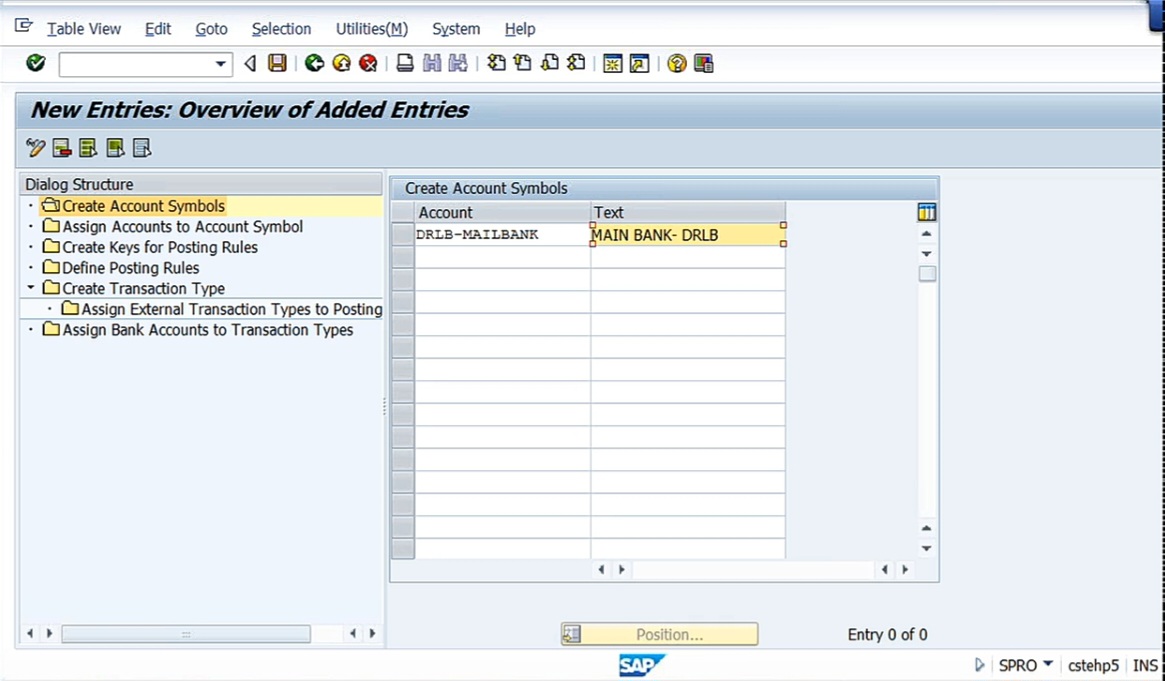

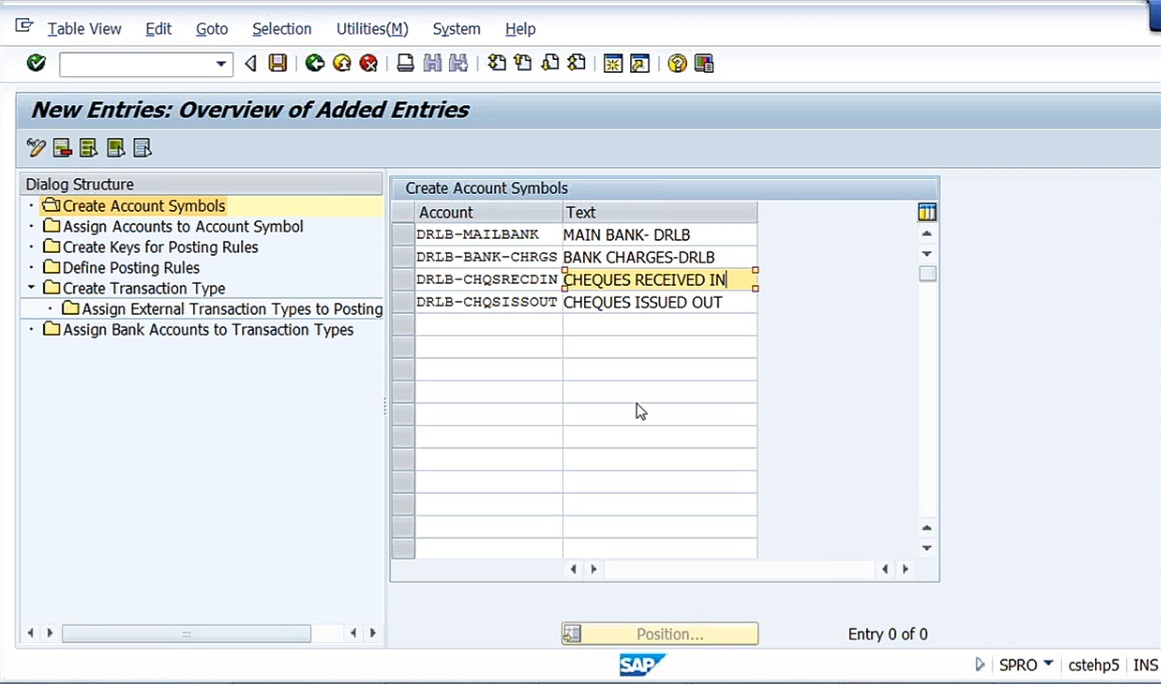

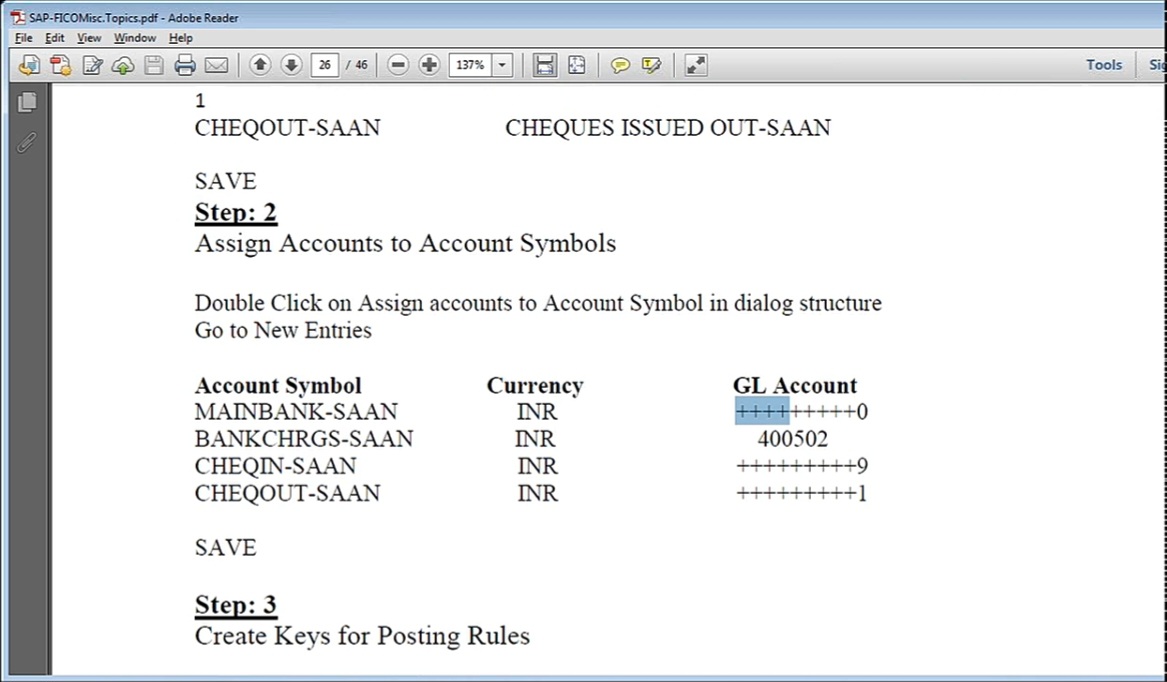

I have to create some symbols. Say, main bank account for your company code. What is this main bank? Text is main bank for that company code. Say, for example, here, DRLB. So let us give the first prefix of your company code, the main bank. Here, don’t give your bank name. Here, you can give up to 15 letters. So anyway, DRLB main bank.

Second one, bank charges, symbol for bank charges. Here, DRLB bank charges. So whatever we are creating here, this is some symbol. One is main bank account, second is bank charges account. Then we have to create cheques issued, and cheques received. So next, DRLB cheques received in. Received means whatever cheques that you receive, you deposit it. So maximum, 15 characters. Then DRLB cheques issued out.

So for 4 types of transactions, we are creating 4 account symbols. These are nothing but symbols, remember that. And if you have, say, for example, RTGS. Whenever you are going to transfer any money from one bank to another bank, we call it as RTGS, fund transfer. So if it’s a fund transfer, you have to put a symbol here. Any type of transaction, whatever you are going to find in the bank. For that, we have to create a symbol. Save it. So here we are done.

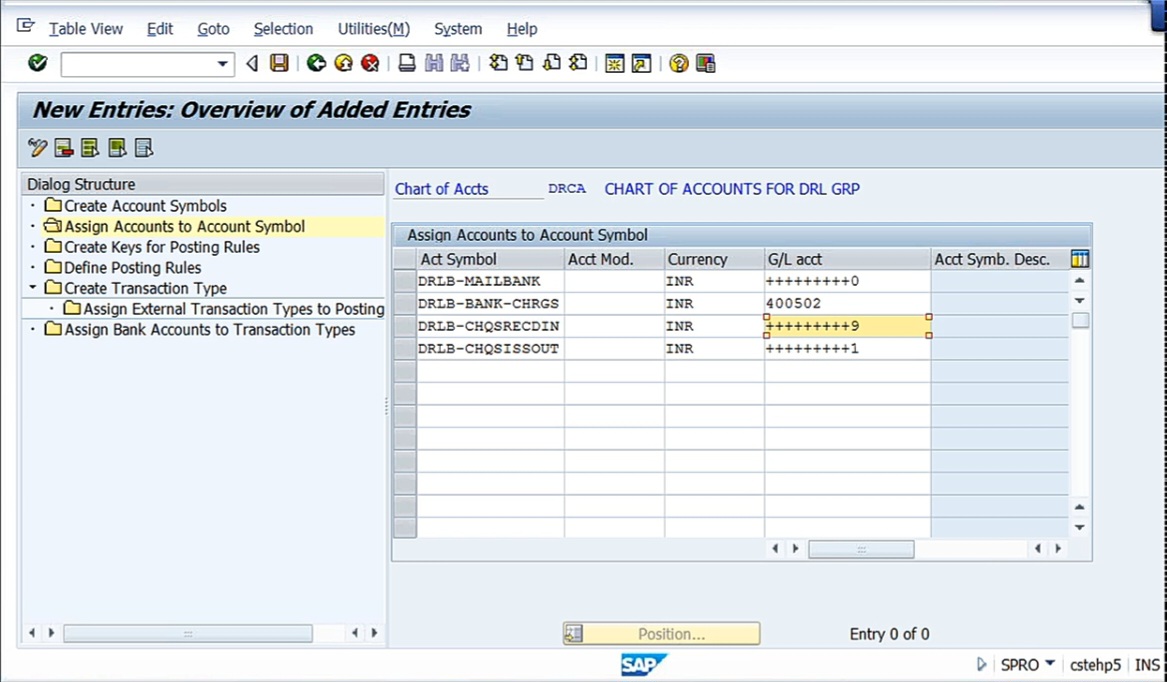

Then next what I need to do is assign account symbols. Now whatever we have done here, whatever the account symbols that we have created, to that I need to assign my GL accounts. Click on Assign Accounts To Account Symbols. Click on new entries. My account symbols are here. Whatever we have created, those things will appear here in the list to select from. Instead of what I have done already, I have copied it, so I’ll just paste it. Account method, Currency, I can say INR. Now what is the GL account to be given here? See here in the notes I’ve given you, this is called masking.

I’m giving here 091. But for bank charges for bank charges, this we call it as hard coding. Hard coding means whatever the bank it may be, the charges will be posted to this account. So anyhow, you know, main bank account. So in the main bank account, we use 10 digits. So here, you take all plus. After that 10 digit, take 0 at the end. For main bank account, 0. Because I told you, 200410, take the last digit 0. And second one, bank charges. So for bank charges, what is the GL account that we have created? Straightaway, I can take it. 400502. Cheques received in, 200411, cheques issued out, 200419. So here also what I need today is take all plus, cheques received in, nothing but 19, so 9. Cheques issued out 11, so 1.

Save it. So using of this plus mark is nothing but we call it masking. What is exactly meant by masking? Masking is nothing but say for example, here I did not mention whether it is ICICI Bank or Axis Bank or SBA or SBH or another bank. But we are creating symbols. Here, whatever the bank may be, your main bank account will be there and your bank charges will be there and cheques will be received in, cheques are received out. Cheques received out means nothing but cheques are deposited or issued out. Now here, masking means whatever the bank it may be, it will these symbols will work for all banks. Otherwise, what happens, you know, if you want to create say for example, I have 6 banks. Out of 6 banks, 6 into 6, 36 combinations have to do here. Instead, what I’m telling to the system, I’m masking it. I can use any bank. Depending upon this one, whatever the bank account you take, system will create EBS, that is nothing but electronic bank statement we get from the bank. We can reconcile it. In case if you want to use these symbols for each bank separately, then there’s a hell of a job. For each and now if you have 6 banks, 6 into 6, so 36 symbols you have to create. So that’s why that is a big task. That’s the reason we are creating only one set of symbols. This is one set. That is done.

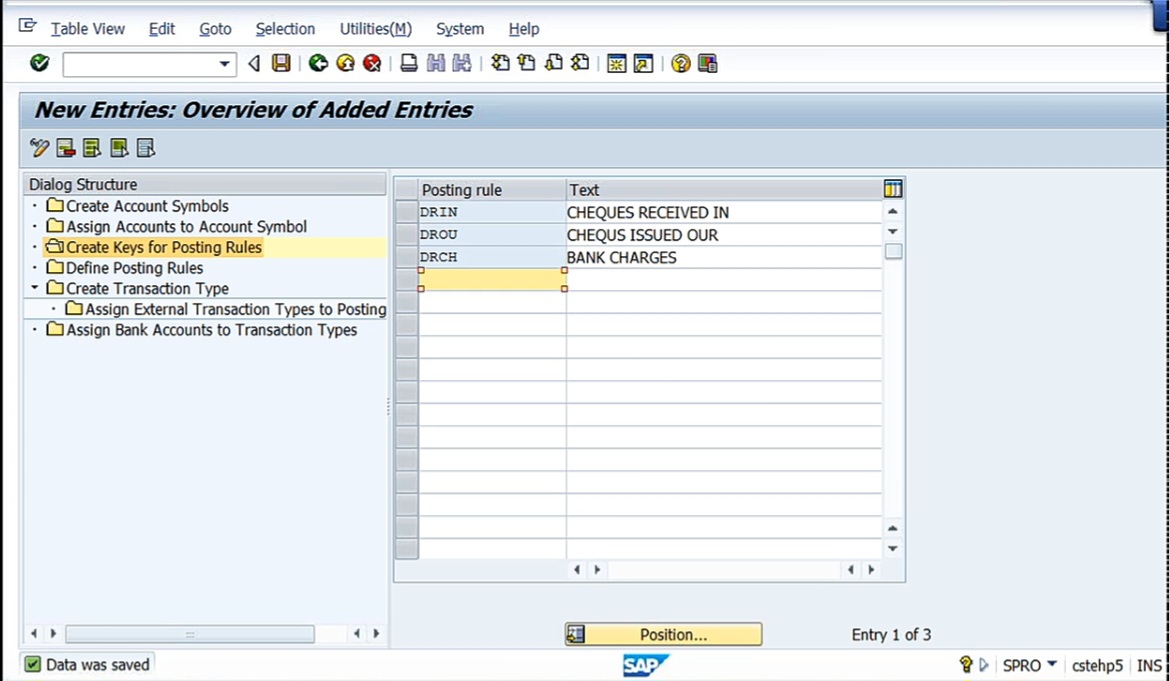

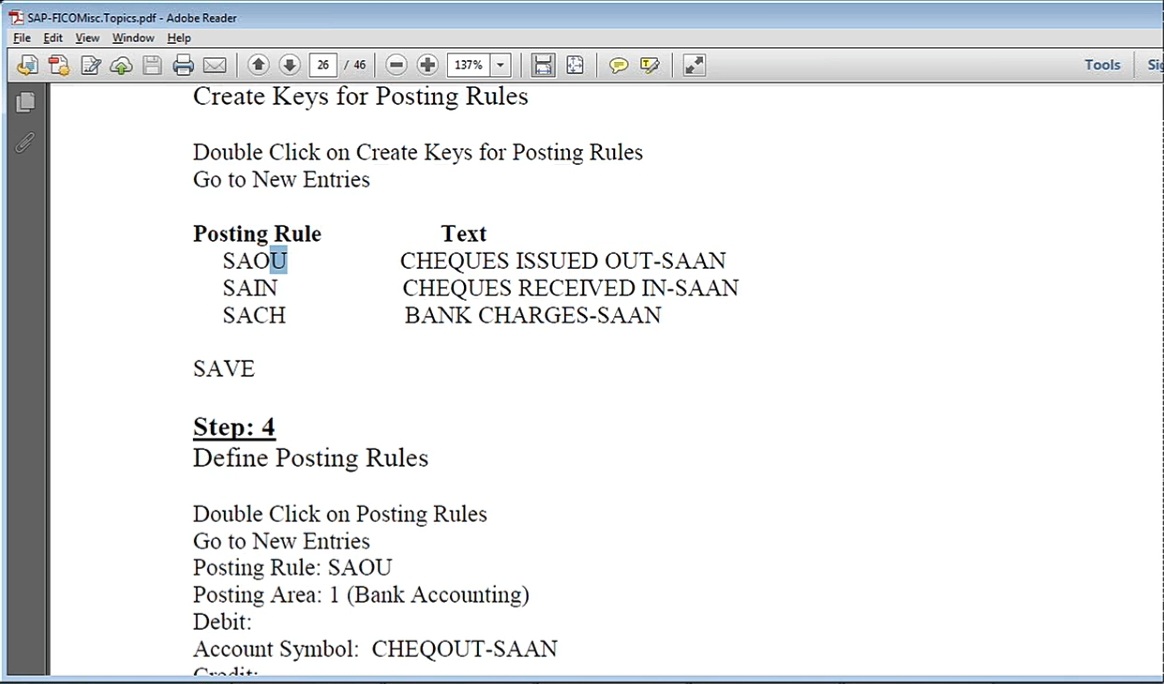

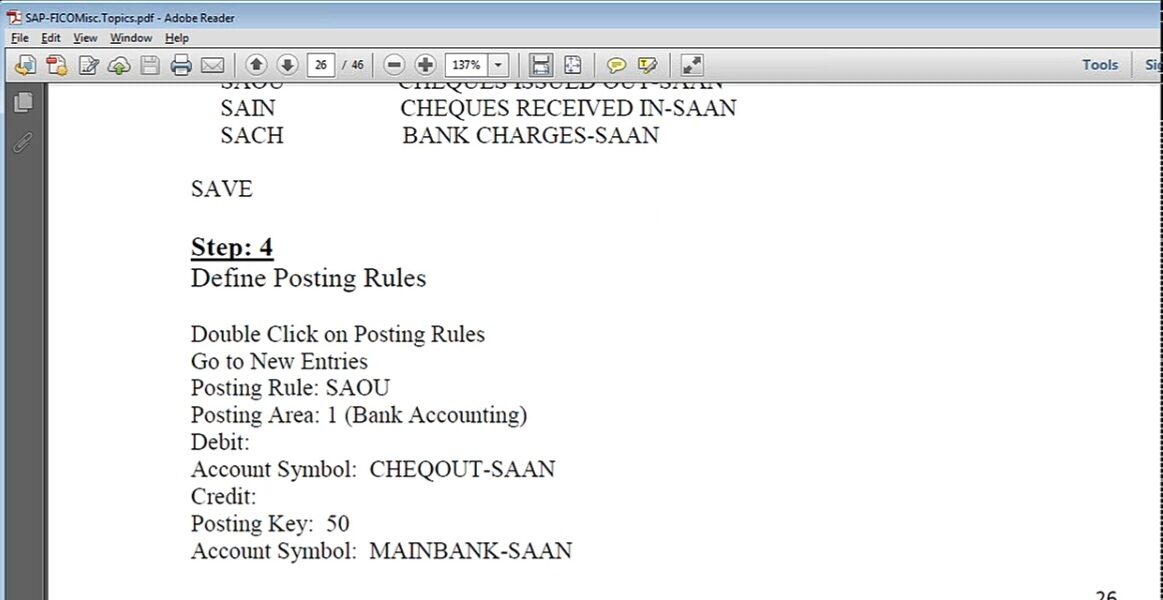

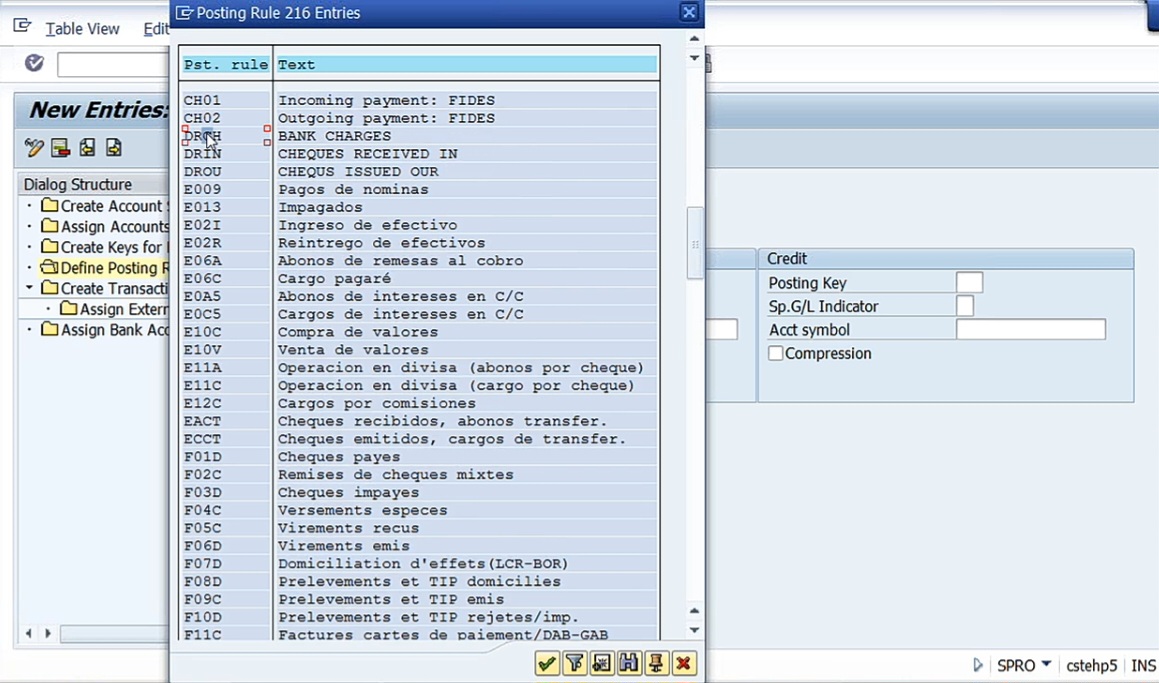

Next is Create Keys For Posting Rules. Here, posting rule is nothing but see here, when cheques are issued out, when cheques are received in, when bank charges are posted, for all these things, we have to create certain rules. What rules? Because I told here, whenever we are going to upload your EBS or MBS, if there is a cheques issued out, you should get this entry automatically. Because at the time of issuing the cheques, we manually, we post this entry and system is going to automatically post this entry. For that purpose, posting rule, what entry should be posted? That posting rule I have to create. But before that posting rule, I’m going to create just a rule name. Here, rule name is cheques issued out, cheques received in and bank charges. For these three, I have to create rules. After going to the Create Keys for Posting Rules, click on New Entries. I have to create my own rule. What are the rules? The rule is nothing but one, 4 digits. Here, it cannot take more than 4 digits. The first is nothing but DRIN, means cheques received in. DROU means cheques issued out. Then coming to DRCH, it means Bank charges. Save it.

Some rule names I have defined here.

SA is nothing but company code here. SAOU means cheques issued out. SAIN means received in. And the SACH means bank charges. So in the text here it is given.

Then here, posting rule we have defined here.

And how it has to work? Means, say this is the symbol. Say, when cheques are issued, cheques are uploaded, when EBC is uploaded, what is the accounting entry we should get? Whether it is a cheques issued, account should be debited, main bank account is credited. When main bank account is debited here and cheques deposit account is going to be credited here. Like that, what is the accounting entry we should get, so that we need to carefully plan the accounting entry here.

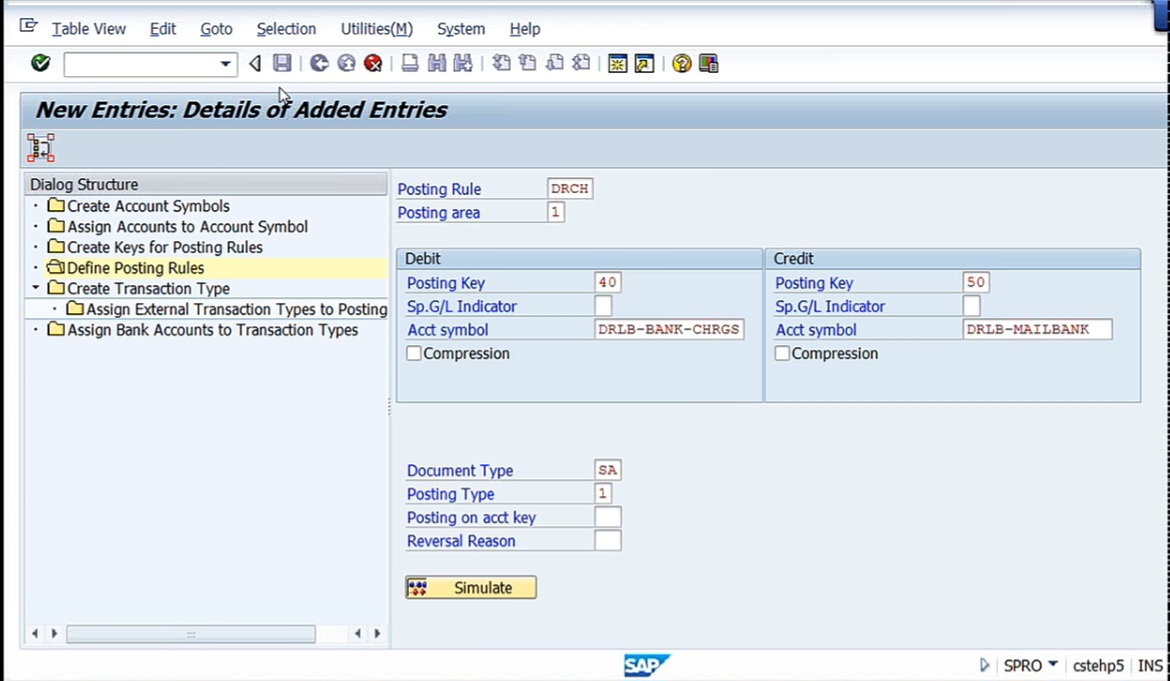

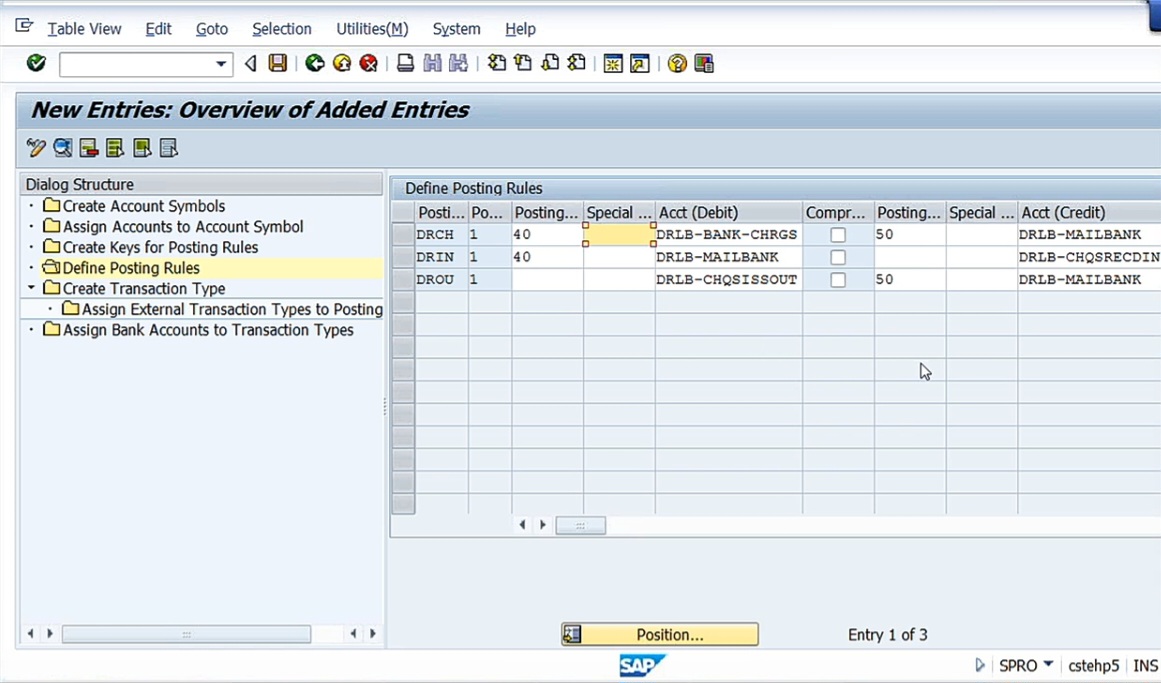

Next, go to Define Posting Rules. Click on New Entries. Here, first of all, what are the rules that we have defined?

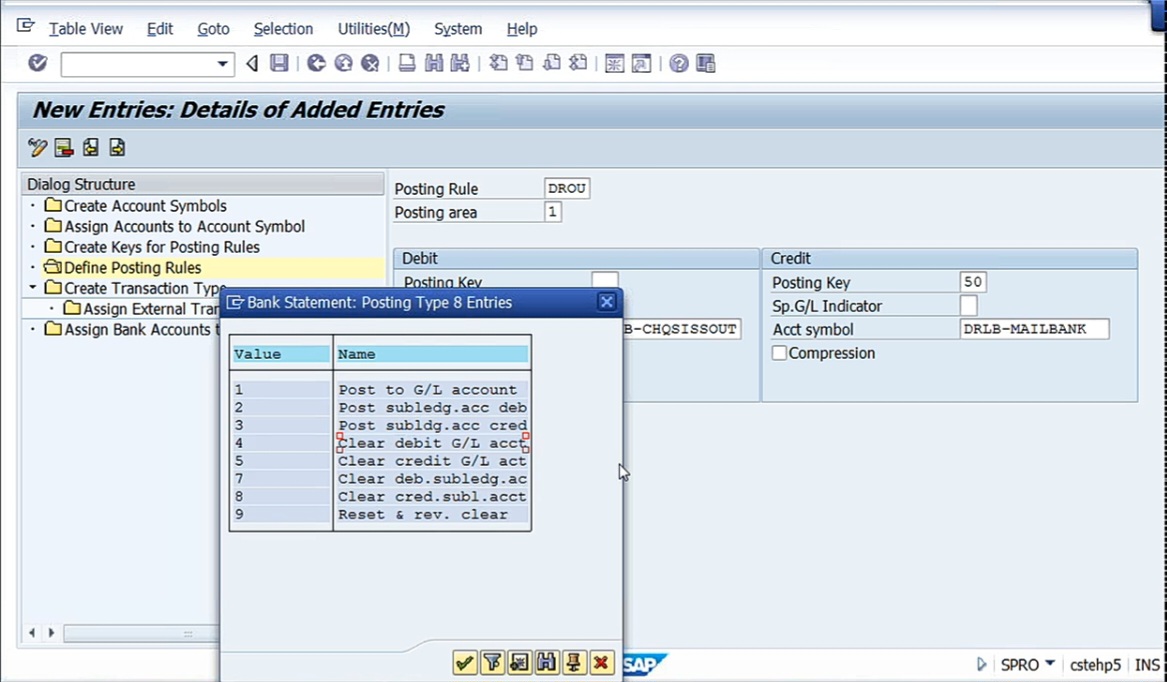

See, DRCH, DRIN, DROU. OU means cheques issued out. This is the symbol we have created, DROU. Posting area, select bank accounting. When cheques are issued out, when EBS is uploaded, what is the accounting entry we should get? That is cheques issued account should be debited, main bank account should be created. So here I have to tell to the system, main bank account should be credited here, so DRLB main bank. Main bank account should be credited, credit. Posting key should be 50. Cheques issued out account should be debited. DRLB cheques issued out. But whenever we are giving any subaccount, don’t give the posting key here. DRLB- main bank is the main bank account, this is the GL account. DRLB-CHQISSOUT is a sub ledger account. This is what I told you, cheques issue account, cheques deposit account, both are sub accounts. But main bank account is the main bank. Main bank account is the main GL account. And the rest of the things are sub accounts. When you are using a sub account, don’t give the posting key. But only when you are giving main bank account, give the posting key. Next document type, we are going to use SA document. And, posting type, I have to use posting rule 4- clear debit GL account.

Clear the debit GL account means what? Here, cheques issue AC DR, this is debiting. This GL account, it is going to be cleared. Means, when we issue the cheques, this is going to be cleared here now. So while debiting this, the account is going to be cleared. So that’s why we’re taking 4, number 4 is nothing but clear the debit GL account. Save it.

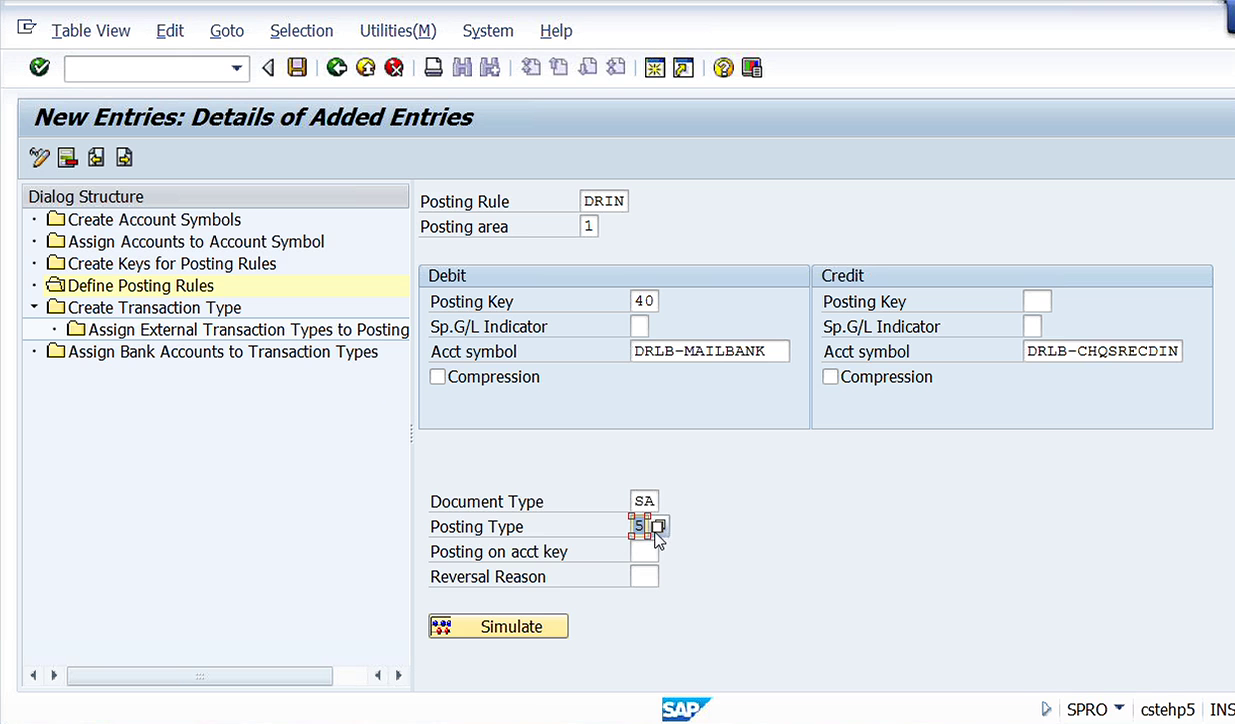

Next entry also I can do it. Click on the next entry symbol. Now DRIN, cheques received in. So even this also, bank accounting. When we receive the cheque, what is the accounting entry? So here, main bank account is going to be debited, and cheques deposit account is going to be credited. That is subaccount cheques deposit account is going to be credited. So that’s why here my main bank account should be debited. So debit 40, DRLB main bank account. Here (credit), cheques deposit account, DRLB cheques received in. So whenever you are using a subaccount, I told you don’t give the posting key. So document type here, SA. And posting type, we have to use 5 here, clear credit GL. This is nothing but this is here we are crediting it, so that’s why we take credit GL account.

The third entry, bank charges, DRCH. Whenever bank charges are going to be debited or credited, Bank account both are now GL accounts. See, what is the accounting entry when bank charges are debited? When bank charges are to be accounted for, then the accounting entry should be bank charges account return to main bank account. This is the accounting entry. Here both are GL accounts. But in this case, one is GL account, one is a subaccount. So that’s why here you have to take both the GL account, both posting keys. Bank charges account return to main bank account. So main bank account is going to be credited here, DRLB mainbank, and for debit, DRLB Bank charges account symbol you have to take. So posting key debit is 40, credit is 50. document Type, SA. Posting type should be post to GL account, 1, because both are GL accounts.

Save it. So these are the 3 line items we have created.

Let us stop here. We have to complete 4 more steps, there are so many other steps out there. In the next class, I think we can complete it. But I know that all these steps are a bit confusing, and of course you need to take it up several times. From the beginning, you’ll be in a state of confusion because why I’m doing all these things, everything you don’t understand. Once we execute it, when the system posts, then again I’ll get back to you how these rules are helping us in creating these GL accounts. Because these entities will be automatically posted. So these are the requirements, and then this is the configuration.