Foreign Currency Valuation 2

So this is a document which we have seen yesterday:

Thank you for reading this post, don't forget to subscribe!

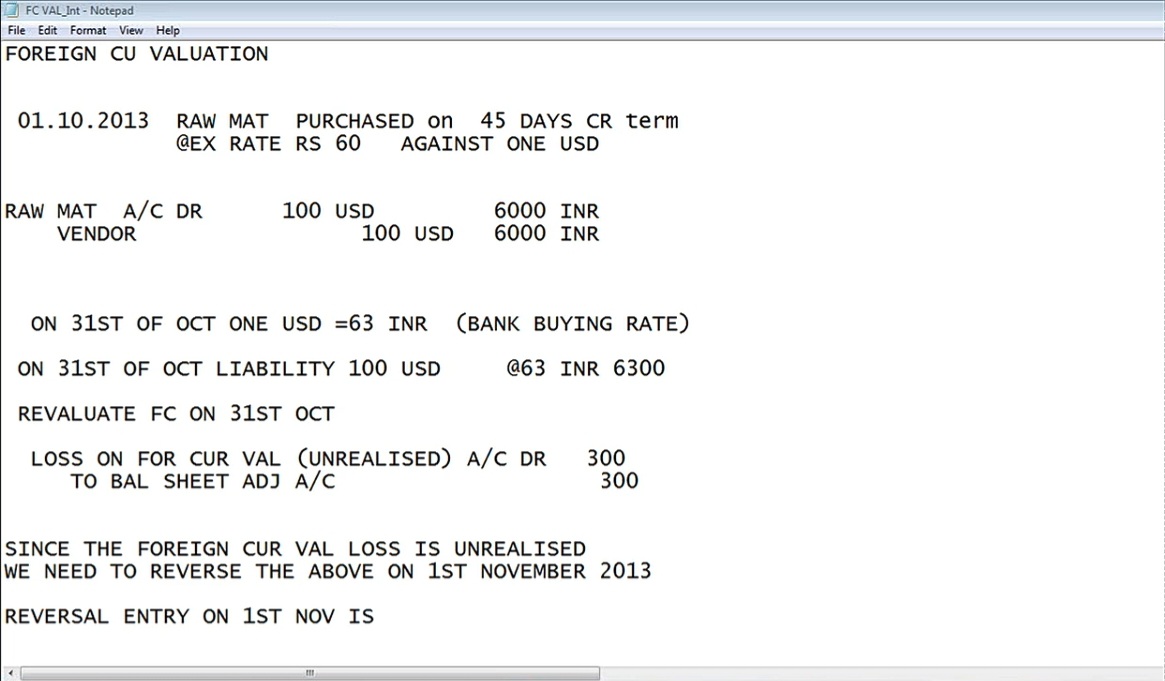

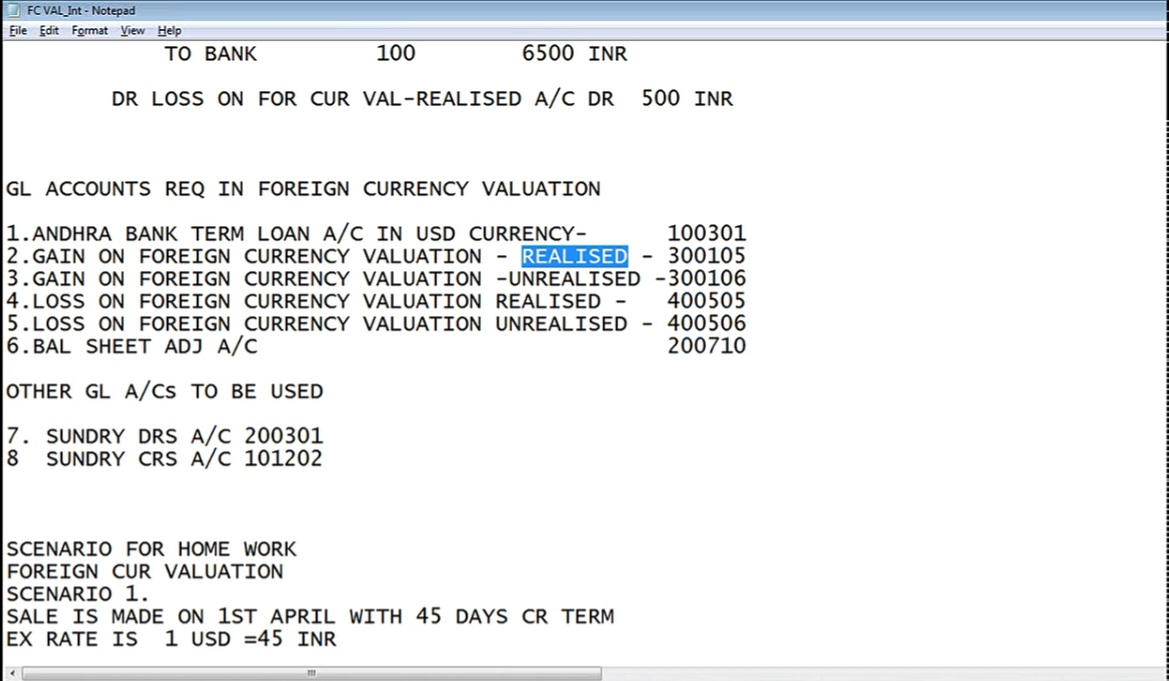

So on 01.10.2013, imagine that we have purchased raw material on 45 days credit term. So at the time, the exchange rate is going to be 60 rupees against 1 USD. So raw material account return to vendor account when you purchase material. So 100 USD, if you are paying 100 in US dollars, 100 USD, and the purchase price is going to be 6,000 rupees. That will be booked into the books of accounts. On 31st October, that is at every month end, every company will evaluate their assets and liabilities at the month end, and the company need to assess its liabilities and assets at the end of every month. Because every month end, whenever an ERP is implemented like SAP, every company would like to have their financial statements on the table of the head of the organization. Because when a software which can provide the financial statements every month, every company will prepare it. Now what is my liability as per the books of accounts? As per the books of accounts, it is going to be only 6,000 liability. But if you are going to take the future liability into consideration, that is today’s exchange rate is 63 rupees, that is on 31st October, 63 rupees. And I need to consider the increase in the foreign currency exchange rate. So that’s why what I need to do is, since this is going to be loss, in case if I’m going to pay today to the vendor, I’ll be incurring 300 rupees more, that should be posted to loss on foreign currency valuation. Loss on foreign currency valuation, since we have not yet paid, but in case if you pay, we call it as convention of conservatism. Nothing but even though we are not going to make the payment now. But in case if I’m going to make the payment, what is my liability? That is what I’m going to consider in my books and accounts. And, so that’s right, loss on foreign currency valuation unrealized account return to balance sheet adjustment account. So balance sheet adjustment account, since this is going to be reversed on 1st day of the next month, this will get nullified. So since the foreign currency valuation loss is unrealized, that is not realistic, this is only on book, that’s all. And if we need to reverse the above entry on 1st November 2013. Reverse entry, first number is balance sheet adjustment account return to loss on foreign currency valuation, same. But on 15th November, payment of 100 USD is due. We’re going to make the payment to vendor account return to bank. So vendor account with 100 is 100. But in order to buy this $100, I need to shell down 6,500 INR. So that’s why bank account is credited with 6,500. But, originally, vendor account is showing 6,000 that will get nullified. The extra 500 rupees is going to be posted to debit loss on foreign currency valuation realized. This is actual loss. That is realized loss. So this is the entry.

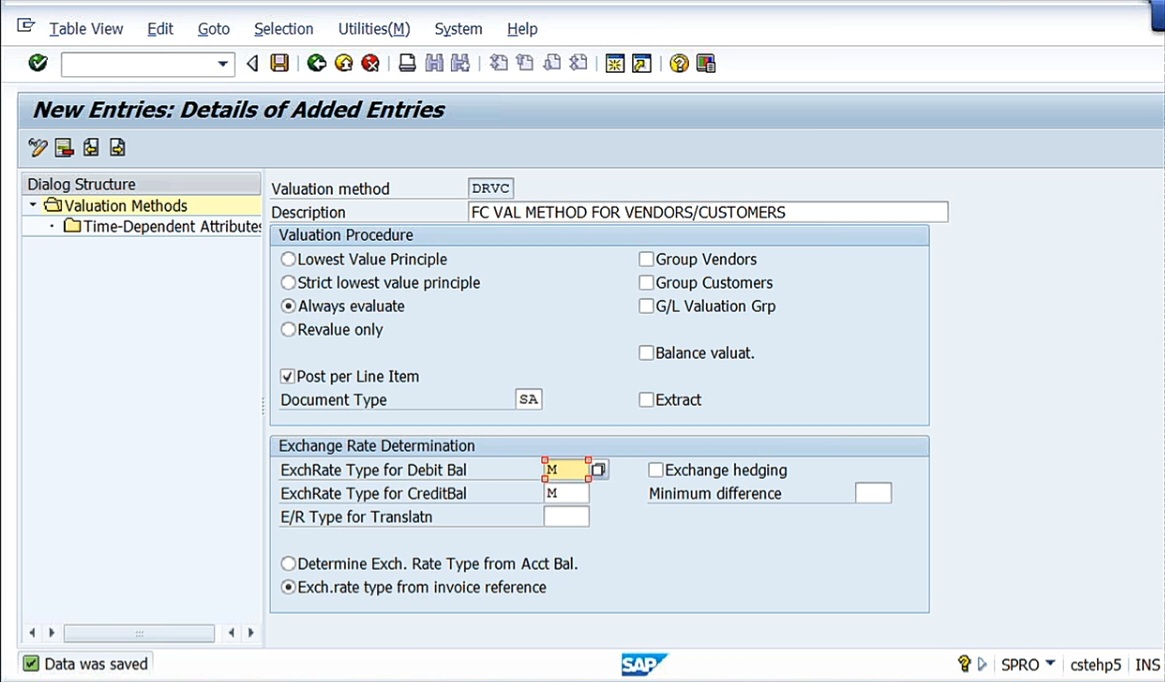

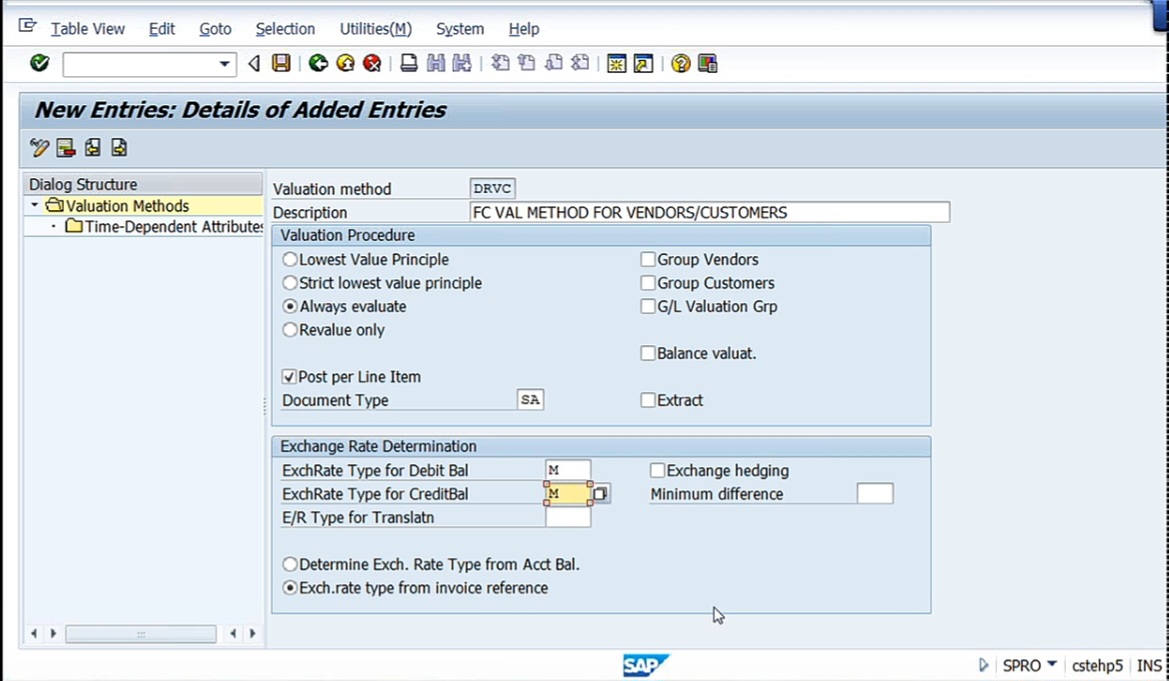

Now let us see how the system is going to post accounting entries and how we’re going to configure it, and gain or loss, gain on foreign currency valuation and gain on foreign currency valuation, realized and unrealized. Based on the exercise, whatever we are doing, now you need to do sales entry also, exactly the reverse. And loss on foreign currency, now since we are making payment, so loss on foreign currency valuation realized, unrealized. These are the 2 things which will work out for us. Let us do the configuration part. First is define valuation method. Got to Financial Accounting (New), General Ledger Accounting (New), Periodic Processing, Valuate, Define Valuation Methods. Here, we need to define one valuation method. There are 2 valuation methods we can define. One is for sundry debtors and sundry creditors. For both line item wise valuation, we have to do it. Say, for example, in this scenario what I told you, only one line item we have taken, that is one purchase of raw material. Similarly, I’ll be buying different types of raw material or assets or anything from any number of customers and belong to foreign customers other than our regular purchases. That is by paying foreign currency, and foreign currency may not only be USD, GBP, or any other currency, any number of currencies it may be. So all those things line item wise even in one vendor account, I may have several line items with the foreign currencies. So that’s why what we need to do is we need to define a foreign currency valuation method. Okay. Let us go to new entries. So this valuation method, what I need to do is, I’ll define foreign currency valuation for sundry debtors and sundry creditors. Because line item wise valuation I need to do. Our company code DRVC, that is Dr Reddy Labs Vendors and Customers. Here, certain methods are there: lowest value principle, strict lowest value principle, always evaluate, revalue only. Select always evaluate. Always evaluate means whether the foreign currency valuation is less or more, whatever it may be, we need to always value it. Lowest value principle means in case if the foreign currency is lower than the value at which we have purchased, that is lower than the current, then only it will evaluate lowest value. Strictly lowest value means if it is last time when we evaluate, it is already lowest value. Strictly lowest value means it is lower than the earlier lowest. So like that, some certain principles, certain methods are there, but just forget all those things. Select ‘always evaluate’. Always evaluate means whether there is increase or decrease in the foreign exchange, whatever it may be, irrespective of that, you evaluate our foreign currency valuation. That is what we are selecting. Check ‘Post per line item’ box. So I want the system to identify for every line item. Every line item wise, foreign currency is not say, for example, say this is line item vendor, this is $100. Another vendor, $200. Another vendor, $400. Like that different line items will be there. It is not the valuation of all dollars put together, only one. I mean total put together, say $1,000 valuation, it is not like that. Each and every line item, line item wise evaluation I need. So that’s why here, what we need today is post per line item. Then document type. So what is the document type that you are going to use for evaluation? Because after evaluation, system is going to pass accounting entry. See, this is accounting entry first time: raw material account return to vendor when we purchased it and, say 300 rupees loss on foreign currency. This is the entry posted by system automatically. For that, system is asking which document you are going to use. We use SA document. Here, you have all the documents types. Select SCA. And, group vendors not required. Group vendors and group customers. If you are going to create a group, again we have to do some other configuration. GL valuation, balance valuation not required. Exchange rate type for debit balance or credit balance, let us take M, that is average value. Now here, we have determine exchange rate type from account balance, Determine the exchange rate type from invoice reference. Means, we are telling to the system because vendors and customers are there, for this purpose, we are asking the system exchange rate determination is exchange rate type from invoice reference. The type of exchange rate is going to be taken from the invoice reference because whatever the foreign currency we are evaluating, you take the foreign exchange rate that has been defined for that line item. So, check ‘exchange rate type from invoice reference’.

These are the parameters we need to define. Save it.

I’m creating another request. FC Valuation DRLB.

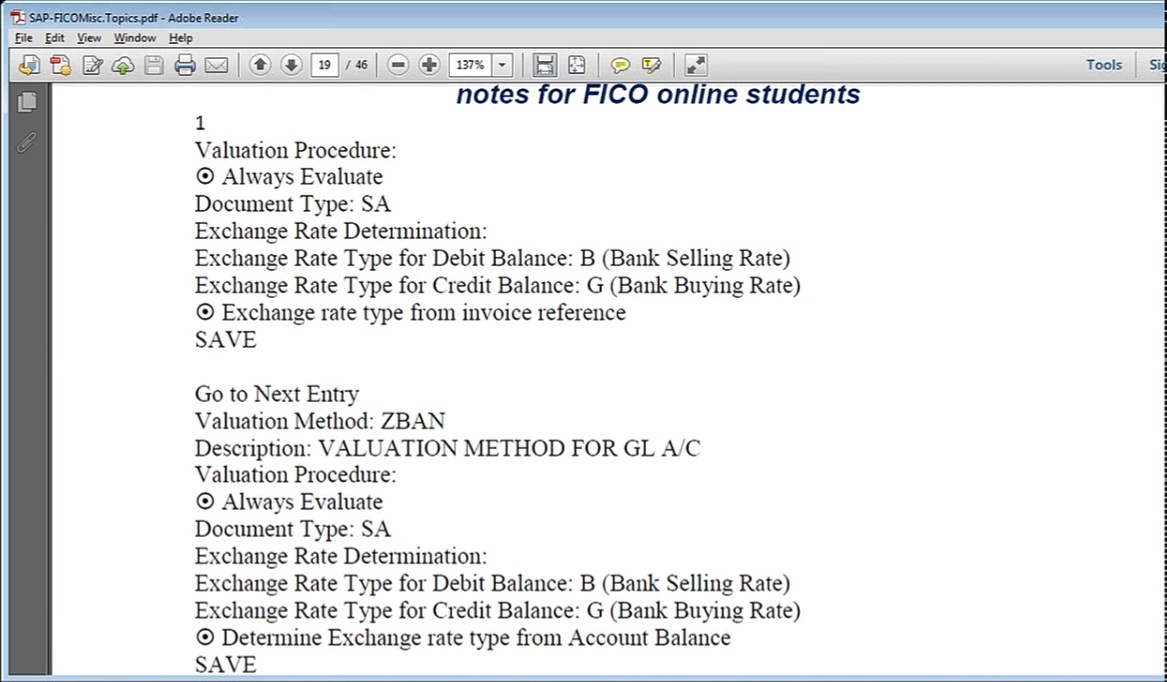

Here, certain different methods also we can use. Bank buying rate, bank selling rate, exchange rate type for debit balance. In the note, let us check here.

Here, always evaluate. It’s saying rate type for invoice reference. See here, it’s saying rate type for debit balance and rate type for credit balance. We can use B or G, B means bank selling rate, G means bank buying rate. Exchange rate type for debit balance: bank selling rate. So in our entry, exchange rate type for debit balance, I can take instead of average. This M is average. I think we have used this one. See, if you observe here, M- standard translation at average rate.

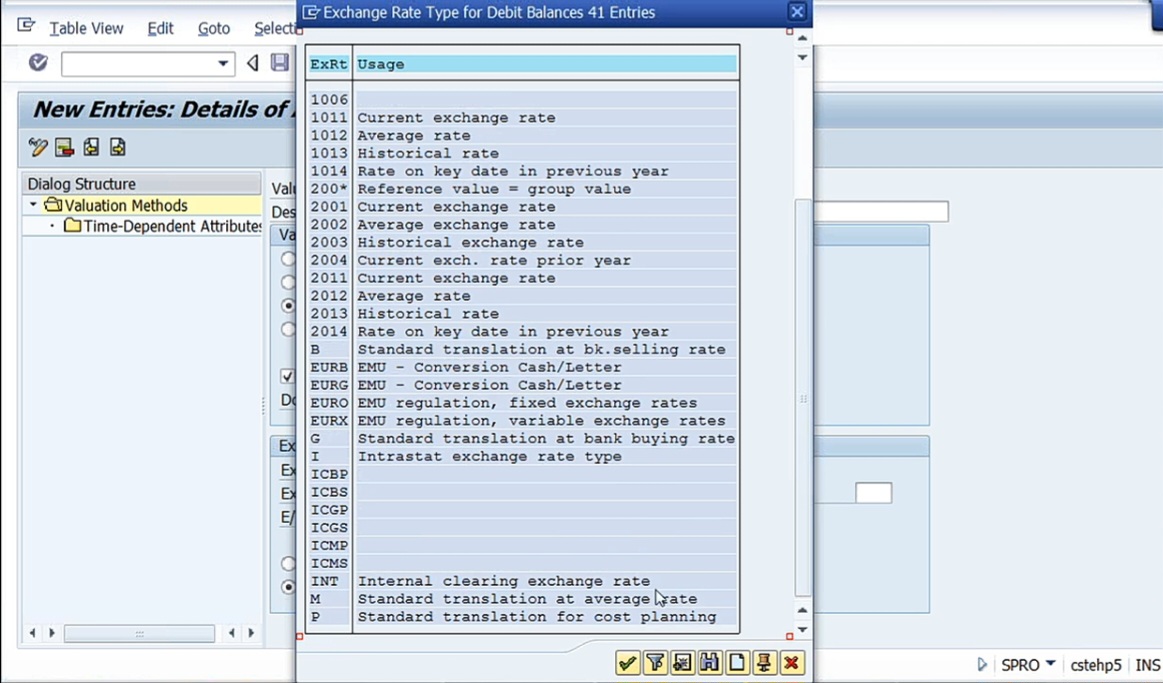

So because in a month, there will be so many transactions, I’m going to take the average rate because of our convenience generally, we do take average rate. If you remember in the beginning when we have posted accounting entries with foreign currency, we have taken M only, that is M is average rate. Here, exchange rate type for debit balance, you can take B, that is bank selling rate. If it is debit balance, that’s bank selling rate, means say for example, debit balance means the amount which we are supposed to receive from the customer. The debit balance is because if you take up customer’s account, customer account will be always shown the debit balance only because the amount to be received from the customer, that is outstanding amount. And exchange rate for credit balance means that is for vendor account. So in case if there is a debit balance, you can take bank selling rate. So selling rate means, say the amount which we are going to receive from the customer, that can be evaluated at bank selling rate. Because once we receive US dollars from customer, we are going to sell it. So at what rate I have to sell, here I’m taking average rate. Rather, you can take here bank selling rate. Or if it is a exchange rate type for credit balance, then you take bank buying rate. Because whatever the rate the bank is going to sell, at that rate, we have to buy it and we have to pay to the vendor. Here, I have given B and G. In case if you are getting any confusion with this, just don’t worry. You take only M, that’s why I’m taking M here.

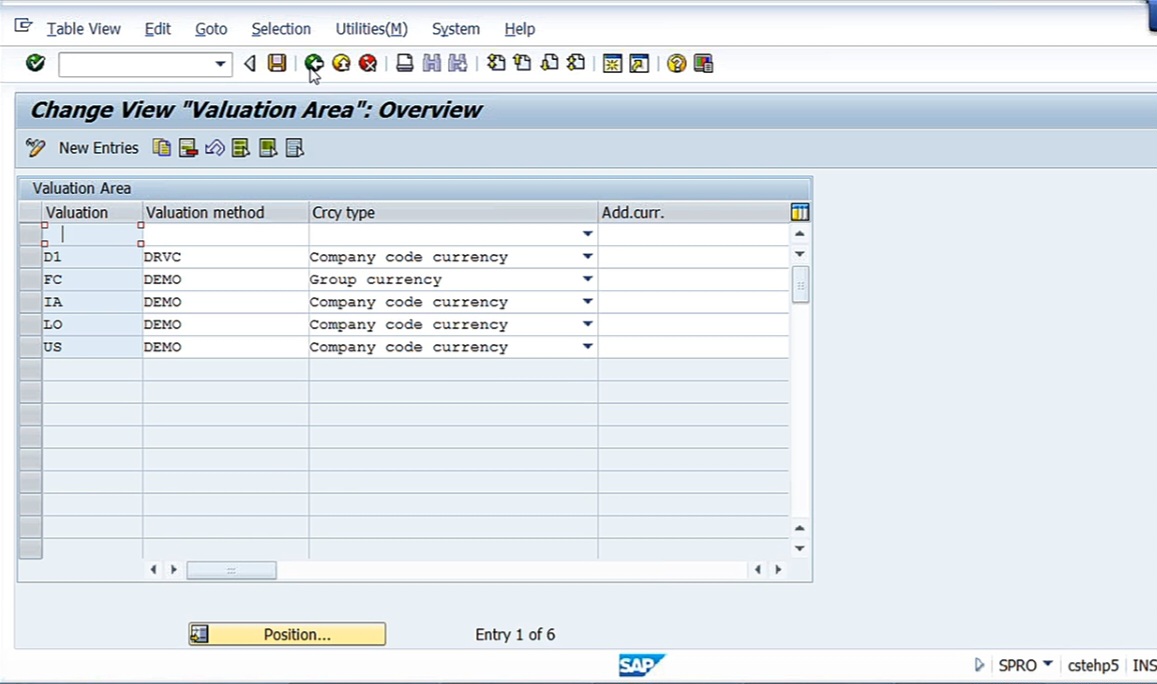

Save it. And here, ‘exchange rate type for invoice reference’, ‘determine exchange rate type for account balance’. When is ‘determine exchange rate type for account balance’ going to be considered? This is going to be considered in case if you are valuating, say for example we have taken loan from a bank. Say, for example, a loan in US dollar. Now after 1 month, I’m going to valuate my loan. So 1 lakh dollars I have taken on 1st October. On 31st, I’m valuating. So on 1st October, what is the value, that is exchange rate. On 31st October, what is the exchange rate? Now the differential exchange rate multiplied by 1 lakh will give you the loss or gain of that, what you call, type of that account balance means the bank loan. So on bank loan, whatever the exchange rate difference from the beginning of the month to end. And the differential amount is going to be loss or gain on account of foreign exchange loan that has been taken from the bank. Every month, I need to valuate that also. So here now, we are not concerned with that. Presently, we want to value customers and vendors. For customers or vendors, both same. Here, if you select ‘exchange rate type from invoice reference’, that’s why I’m defining only one rule for customers or vendor. Come back. Next, define valuation areas. Valuation area, I’m going to define, a 2 digit valuation area I need to define. So what is that 2 digit valuation? What I will do is go to New Entries, our company code is DRL. I am taking, say, for example, D1. Valuation method, whatever we have defined, DRVC is the valuation method, and the currency type is nothing but company code currency, because the valuation we are asking the system to validate for the company code currency. That is if USD is taken or GBP is taken, whatever it may be, the valuation by default should be converted into the company code currency, whatever the currency it may be. So that is what we have defined here.

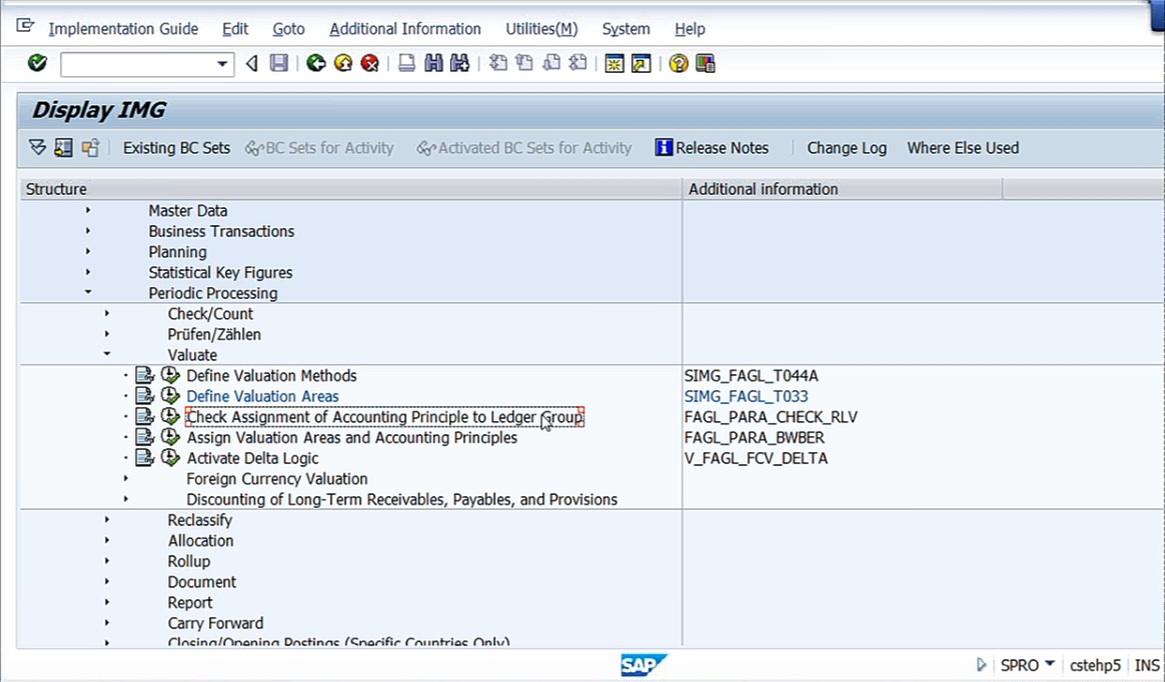

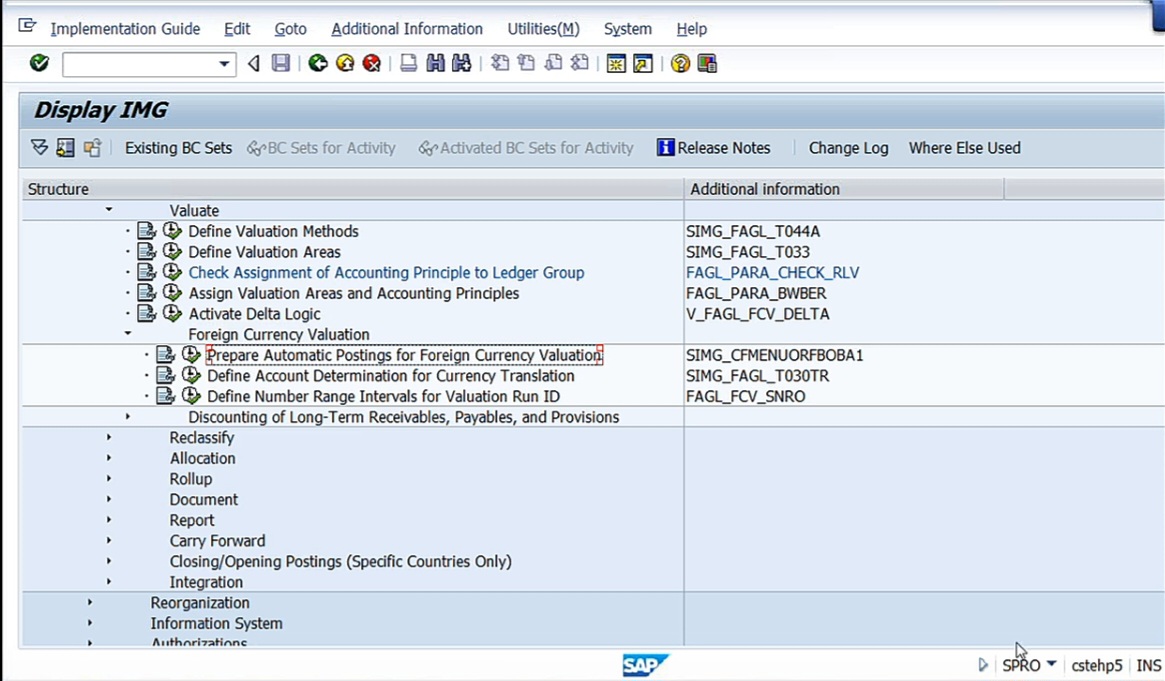

Save it. Then what is the importance of valuation area? This will you’ll understand later, not now. We have just defined a valuation method and that is linked to one valuation area. This is valuation area, D1. Come back. Go to ‘Check Assignment of Accounting Principle to Ledger Group’. Before we do these two steps, Assign Valuation Areas and Accounting Principles has to be done. And here, I’ll tell you one thing. In Financial Accounting Global Settings (New), Ledgers, Define ledger for the general ledger accounting. One thing I need to tell you here. That is nothing but here, there is a general Ledger that is a standard ledger provided by the SAP system.

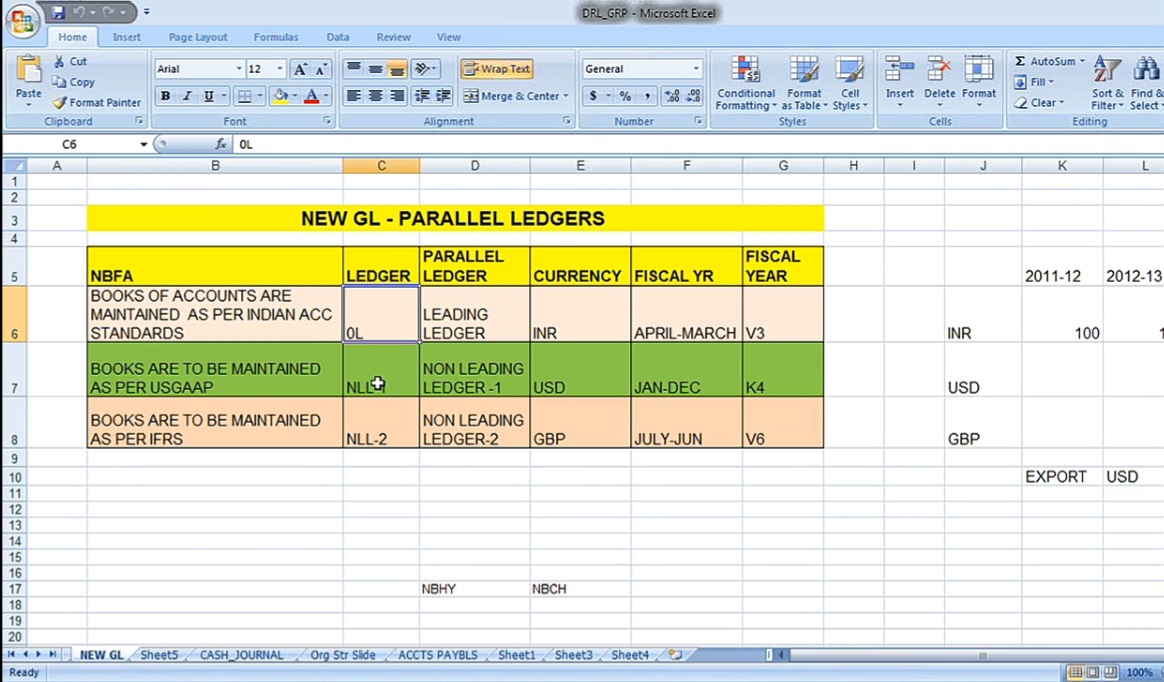

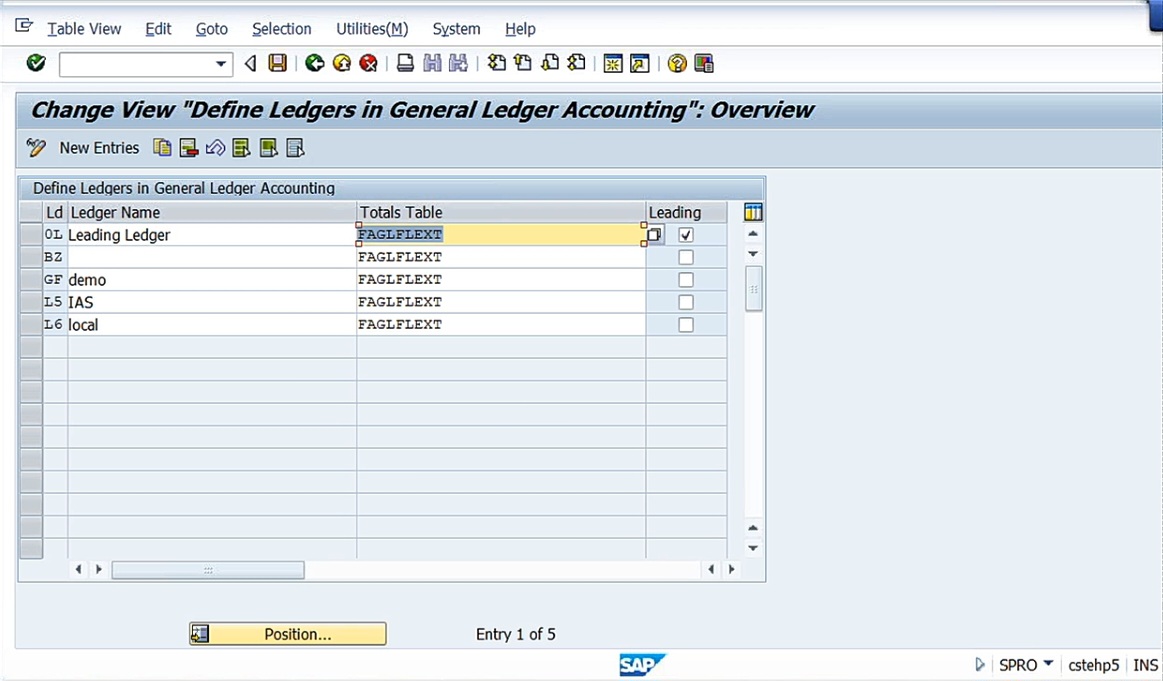

See here 0L ledger. That we call it as leading ledger. 0L is a leading ledger. By default, whenever you define a company code, a leading ledger will get defined for that company code. Now whatever the company code that we have defined, for that by default, your leading ledger is going to be defined. That is 0L ledger that is called. That we don’t know, we don’t observe. But because time has come, this I’m explaining to you, 0L is a leading ledger. What is leading ledger? Then is there any non-leading ledgers? Means yes. This is leading ledger, and we are going to have non-leading ledgers also. That I’ll explain to you when we go to the New GL concept.

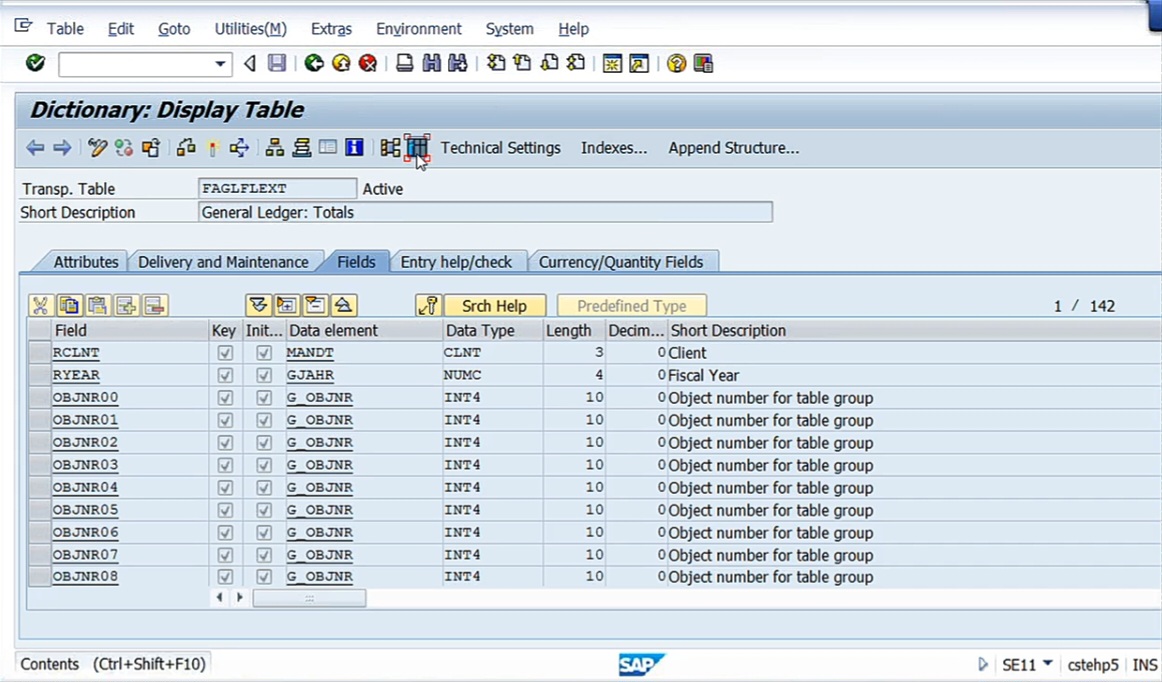

See here, 0L is leading ledger, and, NLL-1, NLL-2, we can define as non-leading ledgers. So what is non-leading ledgers? What is leading ledger? We’ll discuss later. But now for the time being, let us understand the standard ledger that is going to be linked to every company code is leading ledger, 0L. So that leading ledger and all your sundry debtors, sundry creditors, ledger, subledgers, everything is linked to this. Why I’m explaining this to you, see, this shows the table in which the data is going to be stored is FAGLFLEXT.

What is this? This is table. Table means in SAP the total data is going to be defined in tables. In fact, that is the technical requirement. ABAPers know what is meant by table. There’s a T code called SE11. Type SE11 in the command box abd press Enter.

Any table you can see here. Copy FAGLFLEXT and paste here. That is database table. That is this we call it as totals table. Click on display. Means the new GL data is going to be stored in the table. So not only that accounting data, everything is going to be BSEG, BKPF.

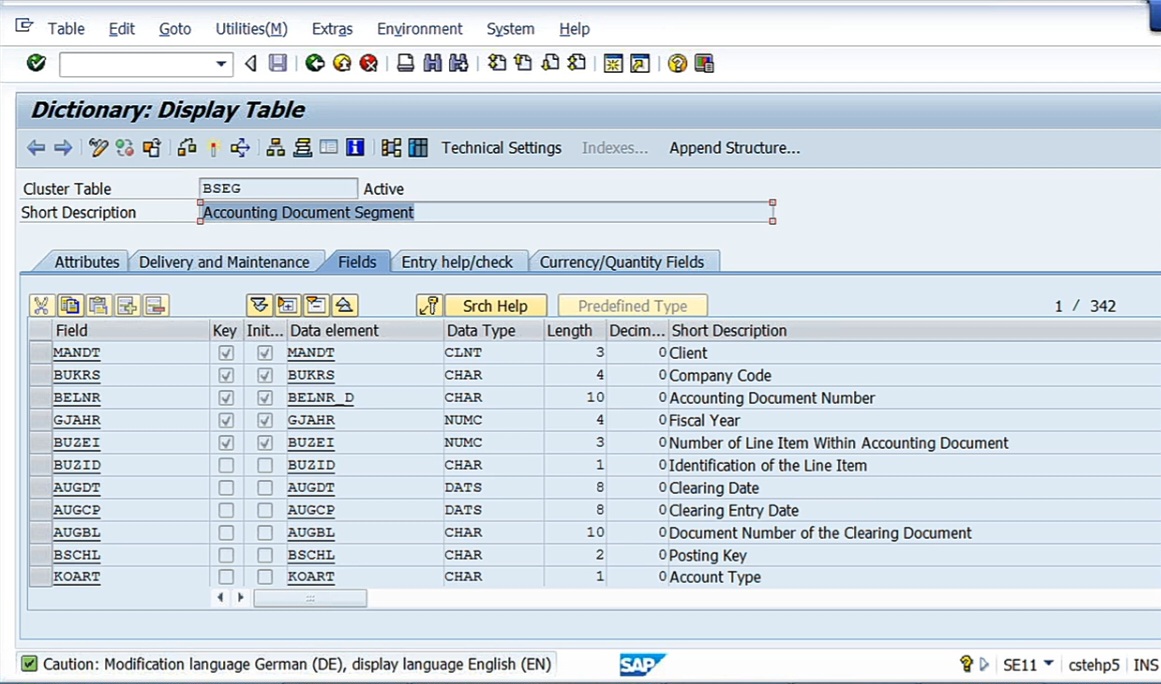

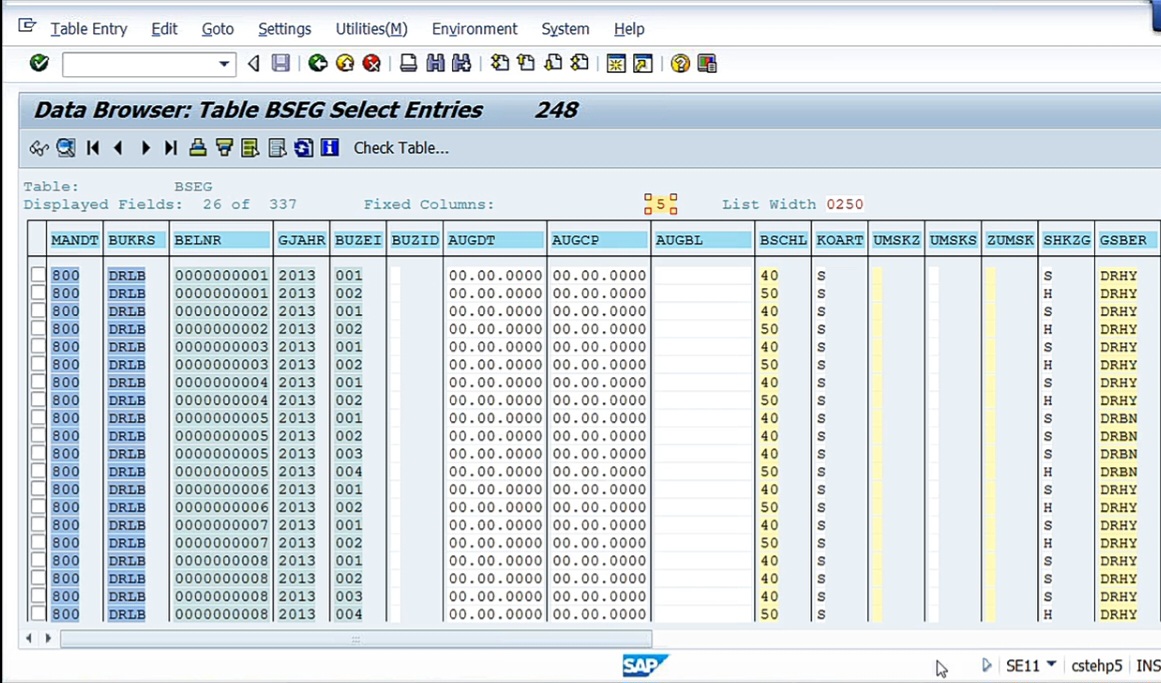

See ledger totals, all ledgers. Here, if you click on the button before ‘Technical Settings’, the total data is visible. And similarly, if you want to display BSEG table. BSEG is nothing but a table name in which data is going to be stored. What data? Accounting data. Accounting data is going to be stored in SAP tables. And because see where the data is going to be stored for every software, there will be some way of storing the data. See accounting document segment, BSEG.

And if you click on this, you’ll get BUKRS. This is the technical name for the company code. Right here, say for example, DRLB.

Execute. Our data, total data is stored like this.

Technically, the data is going to be stored. Every data is going to be stored here. There is the line item 1, line item 2, year, etc. Whenever you post an accounting entry, system creates with all this table with all these fields. Whether you enter it or not, system will create it. That’s why lot of space is going to be wasted here. In case of ERP, it takes lot of table. Because for every line item, I don’t know what line items I’m going to use, what information I’m going to store. That’s why for each and every line item, total structure is going to be created here. And wherever the amount is required, that amount will be posted. That’s all. Like this, the total information is going to be stored in this kind of tables. Now come back. So this FAGLFLEXT is also a table in which the GL general ledger accounting information is going to be stored.

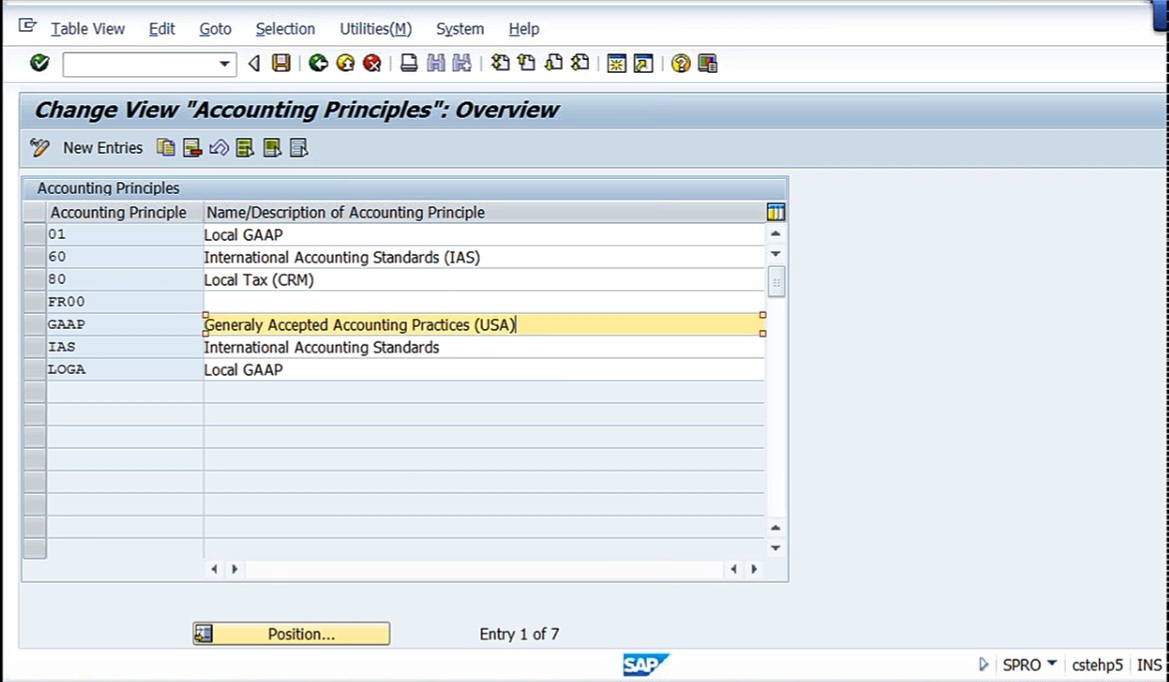

Here, I need to tell you one more thing. Go to ‘Define Accounting Principles’. If you are configuring your SAP system for US accounting, you have to define your US accounting principles like US GAAP. If it is going to be UK, then you are going to define accounting principles as per IFRS, that is International Financial Reporting Standards, now which is going to be mandatory for all countries. There are uniform accounting standards that have been defined by the IFRS board. Accounting standard means what? Every country will have their respective accounting standards, that is nothing but as per the country’s requirement, the system of accounting is going to be defined. Whether how to evaluate your foreign currency, what are the principles, how to evaluate your inventory, what is cost or market value, whichever is less. That is Indian way. U.S GAAP, some other principle. IFRS, some other principles. JAS, Japanese accounting standards. Chinese accounting standards. Like that, different countries will have different accounting standards. Now, globally, all these accounting boards have come together, and they have announced IFRS, that is International Financial Reporting Standards. Till now, I think 9 or 10 accounting standards have been issued, and the rest of the standards are under processing. Now every country must and should follow this international financial reporting standards apart from your local accounting standard. So even in India, we follow Indian accounting standards as well as international financial reporting standard. And even U.S also is going to follow only IFRS from 2014 onwards, until then they are following US GAAP. GAAP means Generally Accepted Accounting Practices. Now why I’m telling you this, define accounting principle. So for your country’s accounting principle, we need to define, then that need to be linked to the respective ledger. Right here, I need to define my accounting principle.

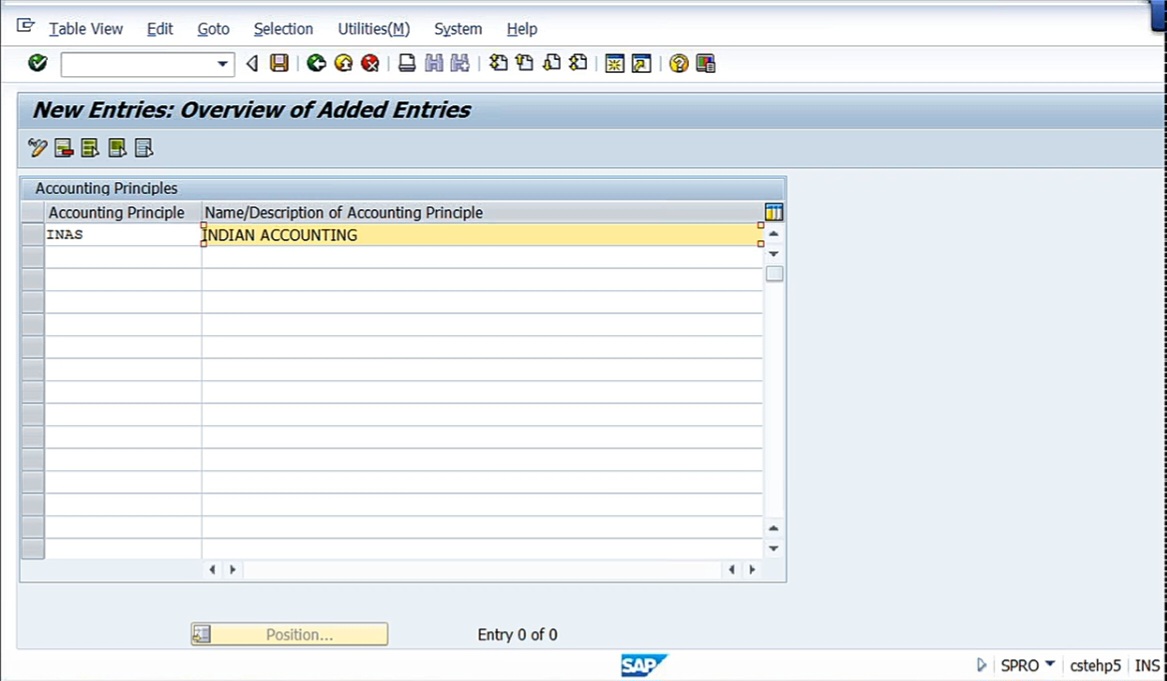

Right here, you see GAAP, generally accepted accounting practices, USA. IAS, international accounting standards. LOGA means local GAAP. So what I will do, I’ll define my own Indian accounting standards. Go to New Entries.

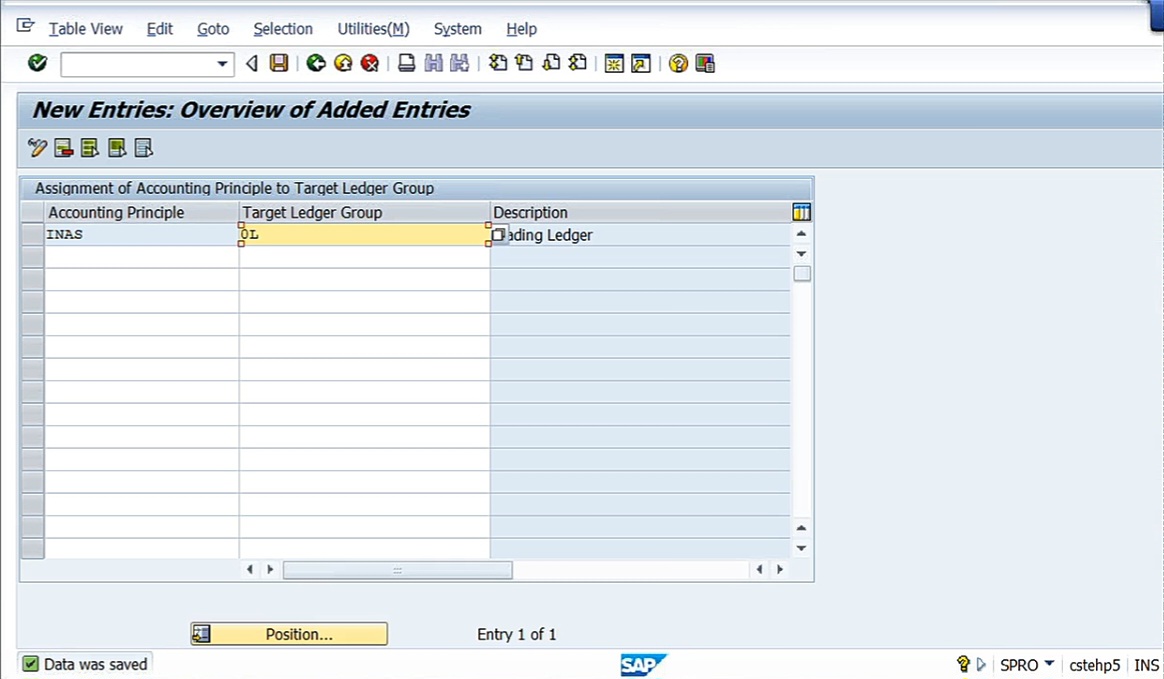

First, I’m defining this. Once we define this one, go to ‘Assign Accounting Principle to Ledger Groups. Assign accounting principle to ledger group means here, Ledger group I told you 0L is a standard ledger leading ledger. What I will do here, go to new entries. My accounting principle is, right, INAS. Target ledger group 0L, because 0L is a standard ledger for my company code.

So here, what I’m telling to the system, I’m going to follow Indian accounting standards to the 0L. I told you that by default 0L has been linked to my company code Doctor Reddy Labs. Now I’m going to define one Indian accounting standards principle. How this is going to be linked to our foreign currency evaluation I’ll tell you now.

Here, in ‘Check Accounting Principle to Ledger Group’.

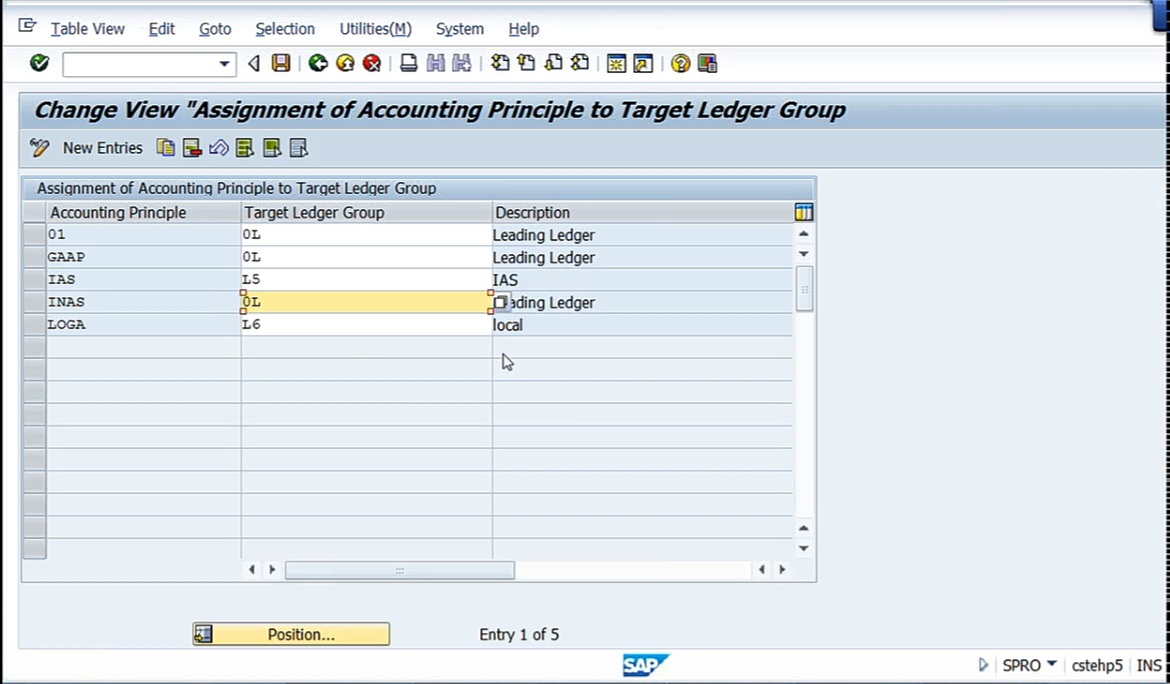

See INAS has been linked to ledger group 0L. I’ll show one more thing here. This is 0L is leading ledger, I can create non-leading ledger, ledger 1, ledger 2. And in case if my company code has to report my financial statements in 2 or 3 different accounting standards, it may be required. Say for example, in case if I’m going to raise my finance through U.S stock market. Say, for example, Doctor Reddy Labs literally, they have raised their funds from U.S market and also European market. And, that’s the reason what Doctor Reddy Labs has to do, they have to submit their financial statements not only in India, they have to submit their financial statements to SEBI, that is in India, and, in U.S, U.S SEC, that is United States, Securities Exchange Commission. But how they have to submit? Again, they have to prepare their financial statements in U.S dollars as per the calendar year, they have to prepare it. So here we have that we are going to discuss in New GL, that is leading ledger, non-leading ledger, etc. Then depending upon my country’s supporting requirements, I can have any number of ledgers. Each ledger can be prepared as per the different accounting principles. But now I’m going to assign my Indian accounting standards, it’s going to be linked to the main leading ledger. Leading ledger is prepared as per the Indian accounting standards, that has already been defined there, and here also appears the same. Now go to ‘Assign Valuation Areas and Accounting Principles’. Now this valuation area, whatever we have defined, that is D1 we have defined. Here, go to new entries. What is my valuation area? We have defined D1. D1 is already linked to my valuation methods, DRVC. So whatever the principles that we have defined in DRVC are linked to valuation area D1. Now D1 is linked to my accounting principle. My accounting principle just now I have defined Indian accounting standards.

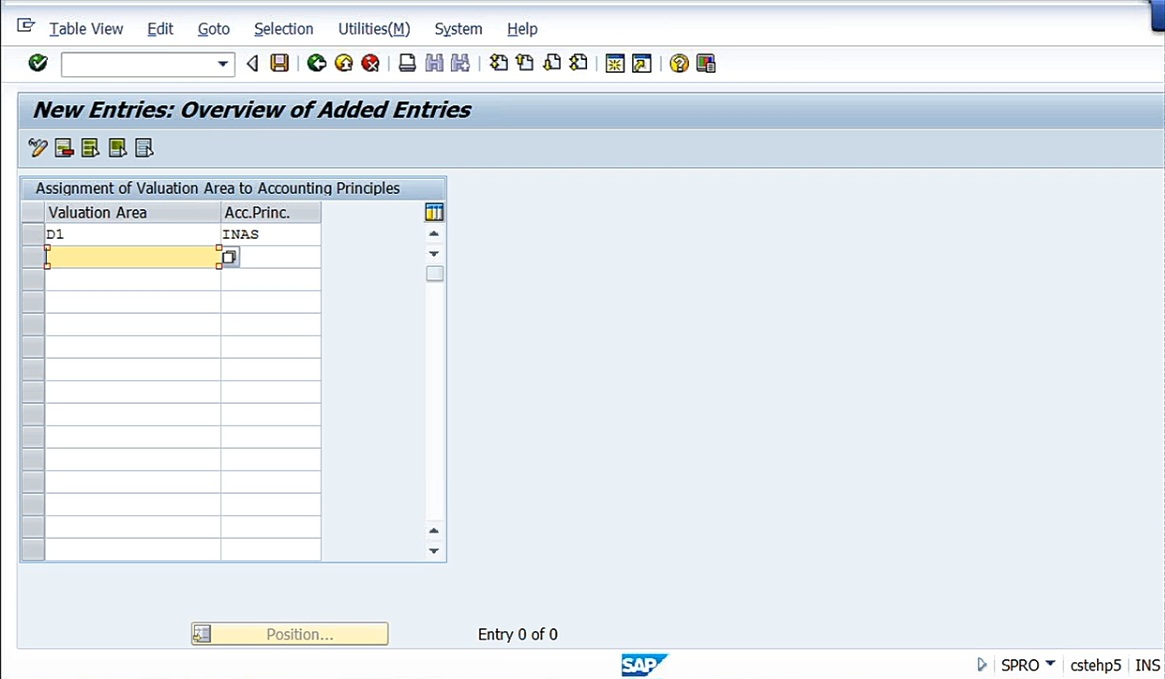

So my valuation, stock valuation, I can define something method that will be linked to INAS. Like that any requirement as per the country’s requirement, Indian accounting standards, I can define that and link it to that country’s respect to accounting principles. Now INAS has already been linked to your, leading ledger 0L. In turn, the foreign currency valuation, whatever we have defined, that has been linked to DRVC. DRVC is linked to D1. Now D1 is linked to Indian accounting principles, INAS, and INAS has already been linked to 0L. Now whatever the financial statement that you are going to prepare as per the 0L that is a leading ledger, that will be prepared as per Indian accounting standards. So every principle we need to create and that should be linked to the accounting standard whatever you are going to define. So in that way, your valuation principles are linked to the accounting standards and the accounting standards are linked to the concerned leading ledger. Of course, I know that it is difficult to understand at the first instance, but you need to define and you need to look into it once again, so then you can understand. So here, we have defined valuation method, valuation method is linked to the valuation area, valuation area is linked to the accounting principle, and that has been linked to the valuation area and accounting principle are linked to each other here. So one part is over.

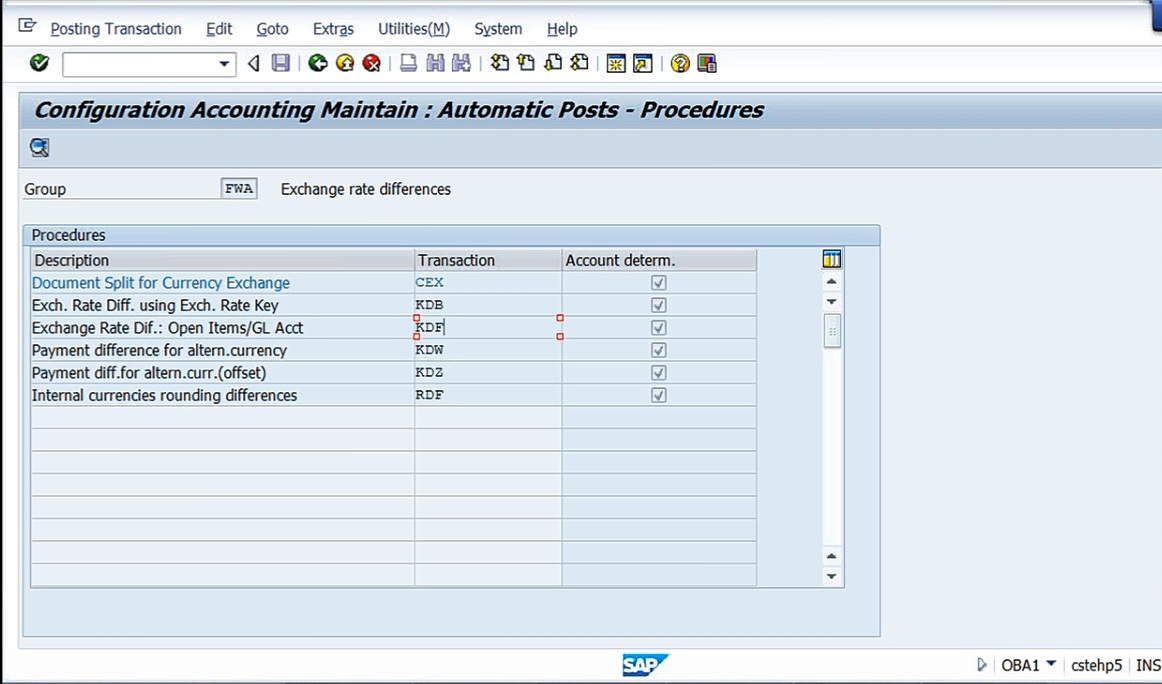

Now coming to the Foreign Currency, Prepare Automatic Posting for the Foreign Currency Valuation.

So here I told you that accounting entries are required on every month end. Every month end, my liability, whatever it may be, that has to be booked and reversed. I’ll be posting few hundreds and thousands of line items. All those things valuation manually just impossible for me. So that’s why all accounting entries I cannot manually post. I want automatic posting of entries. So for that purpose, I need to make automatic postings for foreign currency valuation. So here, in OBA1 I need to make the settings. Exchange rate difference: open items/ GL account.

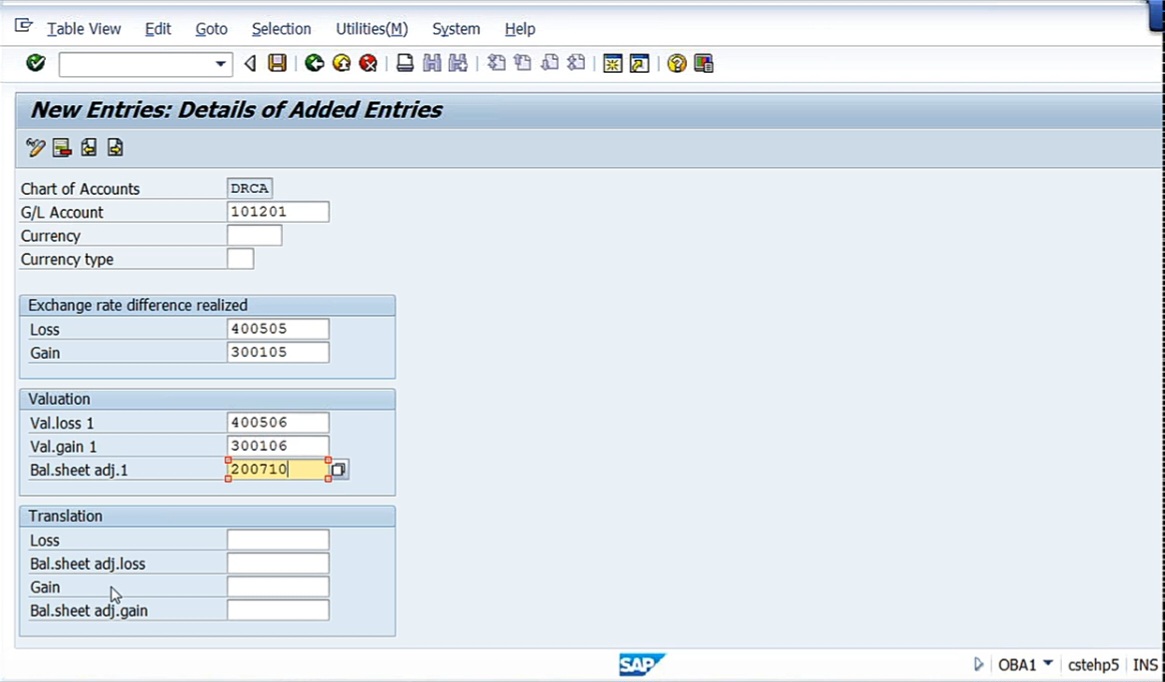

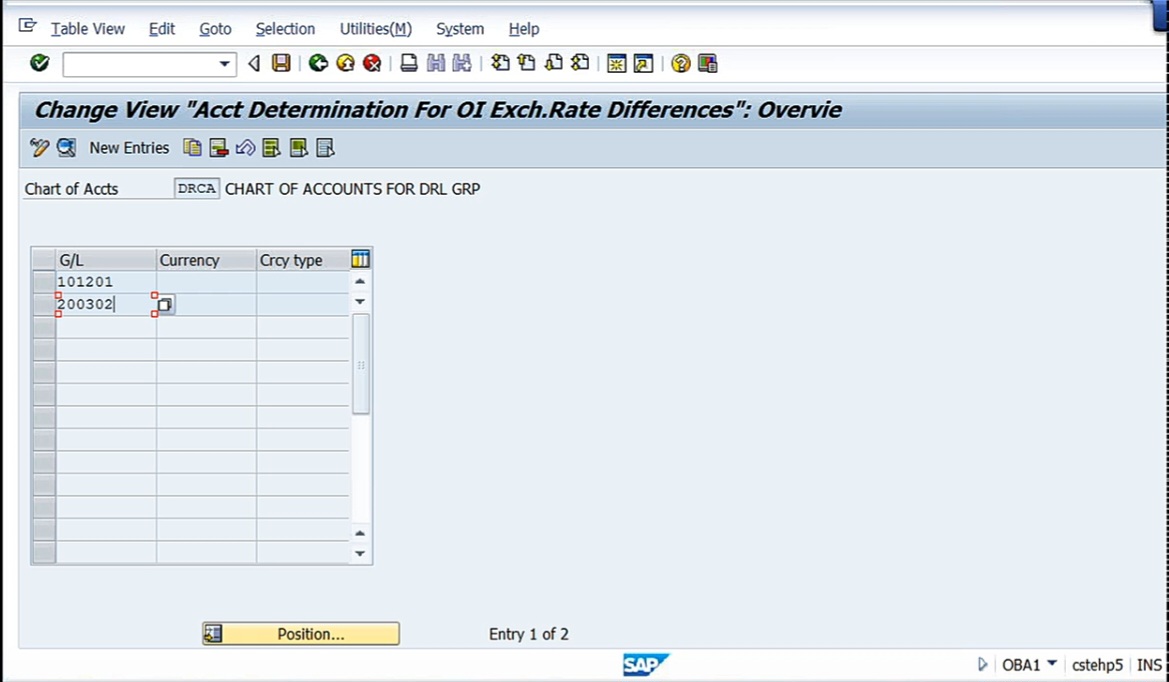

Here, double click on KDF. KDF is nothing but transaction key or accounting key. Whenever there is a transaction key I told you, it should be linked to a GL account. Now double click on this line item KDF. It’ll ask you which chart of accounts you are following, DRCA. And go to New Entries. Now here, two things. Number 1, we are going to valuate, say, company code DRLB, and the GL account is going to be raw materials. So anyway raw material vendors are there for us. So here is what I will do, I’m taking here GL account material vendors, 101201. Currency, currency type, you need not take now. Now exchange rate difference realized, already we have created GL account for exchange rate loss or gain, realized, unrealized accounts we have created. So here, loss and gain realized. System is asking me, okay to which account you want me to post if it is going to be realized? Realized means at what stage we post realized entry, realized entry is going to be posted when since the foreign currency valuation loss is unrealized, we reverse it, that is over. Now, say, on 15th November, payment of 100 USD is due. When we make actual payment to the vendor, the loss or gain is going to be realized at this stage. So here, loss. Similarly, in case of, say, customer sales etc, it is going to be gain. Even in case of vendor payment also, you’ll have a gain if foreign exchange, that is exchange rate reduces. Say for example, here, exchange rate at the beginning, say, 60 rupees. Subsequently, it got reduced, say, to 55. In such case, you get gain. So at that time, I want the system to post the gain. So loss or gain realized should be posted too. We have already created the GL accounts here.

So realized but loss or gain. Say realized gain on foreign currency, 300105 we have created. Loss on frequency valuation realized 400505. Both I’m taking. Here, I’m using some symmetry 505,105, like that. Similarly under valuation, loss or gain, unrealized. Unrealized gain 300106, Unrealized loss 400506. So we have already created balance sheet adjustment account 200710.

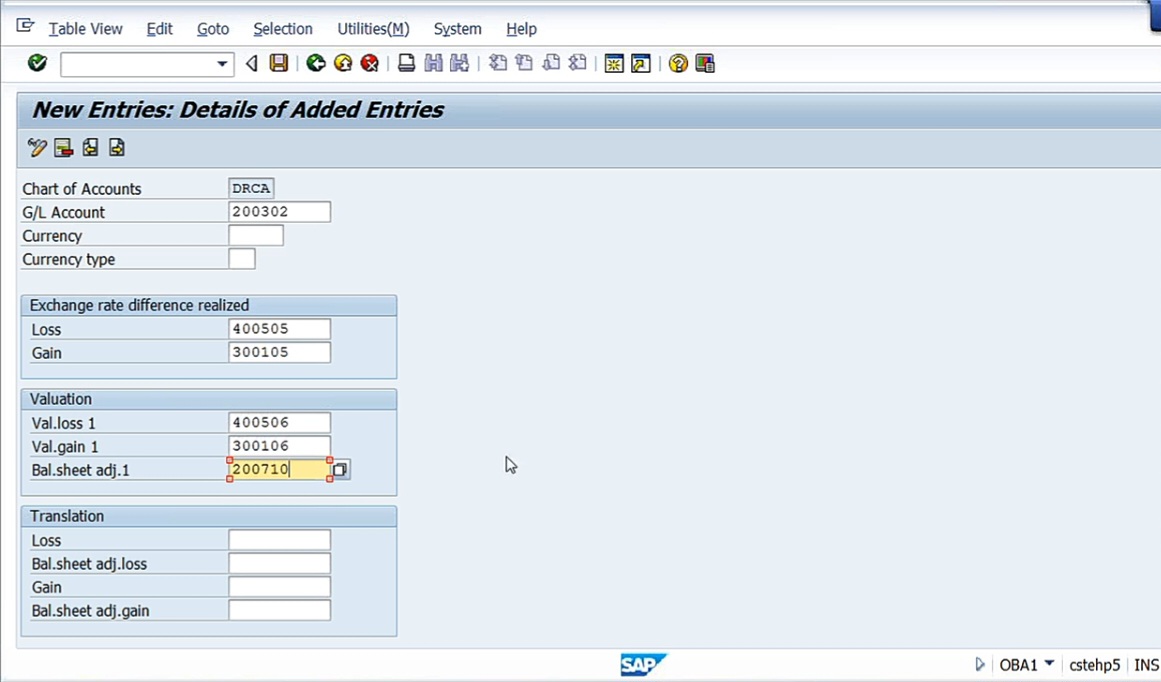

Leave below, don’t touch anything. This is sufficient for us. Save it. Now this is for the purpose of vendor payment. Vendor payment in case of when you are dealing with vendor payments, any loss or gain on account of foreign exchange will be posted to these accounts. Now what about customers? Go to new entries again. Now, sundry debtors. In case if you are going to make sales and there is a foreign currency, so now exactly the same scenario whatever we have discussed here. Right here, we are taking vendor. Instead, if you take customer on 01.10 we made the sale and exchange rate is going to be increased, then in such case you are going to get gain on the sales. So that’s why in case if you are going to bring out the foreign currency valuation on customer sales, you have to assign these accounts. Say, my sundry debtors account is 200301, sundry debtors. Sundry debtors domestic customers or sundry debtors foreign customers, whatever it may be you can take. And same exchange rate realization, same GL account you can take here.

Save it. So here, the configuration has been done with.

So these 2 GL accounts are for sundry debtors and sundry creditors. We have defined the valuation rules and automatic account assignment has been done here. So, this is done with. This is sufficient for the time being.

So the configuration part is over. Now what next we need to do is we have to post the accounting entry for the purchase of raw materials.

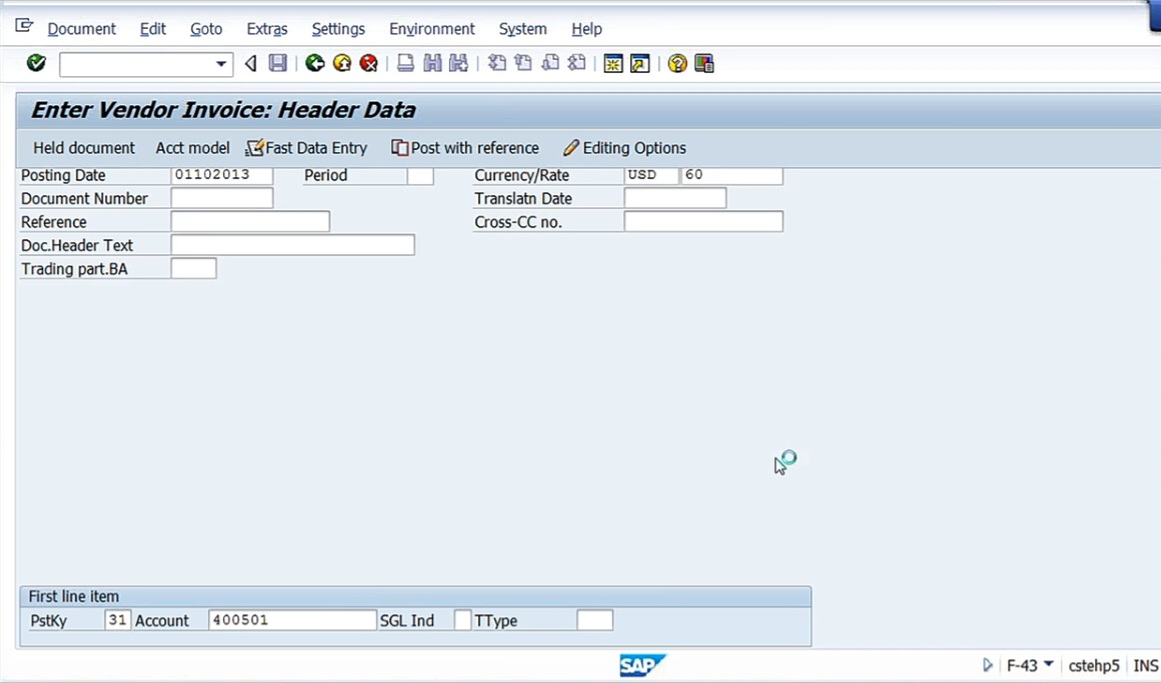

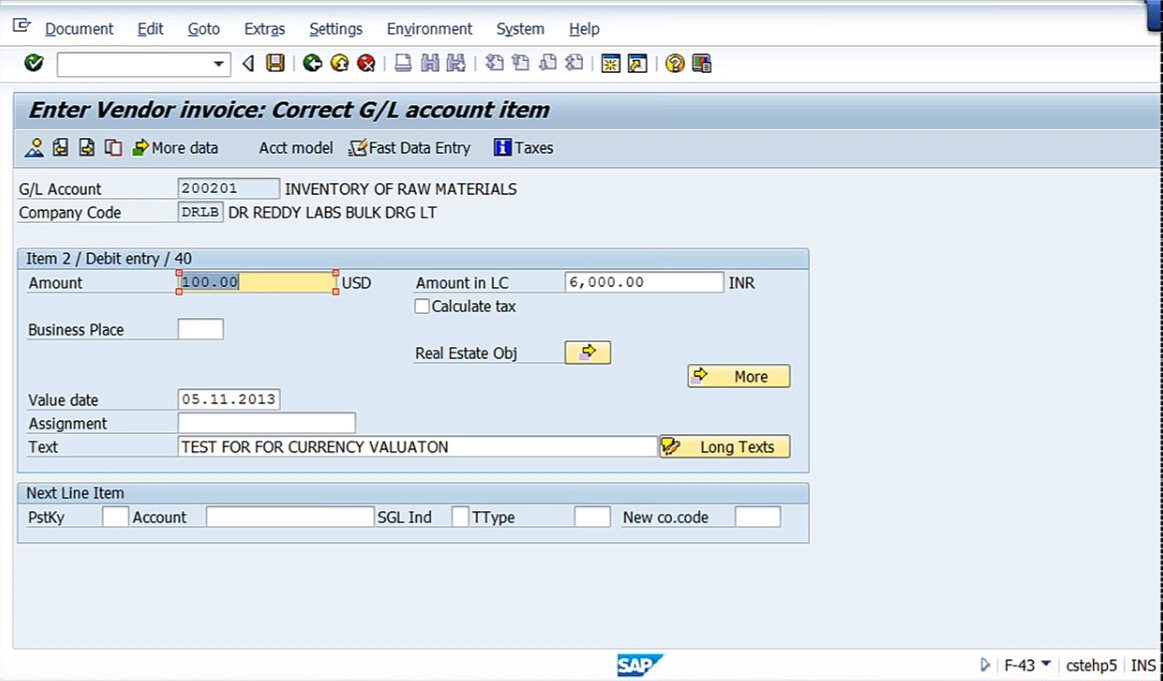

Next, what we do is, we enter the foreign exchange rate. So here, what we need to do, in order to exchange foreign enter the foreign currency, that is define your translation rate, at what rate we have to evaluate. So here, as per our requirement, what we told you is, on 110, raw material is purchased at 60. And, on 31st October, it is going to be 63. Now first, what I will do is I’ll post the accounting entry. Vendor invoice this is. Go to Accounts Payable, Document Entry, F-43. On 01.10.2013. Company code, DRLB, currency/rate USD. At what rate we are going to buy now, say, at the time of making payment, I need to define at what rate I’m going to buy. Sixty rupees. So one USD is equal to 60. ABC raw metal vendors. 400501.

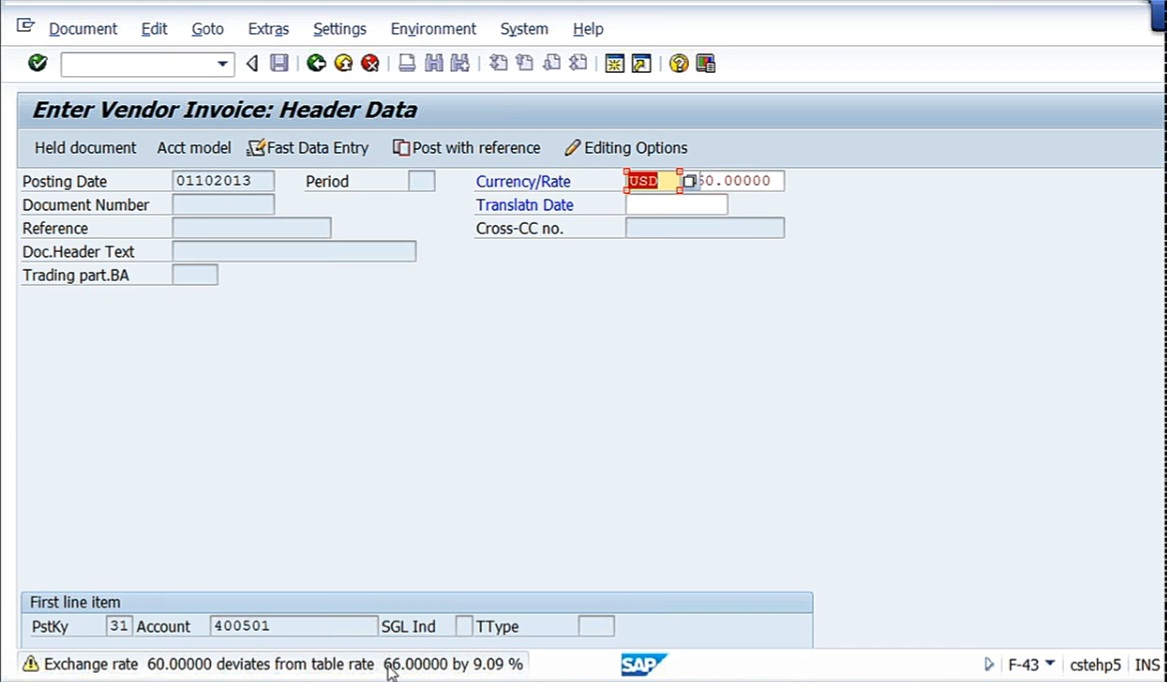

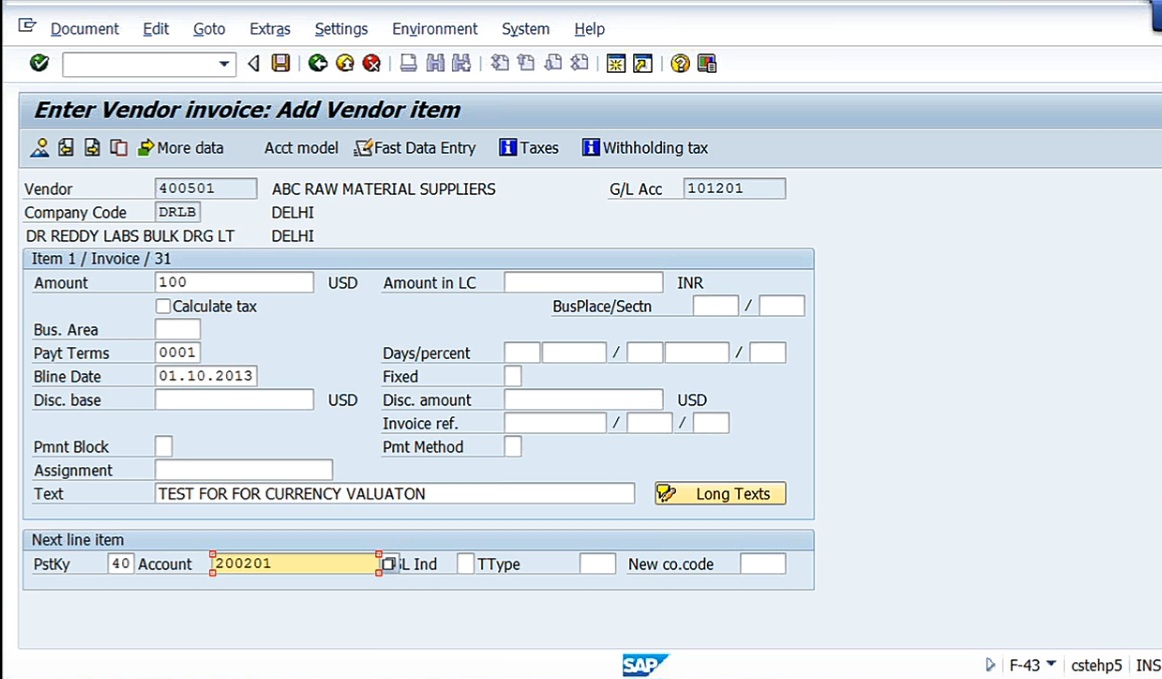

Okay. Already in the table, 66 has been defined. Continue. Now here, what I’m doing, let us take only just only 100. So test for foreign valuation. So vendor account is credit, then raw material account should be debited. So raw material account, 40. Account 200201, inventory of raw material. Inventory of raw material account return, raw material is received and vendor account is going to be credited.

So debit raw materials account.

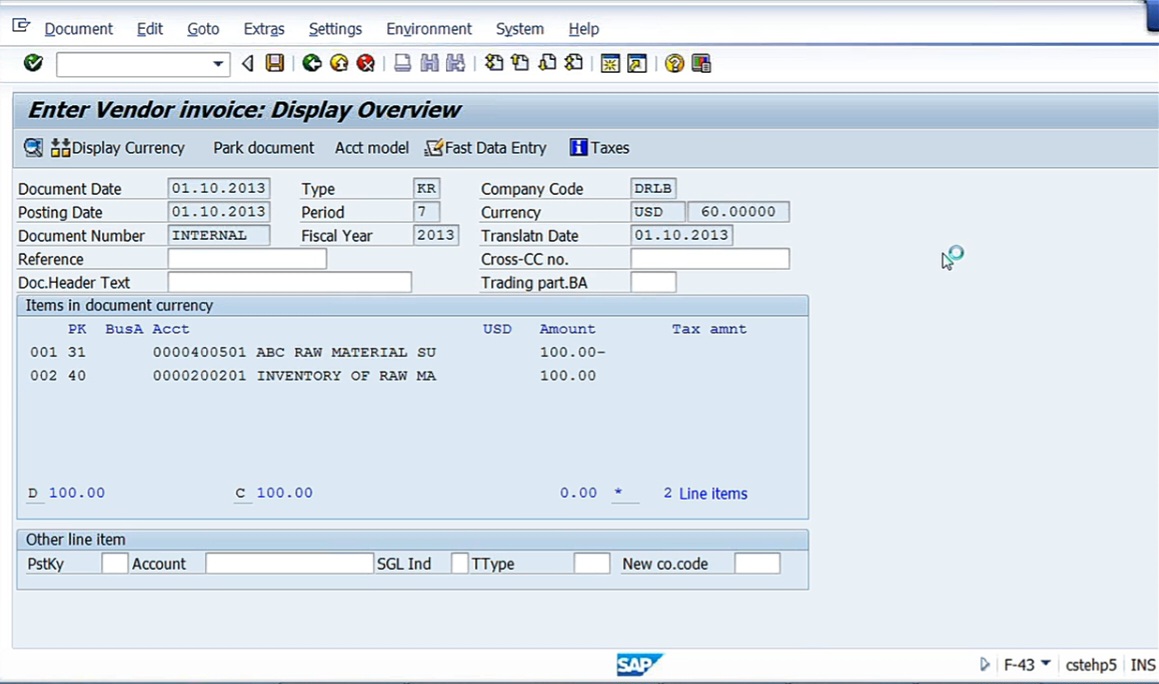

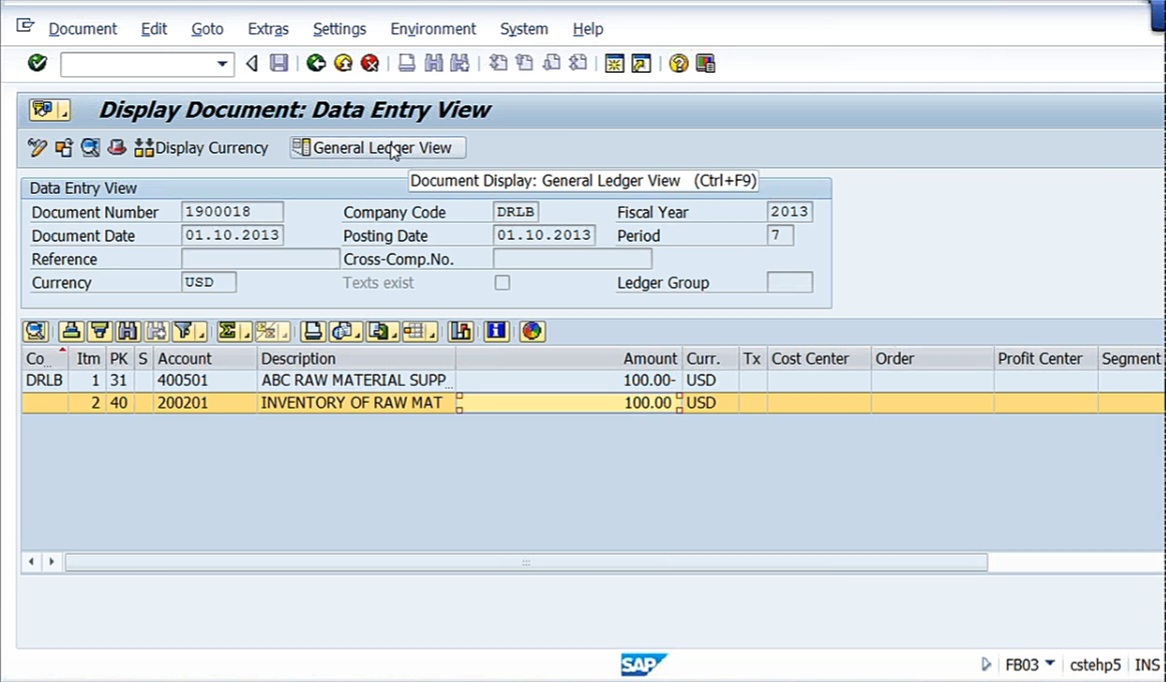

100 USD, 100 USD. Save it. You want to see the document, Go to Document, Display.

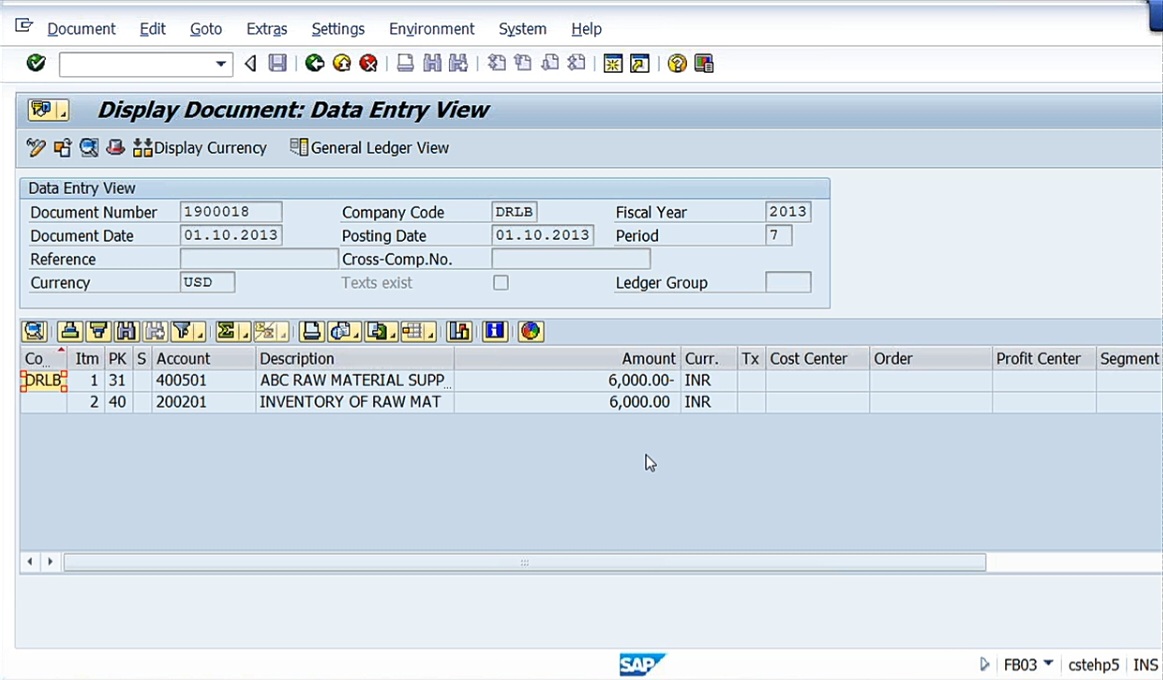

If you want to see it in INR. Click Display currency.

So let us stop here because again, a lot of process is there after posting the accounting entry, we need to valuate, the valuation process is there.