Foreign Currency Valuation 1

So loss on foreign currency valuation unrealized account return to balance sheet adjustment account. So this balance sheet adjustment account is nothing but that will be nullified. And, because now since there is a increase in the exchange rate, I need to book this expenditure because I need to take on in the balance sheet on 31st of October. Because on 31st of October, I’m going to prepare my balance sheet and P&L account. So at that time, I need to show to my shareholders what is my liability towards foreign exchange, loss or gain. If anything is there, I need to show in my books of accounts. So that’s why since there is an increase in the US dollar, if I’m going to pay today, if I’m going to make the payment to vendor today, I need to shell down 6,300 not 6,000. So that’s why 300 rupees extra I need to shell down. But this is unrealized because my due date is on 15th of next month, that is November. But as on 31st of October, I need to book the loss. Though it is unrealized, I need to book the loss. So that’s what I need to do. Loss on foreign currency valuation account return to balance sheet adjustment account. Since the foreign currency loss is unrealized, we need to reverse the above entry on 1st November 2013. Exactly the same because on 31st October, my books of account prepared, that is balance sheet and P &L account are prepared. In that, I have considered 300 loss. Since that is unrealized, I have to reverse the same entry. So I’m reversing it on 1st of November. So that is nullified. So what is the accounting entry? Same. Now, balance sheet adjustment account is going to be debited. The reversal entry can be Balance sheet adjustment account, debtor for rupee 300 to loss on foreign currency valuation unrealized account. So this gets nullified. This is only for the purpose of showing in my books that there is a loss. And it seems that is unrealized that I’ll be reversing it on the next day.

Now on 15th of November, payment of 100 USD is due, then the exchange rate is, say, 65 rupees on that date. Now the loss on foreign currency valuation is going to be 500, that is 60 minus 65. So now I have to purchase dollar at 65 rupees. So that’s why what I need to do is I need to buy the dollar for 65, that’s why my loss is going to be that 500 rupees. That is so when that account return 100 USD to bank account 100 at the time of making payment, what I do? See, in USD, I’ll be take only USD. But at the time of paying, I’ll be using here. Here it is going to be 6,500 and there are 2 things here, vendor account return to bank account because bank my outgoing amount is 6,500, not 6,000. My vendor account is showing 6,000 balance, that’s why my vendor account is going to be debited with 6,000. My bank account is going to be credited with 6,500, but the difference of this 500 is loss. Debit loss on foreign currency valuation realized. Say, account return 500 INR.

I’ll repeat the entire scenario once again. Try to understand once again. On 01.10.2013, raw material purchased on 45 days credit term, exchange rate is 60 rupees against 1 US dollar. So I’m going to buy raw material. So at the time, raw material account return to vendor account, 100 USD, 100 USD. So if I see my GL, system will show me 600 INR, 600 INR. On 31st October, this is as per foreign currency fluctuation. Foreign currency revaluation as per the accounting standards, if I’m not wrong, it is going to be accounting standard 21 or 17. As for India accounting standard, it is there like accounting standard of every country. Not only India, US, whatever it may be, we need to consider the loss on foreign exchange that valuation later. So that’s why here, on 31st October, I’m going to reevaluate my vendor outstanding amount. So I have to show to my shareholders what is the liability that we have towards vendor. So that’s why on 31st of October, 1 USD is equal to 63, and on the date 31st October, the liability of 100 USD is equal to 6,300. So the valuation of foreign currency on 31st October, if you calculate, it may be, see I’m showing you here only 1 US dollar. I may be paying different vendors with different currencies, maybe GBP or USD or euro or any other currency, whatever it may be, I need to valuate all the currencies. So that’s why we need system. It’s very simple, nothing is required.

So here, what I’m going to do, loss on foreign currency valuation unrealized account return to balance sheet adjustment account 300, 300. Since this is unrealized, not realized, I’m going to reverse it on 1st November. On 31st of October, I’ll be passing this entry, reversing on 1st November. So what happens now, on 31st October, my unrealized loss on foreign currency valuation will be showing 300 rupees extra, that is loss. So this should be booked to the P& L account. Any loss on foreign exchange, the currency valuation, we need to book it to the P & L account. Now, on 15th November, payment of $100 is due, on 15th November, we need to make the payment. So in such a case, then the exchange rate is, say, 65 rupees. So now the loss on foreign currency valuation is rupees 500 because 60 minus 65. So 60 rupees originally when we purchased it, now it is 65. So how that is going to be recorded by the system is vendor account return, it takes only 6,000, to bank 6,500 and loss, this is realized. Because since now we are actually making payment, loss now will be booked to the P & L account. This will not be reversed again. So this is the scenario. We need to see how system is going to take this.

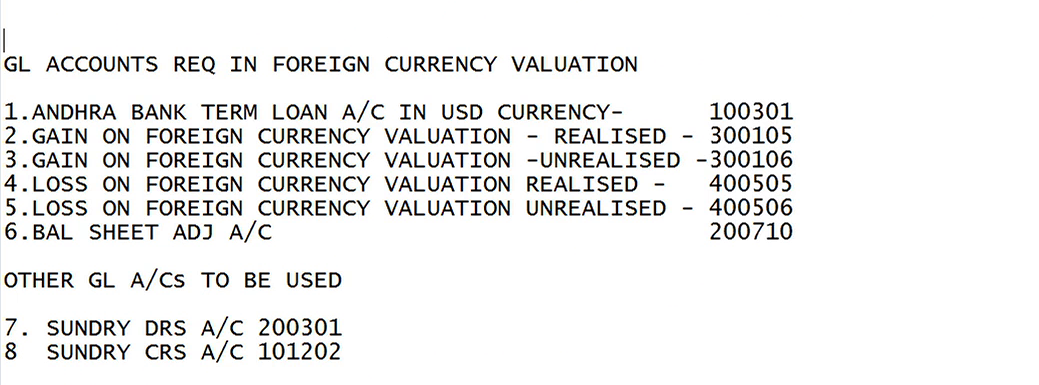

So GL accounts required in foreign currency valuation are shown below:

First one is not required. So, we have gain on foreign currency valuation- realized, gain on foreign currency valuation- unrealized, loss on foreign currency valuation- realized, loss on foreign currency valuation- unrealized.

Here, in this case, we got the loss. We don’t know in case of customers, if you’re making sales to customers, you may be getting gain. So for that purpose, I need to create loss accounts as well as gain accounts. And, this is going to be a balance sheet adjustment account. This is only an adjustment entry, adjustment only for the purpose of reversal. It will be nullified every time. We need not give any importance to that, that is only required at the time of posting the entry. So this is the scenario.

So, let us create a GL account. Go to FS00. I’m using gain on foreign currency valuation- realized – 300105. In Doctor Reddy Labs Bulk Drugs I’m creating. Account group, other income, and this is a P&L account.

Check line item display, sort key 001. Field status group G001. Save it.

Next is gain on foreign currency valuation- unrealized – 300106. I can create a template of 300105, and copy it.

Everything is the same except the GL account number.

Next, loss on foreign currency valuation- realized, 400505. So 505 is nothing but interest and financial charges.

Then loss on foreign currency valuation- unrealized, 400506.

Four accounts we have created. Then coming to balance sheet adjustment account, 200710.

So we have created all the GL accounts.

Now other GL accounts to be used.

So other GL accounts to be used is nothing but in a sundry debtors in case you are making the sales and sundry creditors when you are making a purchase of raw materials. So these are the things. First of all, we need to create regarding the master. The next is coming to the configuration.