Asset Accounting 7

So previously, we talked of 3 scenarios. All these three scenarios are also given in the notes.

Thank you for reading this post, don't forget to subscribe!

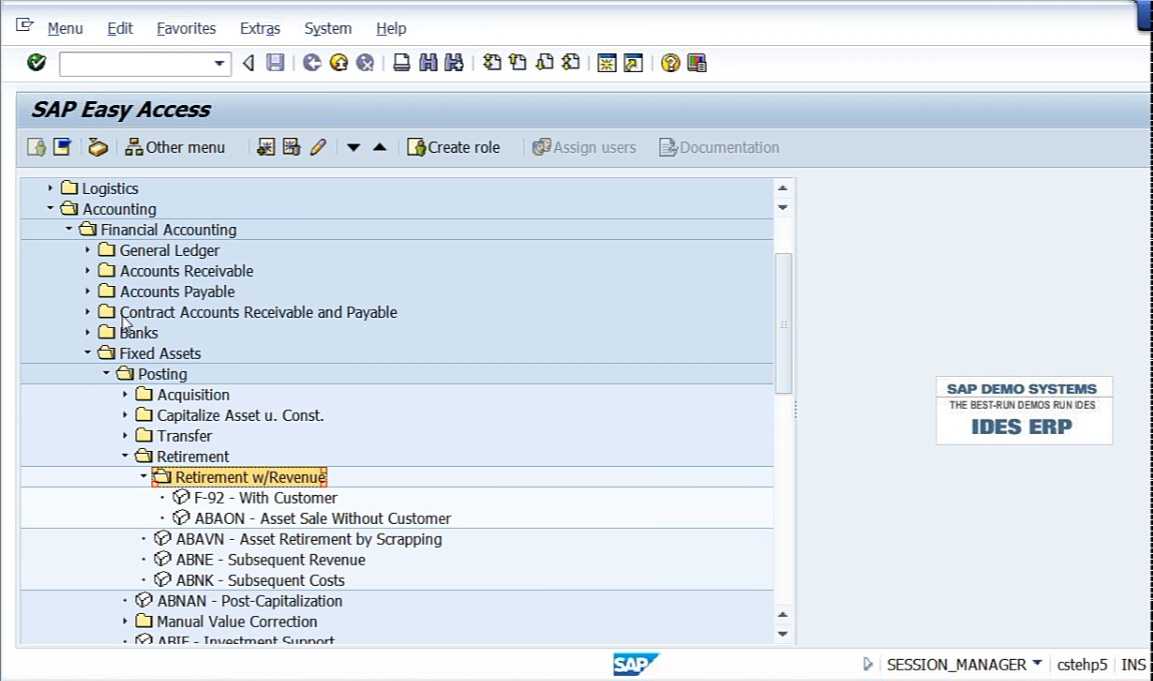

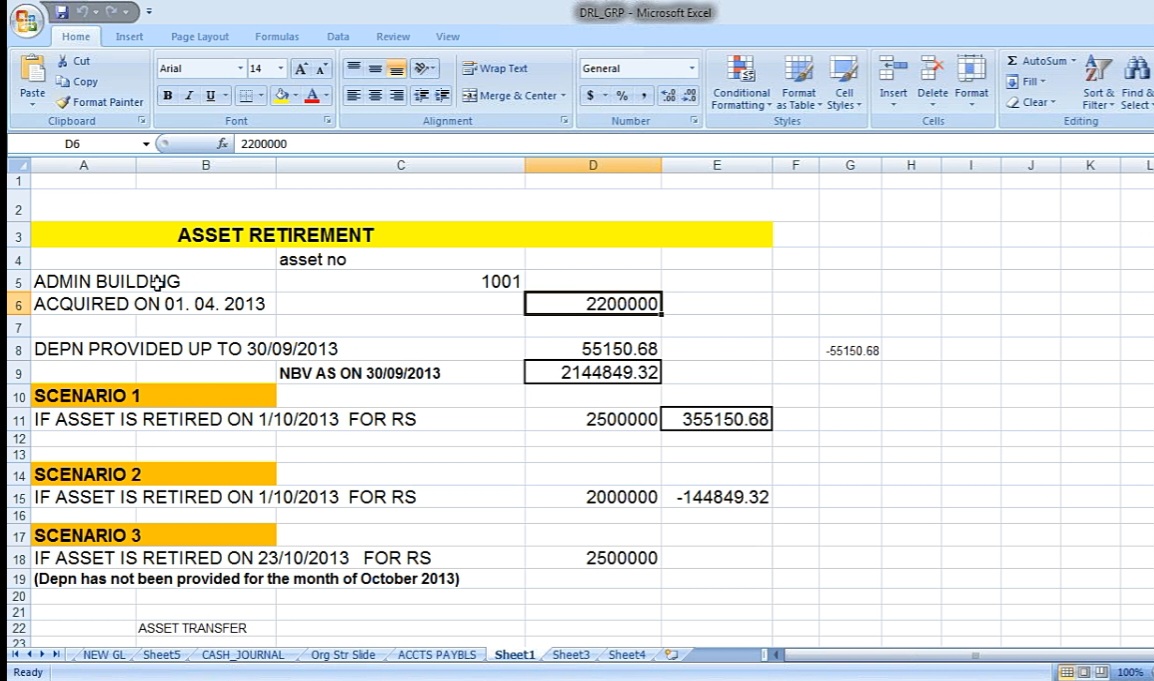

So admin building and, acquired on 01.04 and acquisition value is 22 lakhs, depreciation provided up to 30.09 at 55,150,150. The balance value is this much net book value is on 30.09. And scenario 1, if the asset is retired on 01.10.2013 for 25 lakhs, 355150.68 is the profit. If asset is retired on 01.10.2013 for 20 lakhs, -144849.32 is the loss. And scenario 3, if the asset is retired on 23.10.2013, and depreciation had not been provided for the month of October, whether system is going to consider depreciation or not. These are the 3 scenarios we are going to see now. Go to Accounting, Financial Accounting, Fixed Assets, Posting, Retirement, Retirement with Revenue with Customer.

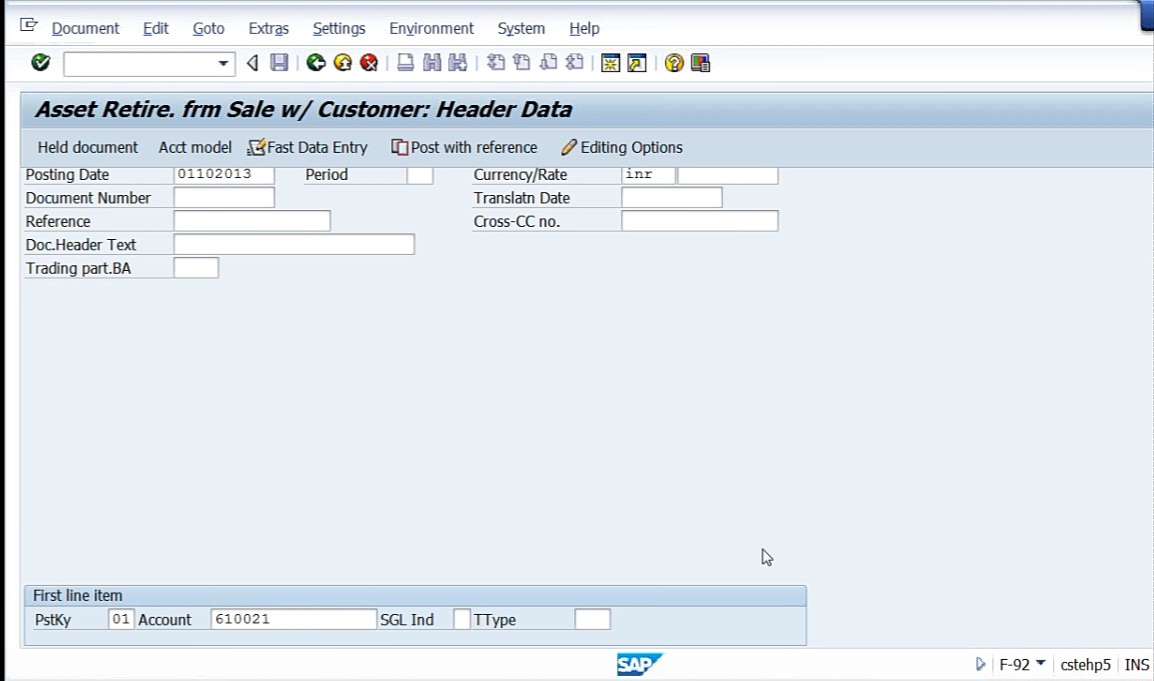

F dash 92 is the standard transaction code. Scenario 1, if asset is written down 01.10.2013 for $25,000,000. So this we’ll see now.

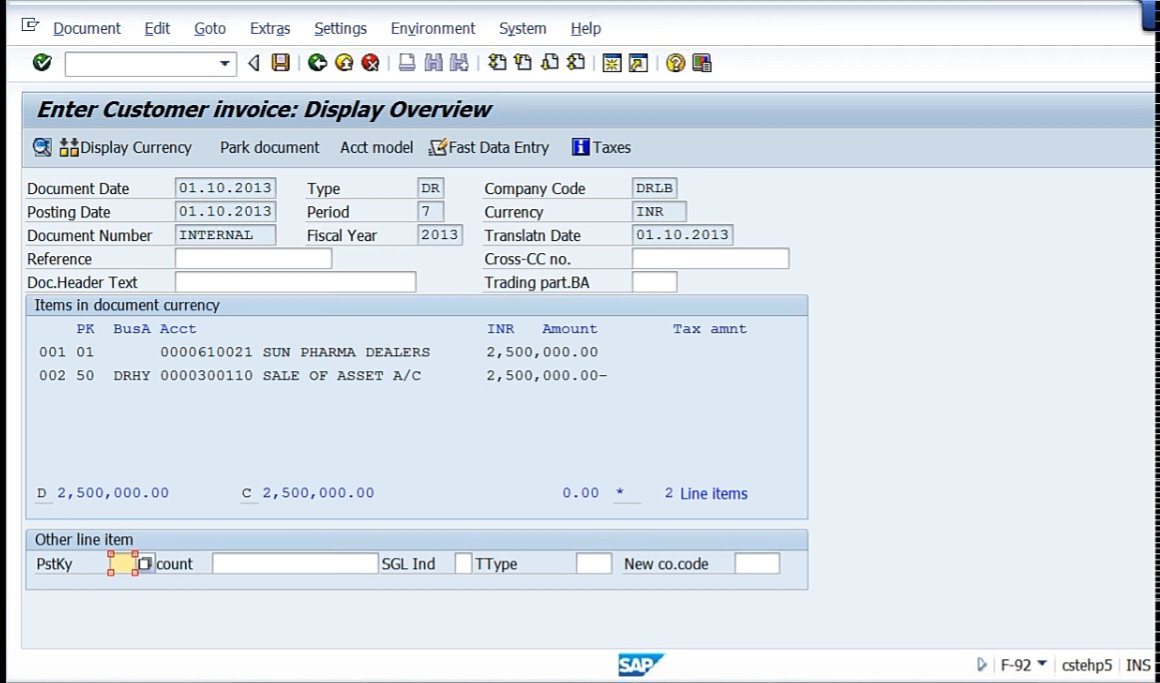

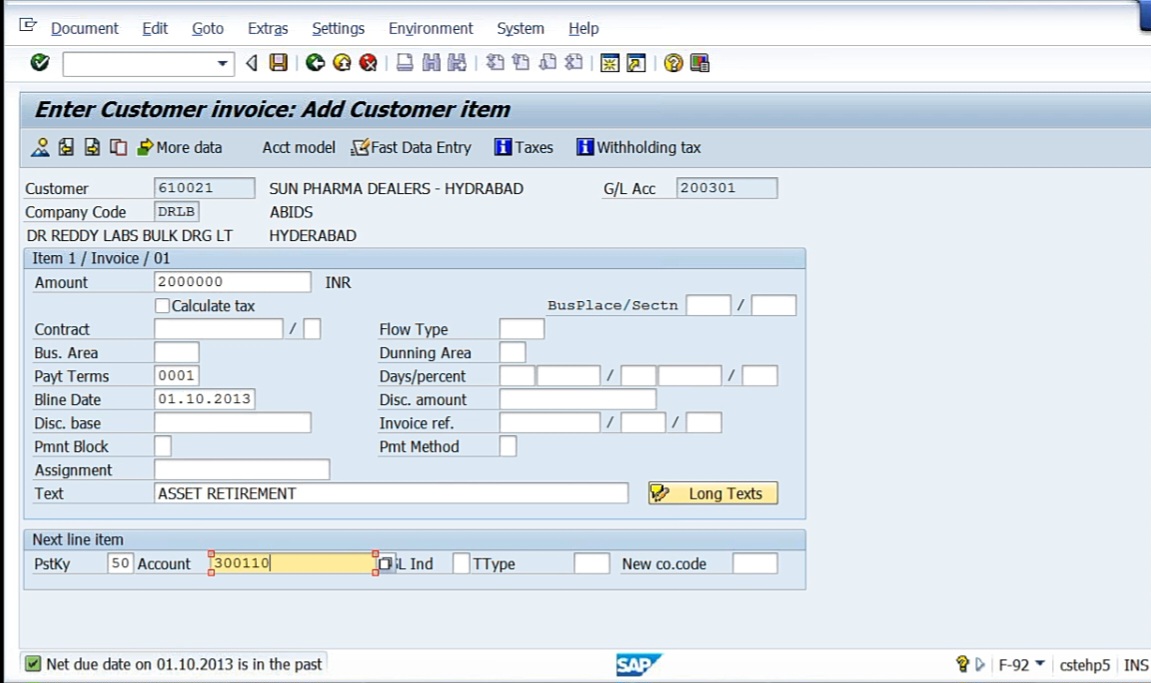

On 01.10.2013, I’m going to retire the asset. I have to sell it to some customer, I’m taking any customer Sun Pharma.

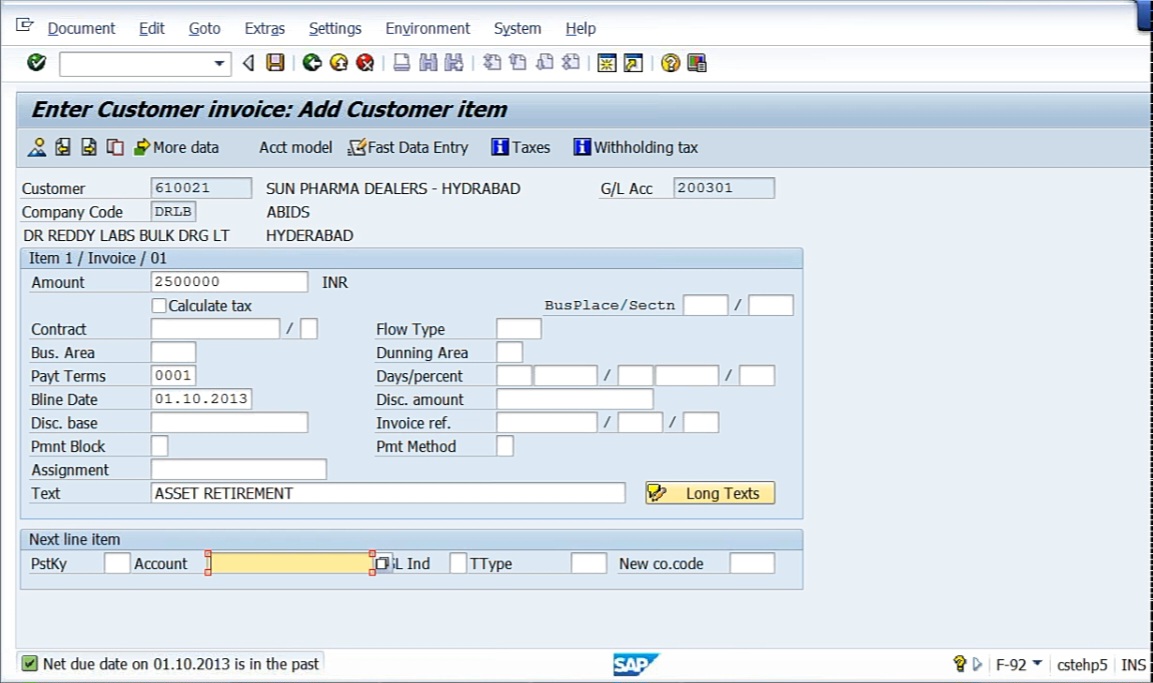

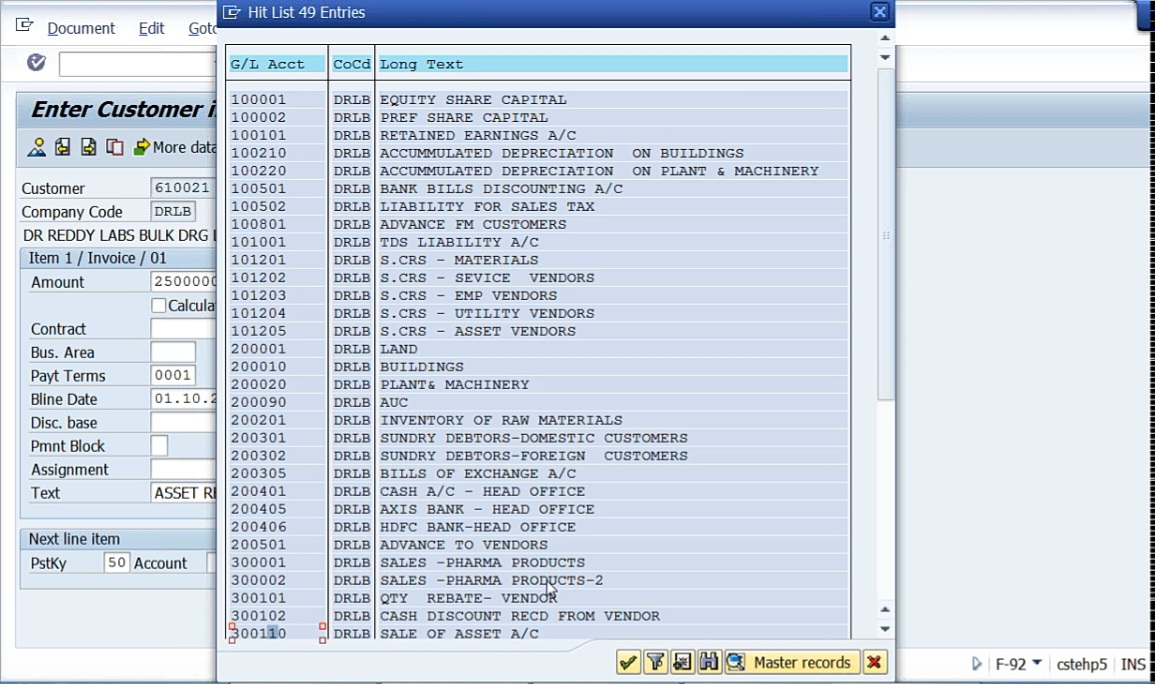

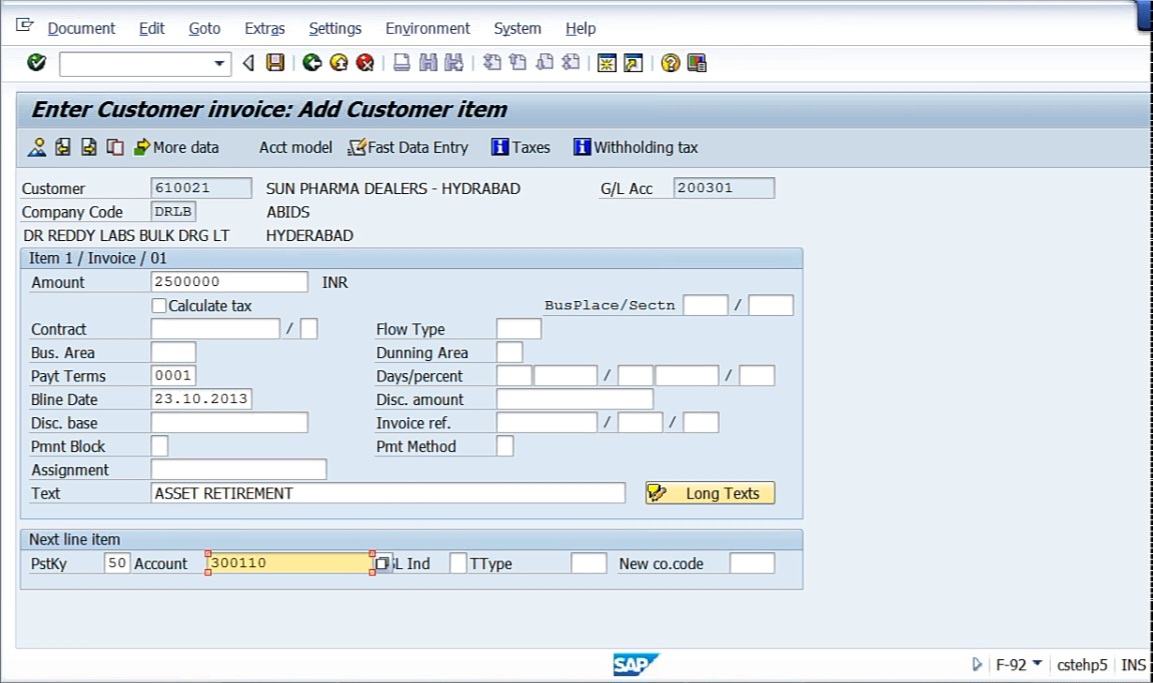

The asset value is 22 lakhs. I’m selling for 25 lakhs. See, generally, asset retirement means asset is going out, we are selling asset. Means, when we receive asset, we debit it. When it is sold out, asset is going out, then we credit it. Then whom we are going to debit? The customer. So customer account return to asset. So that’s why the Sun Pharma have taken one customer, and this customer account is debited. Customer debit is 1 for 25 lakhs. And posting key here, generally, customer account will return to assets. But the peculiarity here is we should not use the asset now because if I give the asset, asset number I have to give here. So that’s why here, what we have to do, while doing the entry, you remember we have created one GL account called sale of asset account.

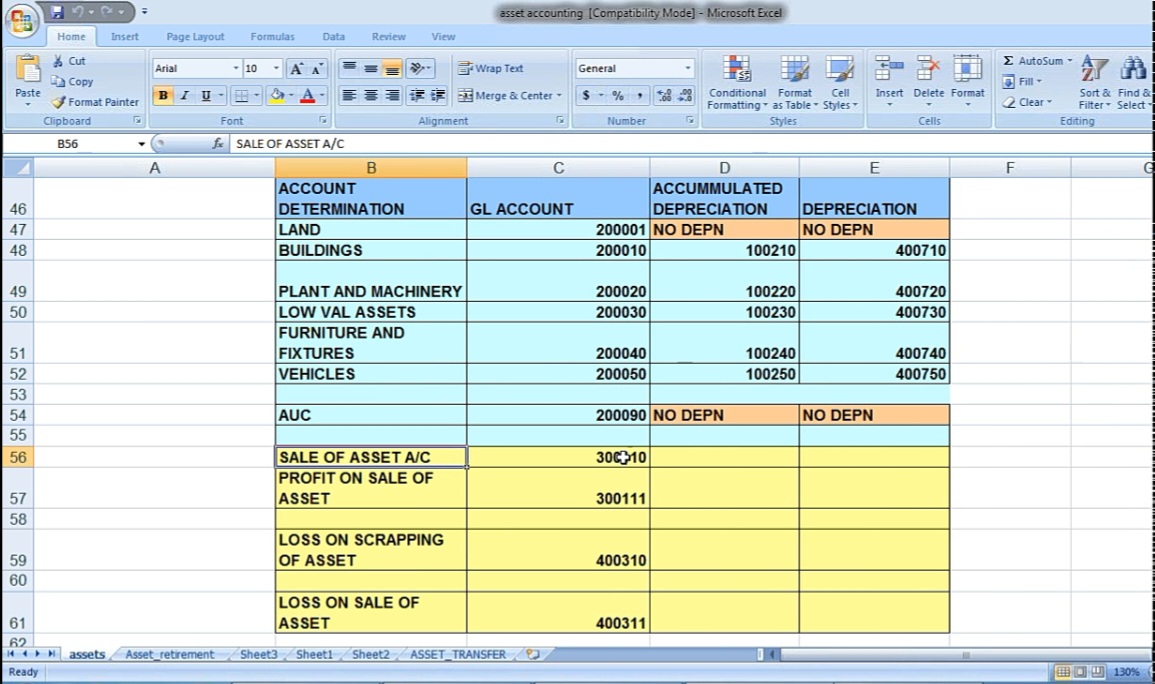

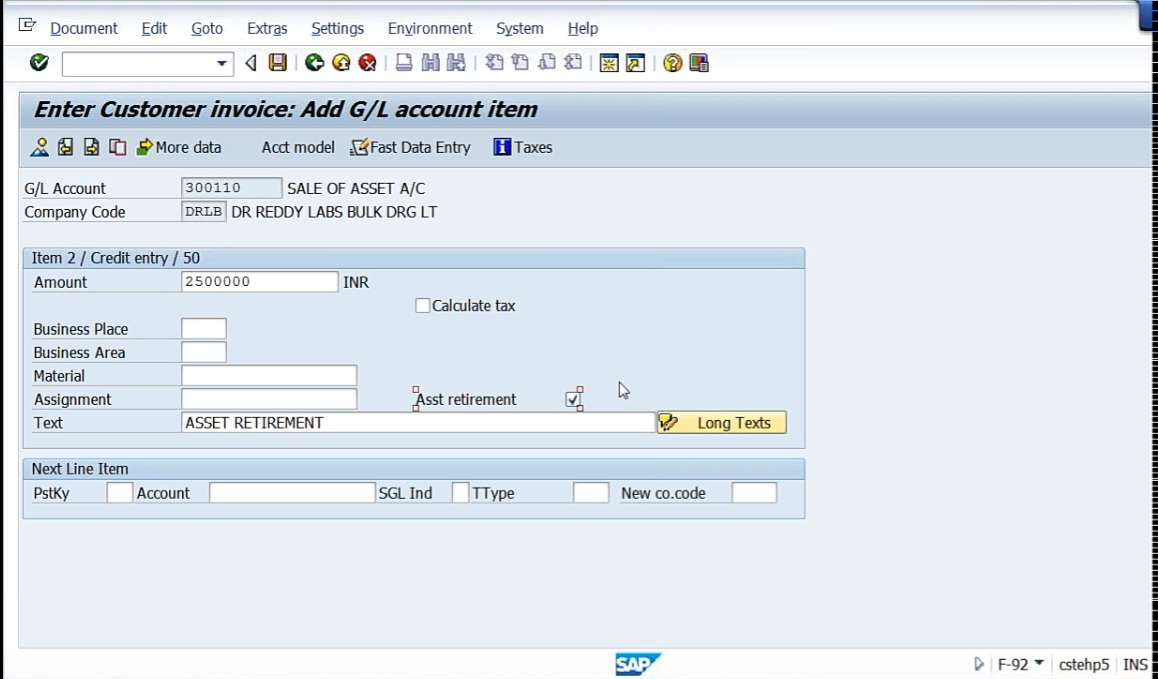

See here, sale of asset. Sale of asset, in case of manual accounting system, there is no account of this kind. But here, sale of asset accounting is only,l an account which is going to be used for the purpose of nullifying the entry, that I’ll show you how it works. Here, I need to take sale of asset account. Sale of asset is 3 lakh 110.

Press enter.

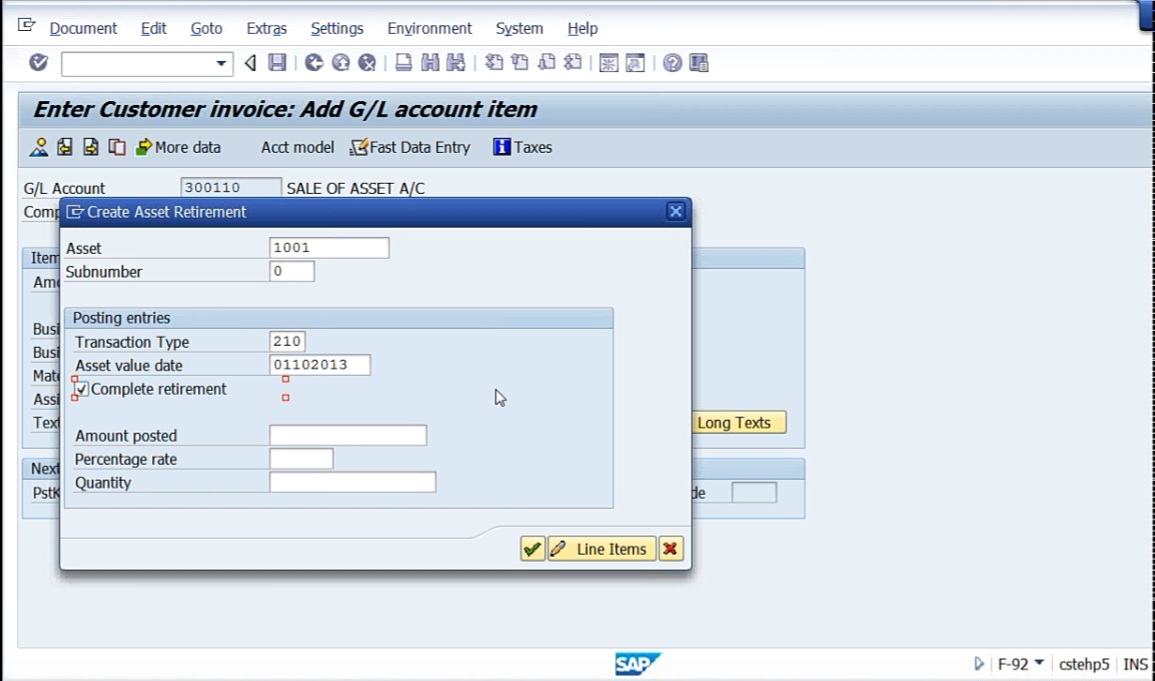

And if you remember, sale of asset account we have given field status group G052 in FS00, G052 accounts for fixed asset retirement. This is very, very important. If you take this field status group, then you’ll get asset retirement. If you don’t take that, it will not come. So that’s why this is very important here. Once you check this asset retirement box, press enter. Now system will ask you which asset you are planning to sell away. That is 1,001. What is 1,001? administrative building? Sub number 0. Asset value date, we thought 01.10.2013, complete retirement.

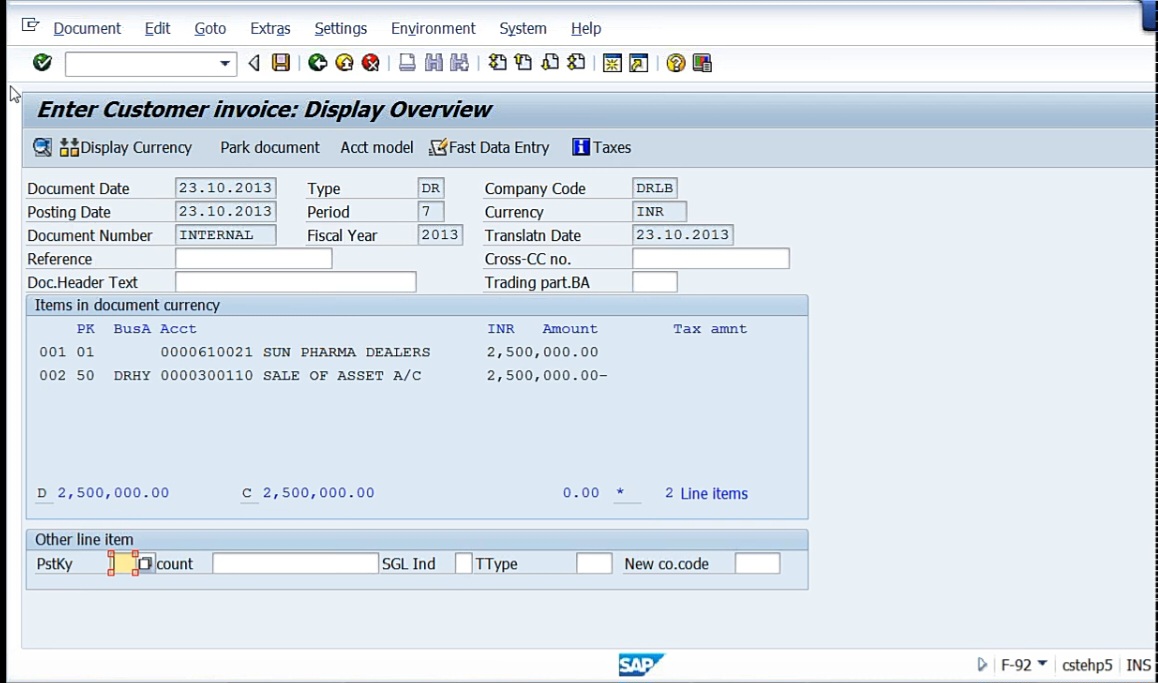

So we are telling to the system, this is the asset we are going to sell, the asset value date is 01.10, because up to 30th September, we have provided depreciation. That’s all. Click overview, you can see only line items which we have entered.

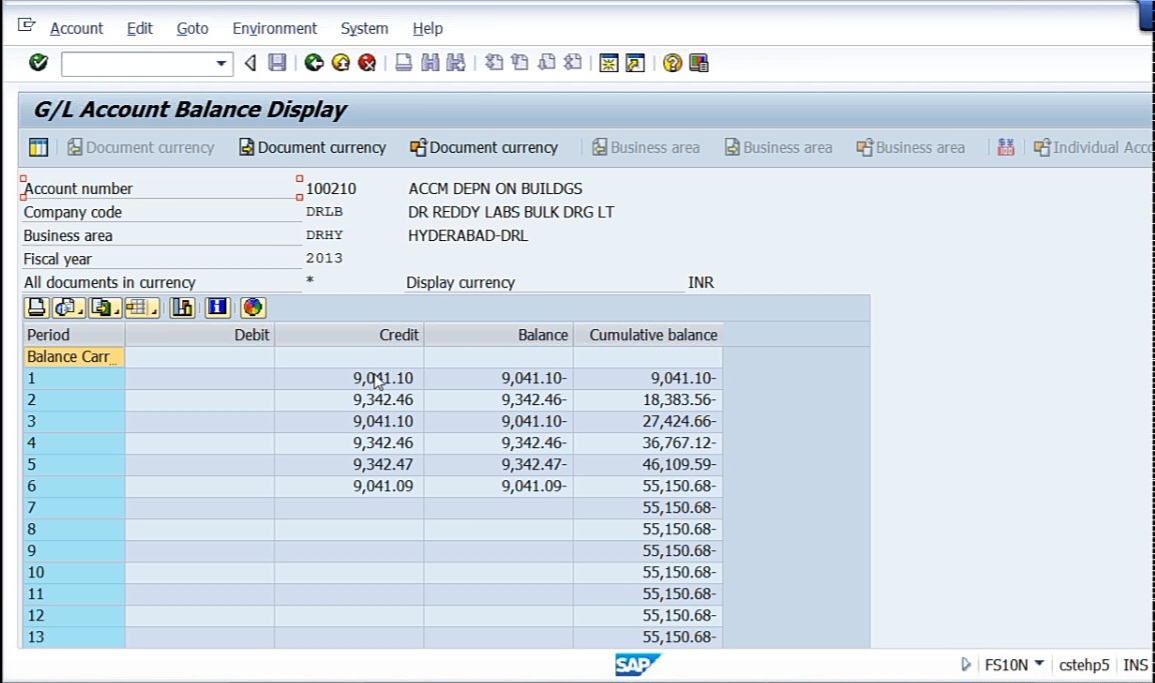

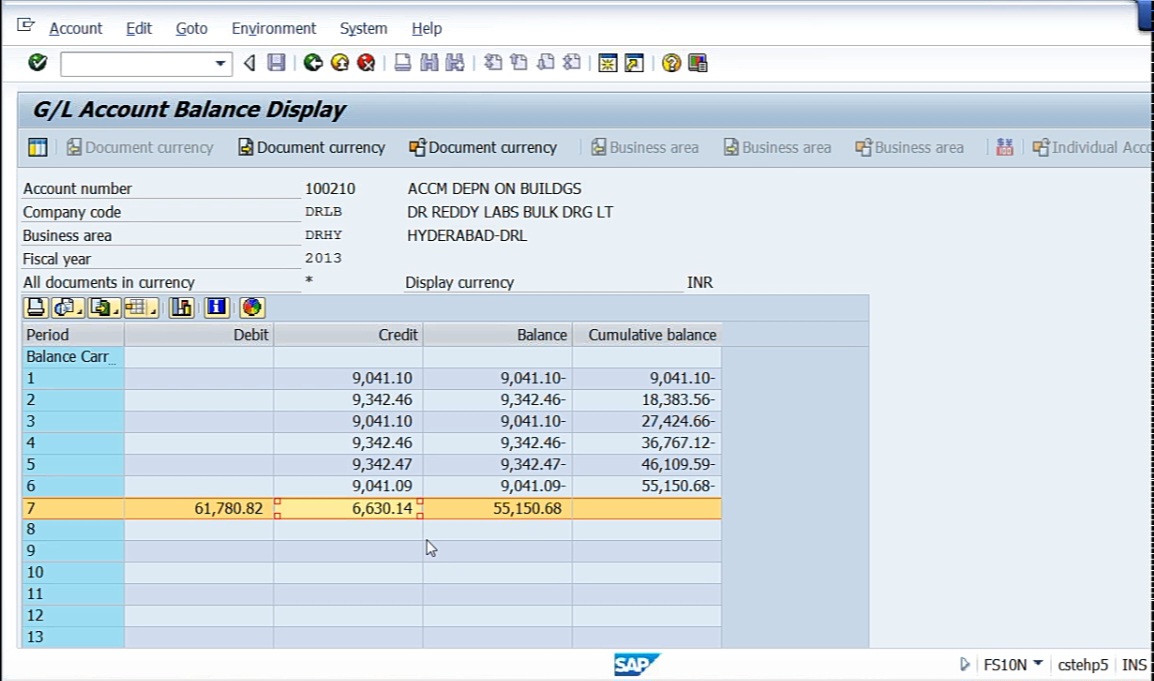

That is customer account is debited, asset account is credited. Now what is the entry we require when you are going to sell an asset? Asset account, when we have received, we have debited it. Now it is going out, we have to credit it. Then what about the depreciation? We have already provided depreciation, and that will be shown in the accumulated depreciation. So whatever the depreciation, that we show here, say FS10N to see the GL account. And if you see the accumulated depreciation on admin buildings.

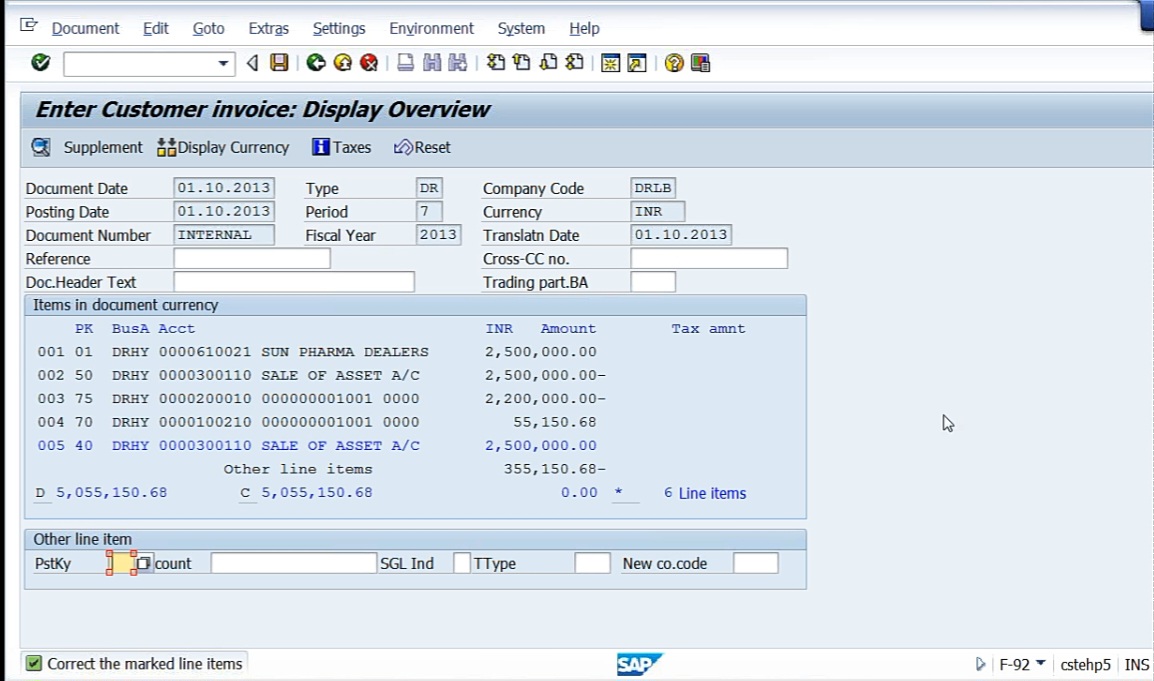

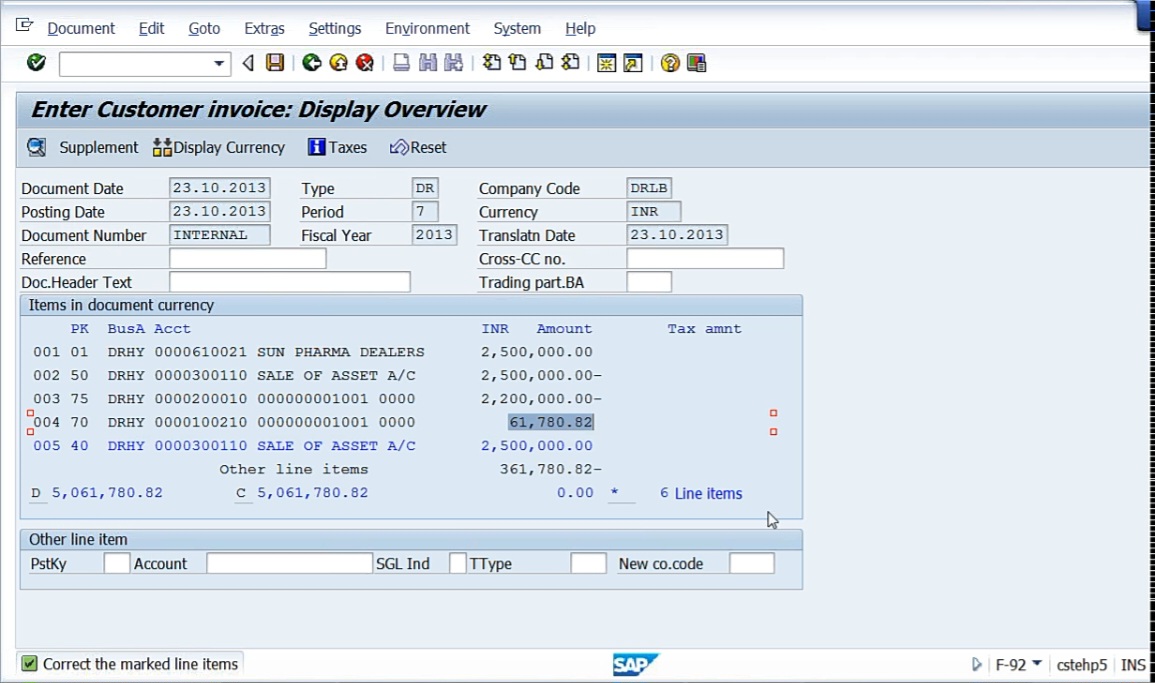

See, every month whatever you have provided, depreciation account returned to accumulated depreciation. So 55,150.68 is showing credit balance. Now asset account has to be credited. Now accumulated depreciation, whatever is there, to nullify this, it will be debited. Then what are the profit that we are planning here? Profit is going to be 359,150, this should be credited. My accounting entry should be since asset is going out, asset value should be credited with 22 lakhs, accumulated depreciation to be debited with 55,150.68, and profit or loss, whatever it may be, the profit is going to be credited. Simulate it now. You’ll get 2 extra line items that is sale of asset account. The sale of asset account will get nullified. It will get plus minus.

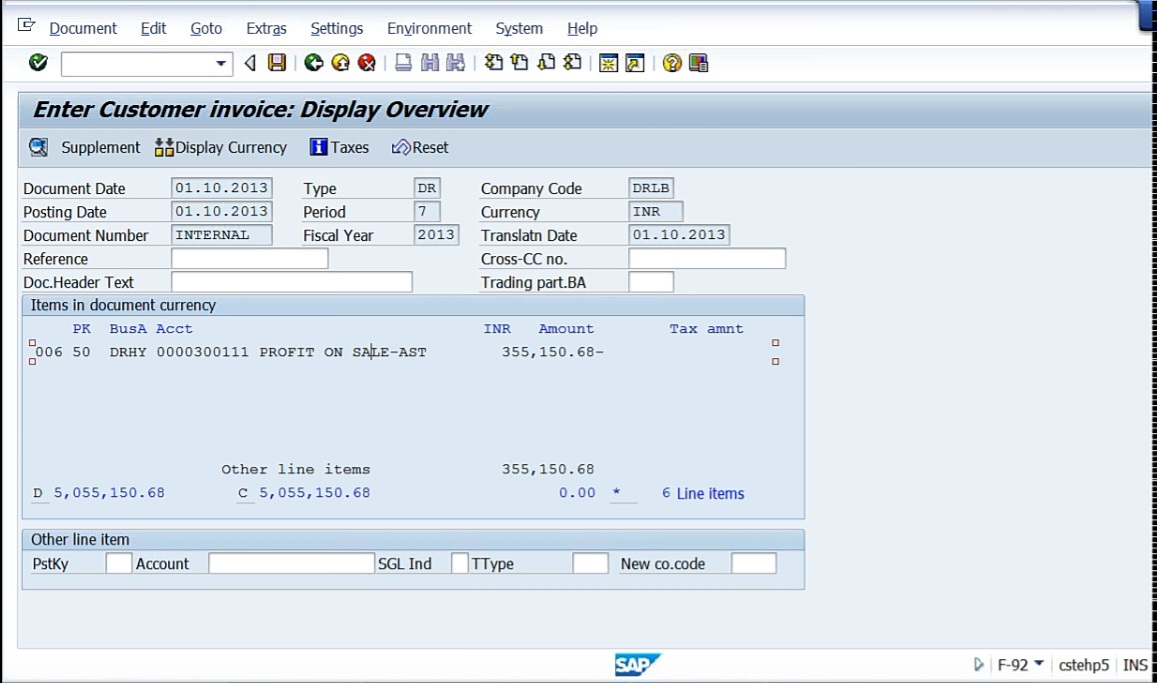

See here, First is Sun Pharma customer account is debited. Because he’s taking the asset, his account is debited. Now here, Sale of asset account, 50, that is credit, 25 lakhs. Also, Sale of asset, 40 debit. So with this debit and with this credit, system gets nullified. This account, no more. Debit and credit is posted here, so that will be nullified. That’s why we need not give any importance to the sale of asset account. That is only which facilitates for the creation of this accounting entry. Now I told you asset account, when we have received it, we debit it, but when the asset is going out, it will be credited, so 75 is asset credit 22 lakhs. 2 lakh 10 is the nothing but GL account for the buildings. And line item 004 is accumulated depreciation. When we provide depreciation, that will be credited. So to nullify that, now it will debit it 55 lakhs 150. Anyway, this is the sale of asset account. Other line items balance is 33 lakh 55,000. If you use page down, you’ll see profit on sale of asset.

How system knows that this is profit? How it has posted to exactly this account? I did not give an entry. All this 6 line item system generated for asset retirement. Because based on the profitability, if it is minus, then it will be credited, if it is a plus, it will be debited. So for this, we have already given assignment, that is in the t code AO90. All the integration of GL accounts have already been given, that is step number 9 or 10. Because of that, this accounting entry will get triggered. If you get this entry, your configuration is correct. Now I’m not saving this because I want to show you in case if I sell for lesser value, whether I’m going to get a loss or not. Because, in this case, system is triggering profit account, profit on sale of assets. Now I’m not saving this. Rather, what I will do, I’ll reset.

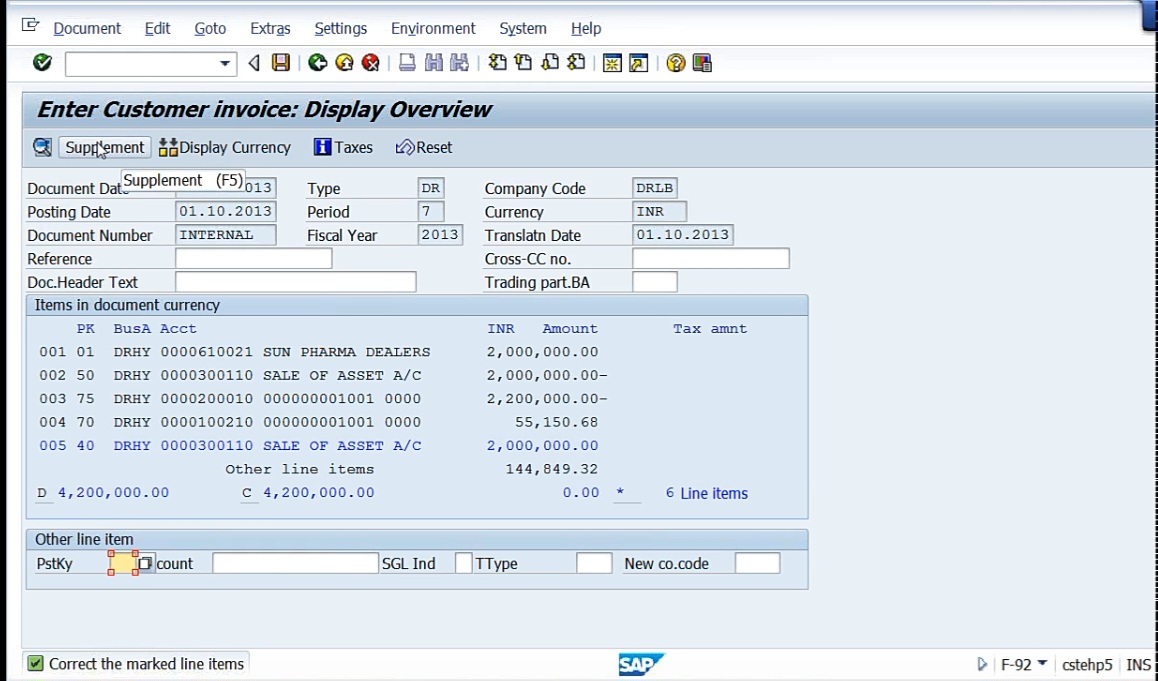

So now the second scenario is if asset is retired on 01.10.2013 for rupees 20 lakhs. Let’s take 20.

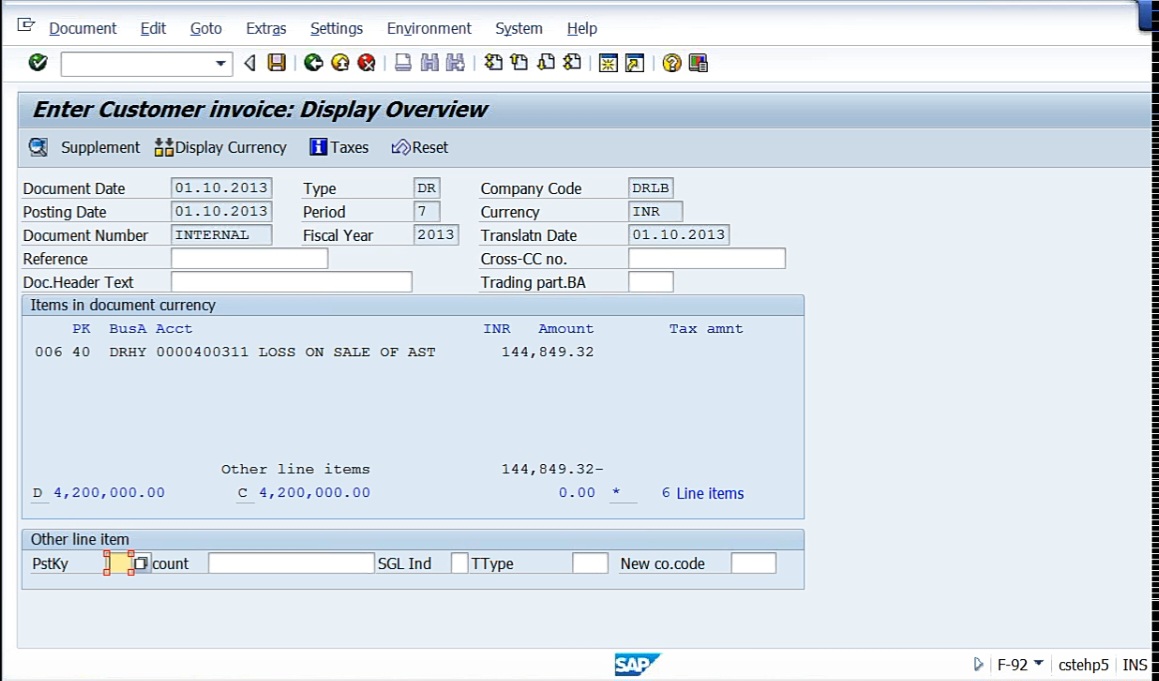

See? 1 lakh 44849.32. Rest of the things are the same. Pharma dealer, this customer account is debit. Sale of asset account with 20 lakhs get nullified. Now fixed asset account with 22 lakh because at the time of procurement, we have paid 22 lakhs, the same entry. And 004 is the depreciation, there’ll not be any change. Same depreciation that will be debited, and if you page down, 1 lakh 44 loss on sale of asset.

See how system knows when there is a profit, system is triggering loss on sale of asset. When we get the profit, it has posted to profitability account, that is profit on sale of asset. So system knows that because we already made a configuration if it is loss to which account, if it is profit to which account. So all those things we have already given to the system.

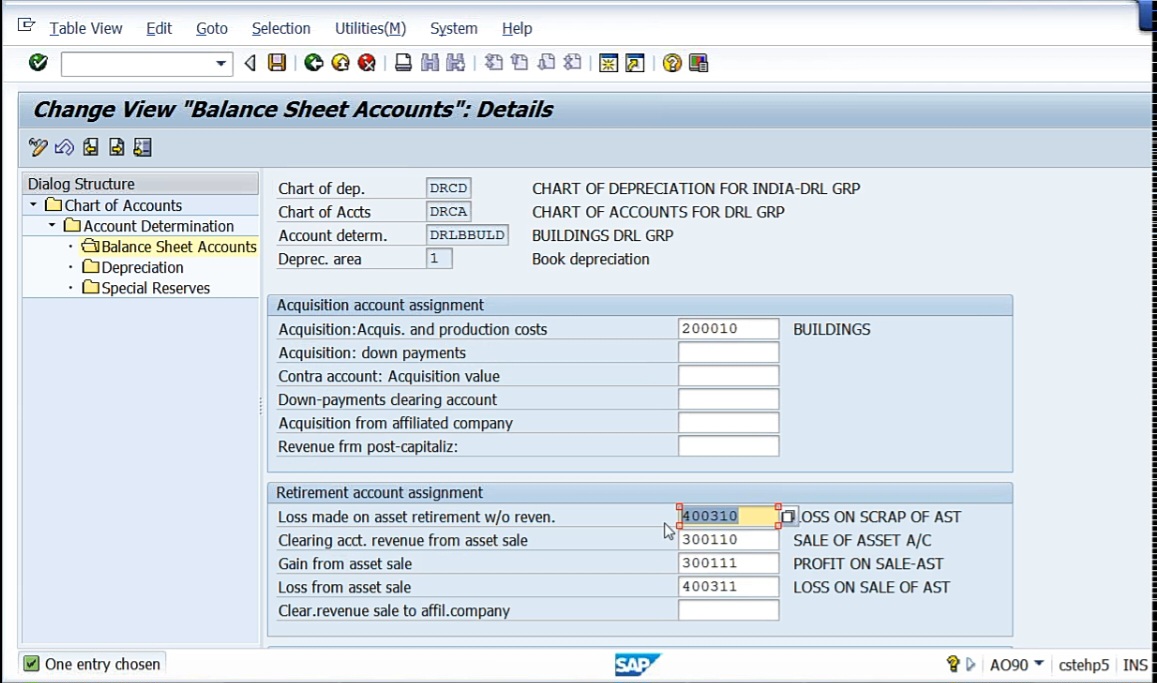

So I’ll show you. Go to KO90, chart of depreciation DRCD. Under Account determination, select buildings. Select balance sheet account.

See, here we have already given the respective GL accounts. If you enter the GL accounts wrongly, then you get wrong accounts only. So here, we need to be very careful while assigning the GL accounts. If you do anything wrong, the accounting entries you’ll get wrong. So that’s why you have to be very careful with this. So this is the accounting entry.

Then if I’m going to sell the asset on 23rd, but depreciation has been provided only up to 30th September. So if we don’t provide depreciation, so, generally, it is periodic, that means at the period end only we provide depreciation. So now we are in the middle of the month, we are retiring the asset. So in such a case, we need to see whether the system is going to consider for this 23 days of depreciation or not.

Simulate it.

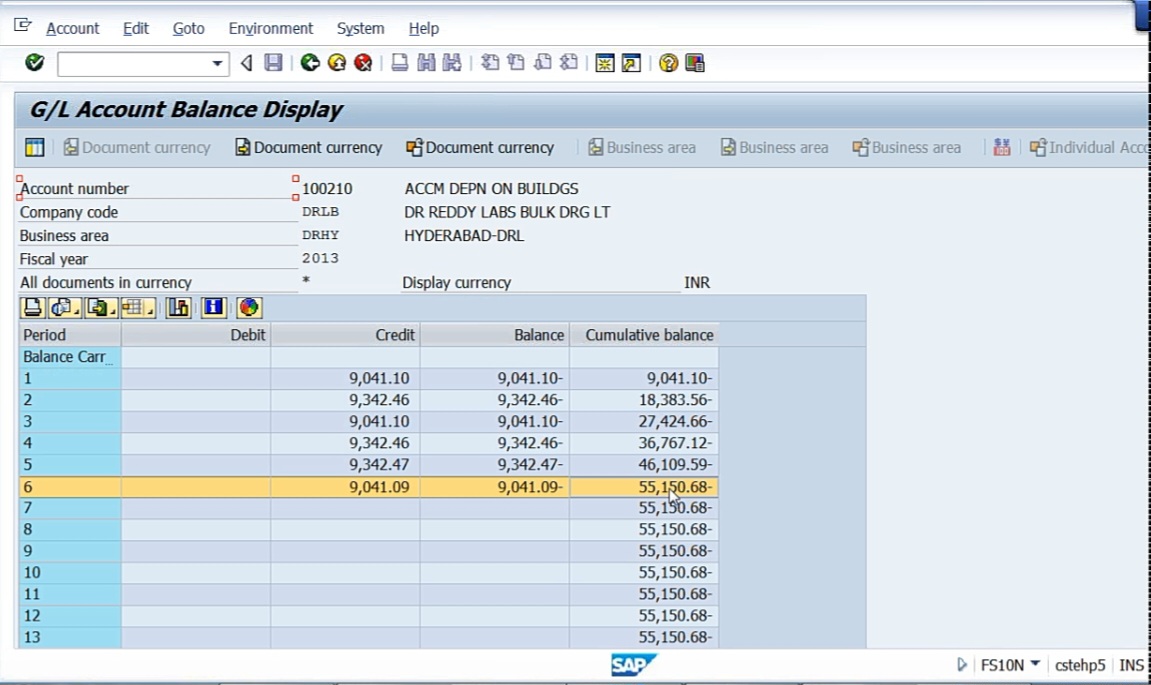

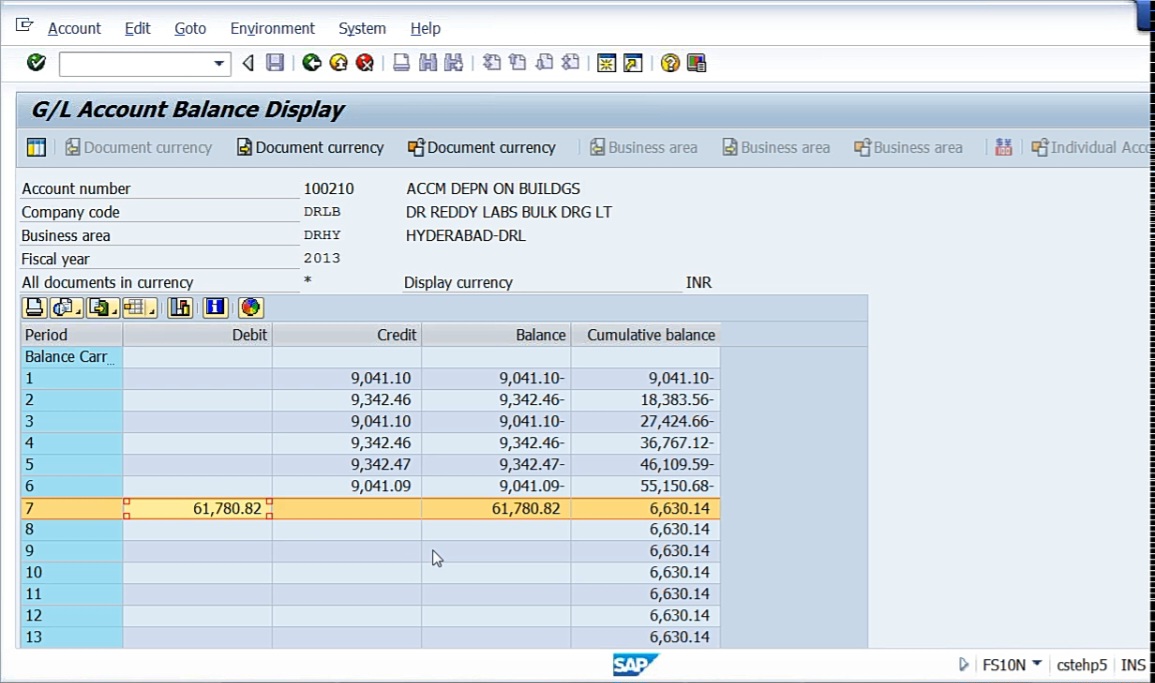

See, accumulated depreciation is 61780. But as per our calculation, depreciation is 55150 up to 30th of September. So on 30th September this much, and the difference 55150.68, that’s 6,000 plus the system has calculated. So that means to say, even though we have not provided depreciation, if you have plan to retire it, system will provide depreciation for the current period. Accumulated depreciation account is going to be reversed. See, system is reversing 61. But if you see here,

See accumulated depreciation, 55150, that’s why this credit balance is there. Now 61780, system will provide debit balance now. Means the differential amount, that is, differential depreciation will be provided when we execute depreciation for the next month. Now this entry, I’m saving now I have to show you how it works. So display the accounting entry. So with 6 line items, when you return an asset, it will show you 6 line items.

See, Sun Pharma dealers 25, this is debit. The two Sale of assets are credit. If you remove these 2, 1, 2, 3, 4 line items. First line item is customer debit, line item 3, 22 lakhs asset credit, and line item 4 is accumulated depreciation, debit, that is reversed. Accumulated depreciation, whenever you provide, it is credited. Now it is debited, which means reversal. Profit on sale of asset, 3 lakh 61,780.82. This is the accounting entry. If you go to the GL account, just go and again reenter.

See, system has provided debited. Till now it was credited, it is debited. 6,630 is the depreciation, which will be reversed. Means it will be provided and then it will get nullified.

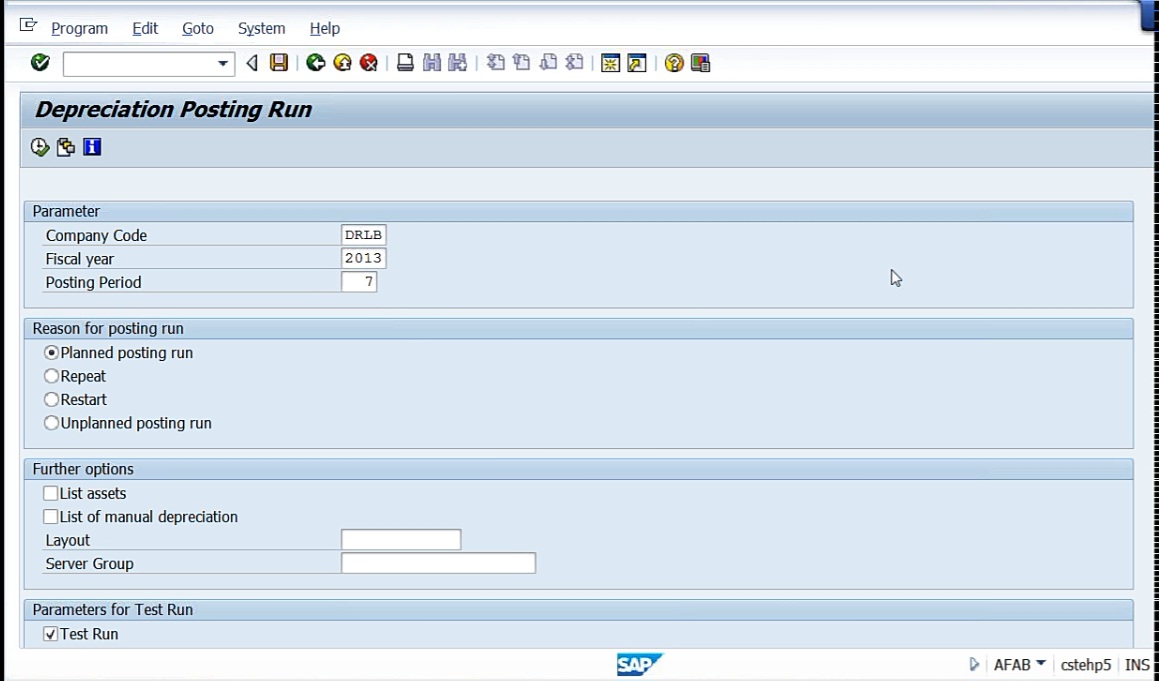

Now, I’ll provide depreciation for the month of October. So depreciation T code is AFAB, that is periodic processing.

If we Test run.

Select first entry.

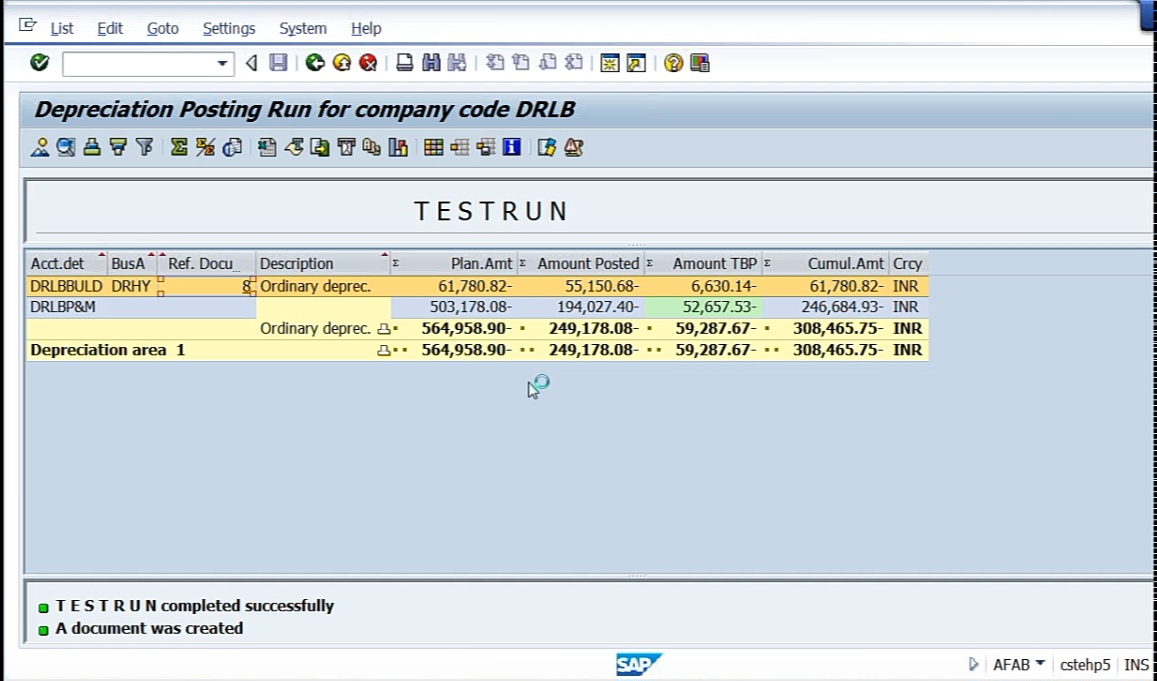

6,630.14, exactly the same depreciation system is providing. Alright. Remove the test run. Go to Program, Execute in background. Select output device LP01. Start time, select ‘Immediate’. Then save.

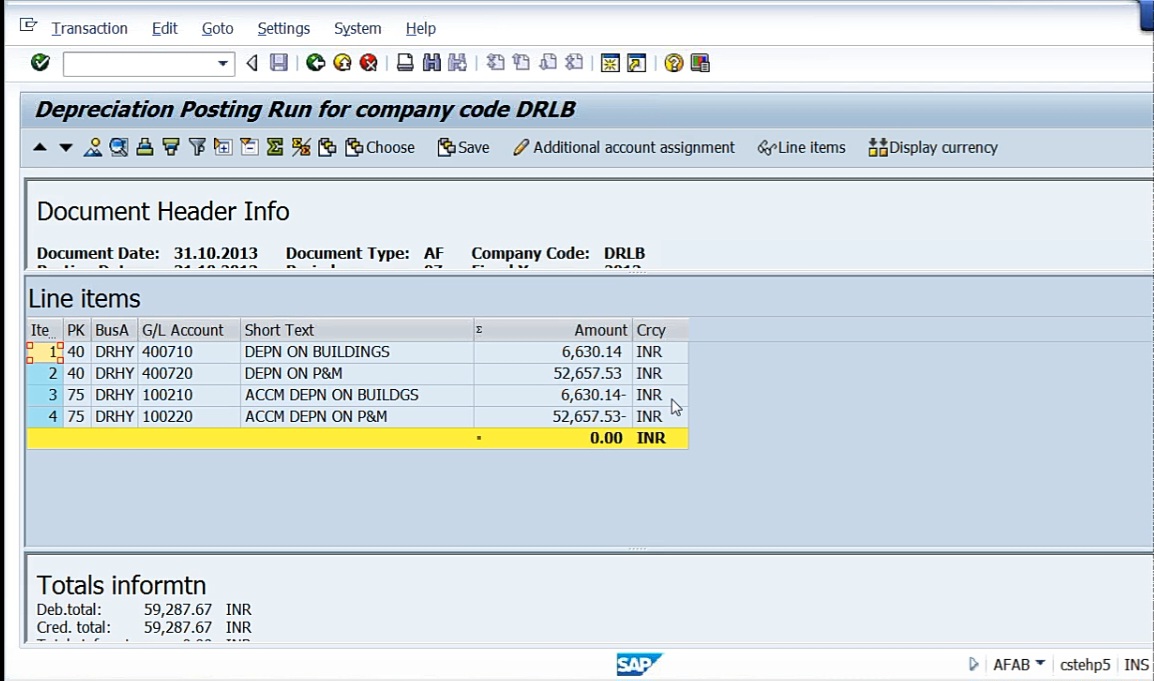

Depreciation is provided. Now go to this account and see. Before depreciation was not provided, now it will be provided and it will get nullified.

See, 6,630. So at the time of retirement, the system considered a depreciation up to the date on which we have sold the asset. But the depreciation will be posted only when you execute the depreciation. Till then, in the accumulated depreciation, it will not get reversed. So system will reverse the total depreciation whenever we execute the depreciation, depreciation will be provided. So this is asset retirement. So retirement is nothing but sale of asset. When we sell the asset, the system considers the net book value and whatever the value that is appearing in the books of accounts, and then it calculates profit or loss based on the sales value. So these three scenarios you work out on that, you’ll get it.