Asset Accounting 6

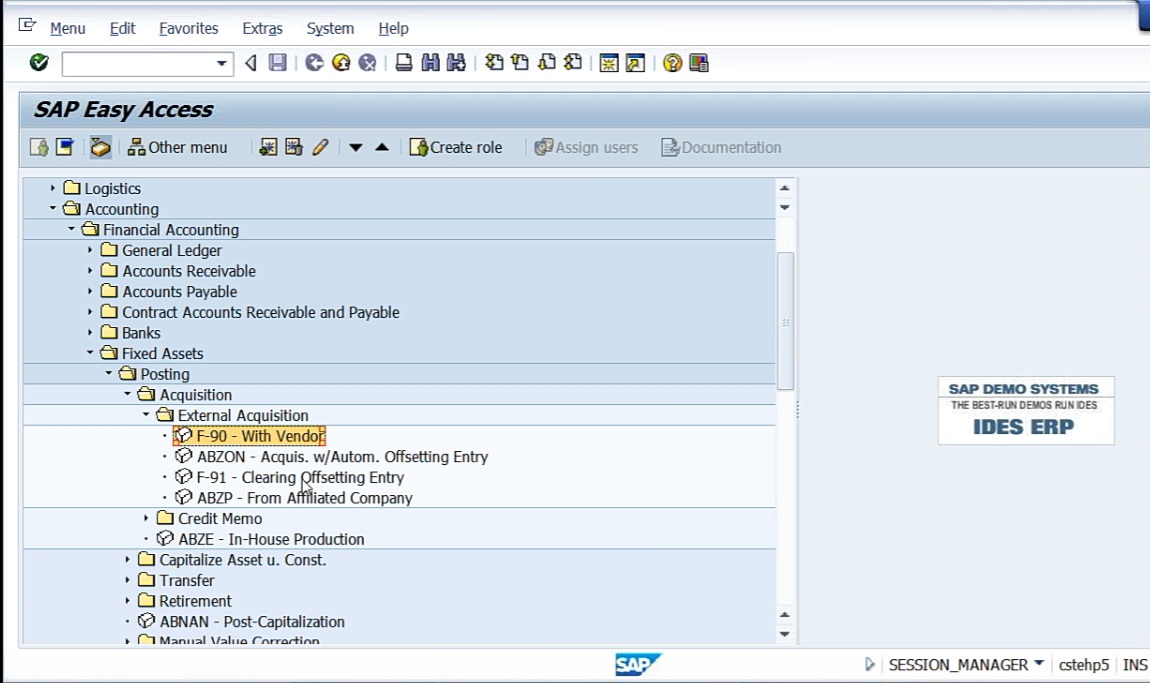

So we are going to acquire the asset. For acquiring the asset, Accounts Payable, Fixed Assets, Posting, Acquisition. This is External Acquisition. Why specifically it is stated as external acquisition? Because asset can be developed within house also. Say, for example, in my factory premises, I’m constructing factory building. So that is internally generated asset. That is not external acquisition. Now we are going to see. So that comes under asset under construction, AUC. So but here, we are looking at external acquisition. Again, external acquisition is with vendor.

Thank you for reading this post, don't forget to subscribe!

F-90 with vendor. So now we are going to acquire any asset whenever you are going to acquire, we use F-90 with vendor. So asset account return to vendor account. So what I will do is now we are in the month of October, I will acquire the asset in different dates so that you can identify the depreciation. Depending upon the number of days, system will calculate the depreciation. And the depreciation, already we have created the depreciation keys and so much of configuration has been done. So whether all those things are working for us or not, let us see. First, what I will do is I’ll acquire 1 asset. Say, for example 01/04/2013.

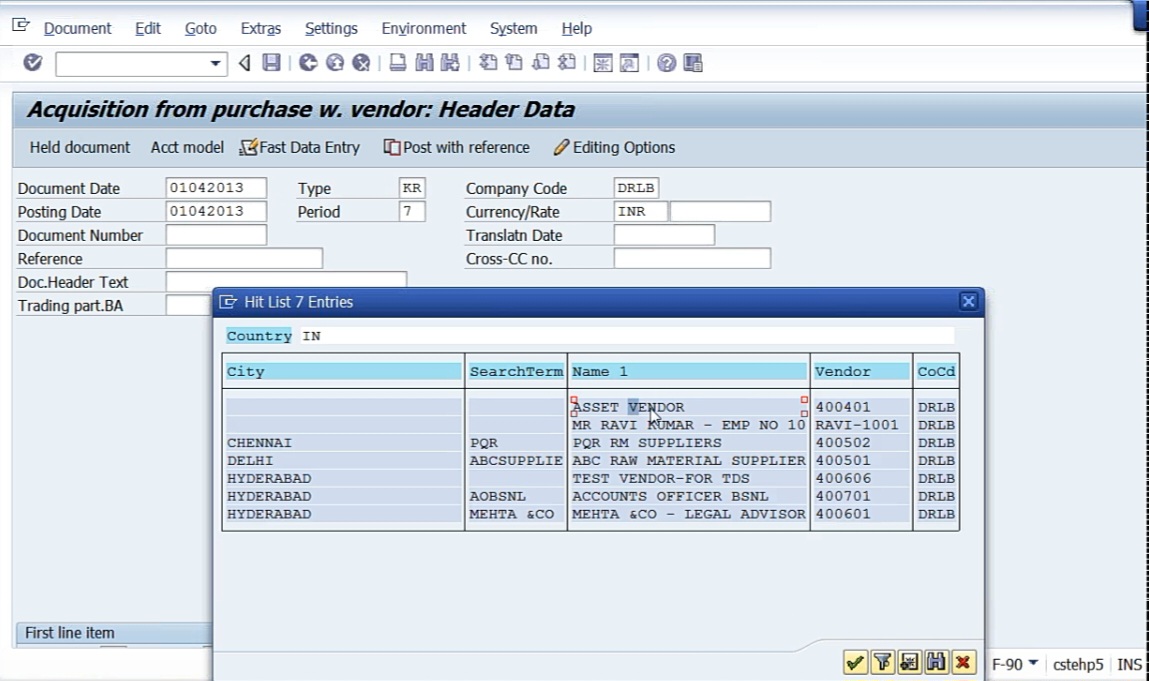

On 1st April, I’m acquiring 1 asset. On this date, I’m acquiring the asset. Asset vendor 400401. First message: Period 7 adjusted in line with posting date 01.04.2013. Go ahead.

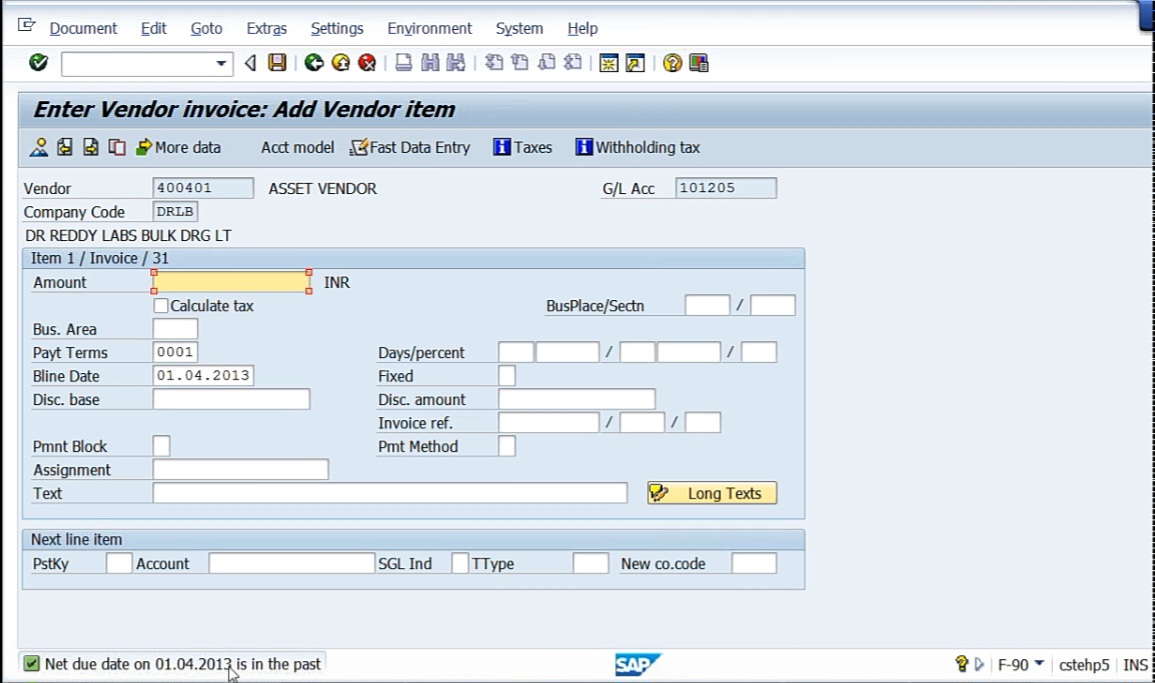

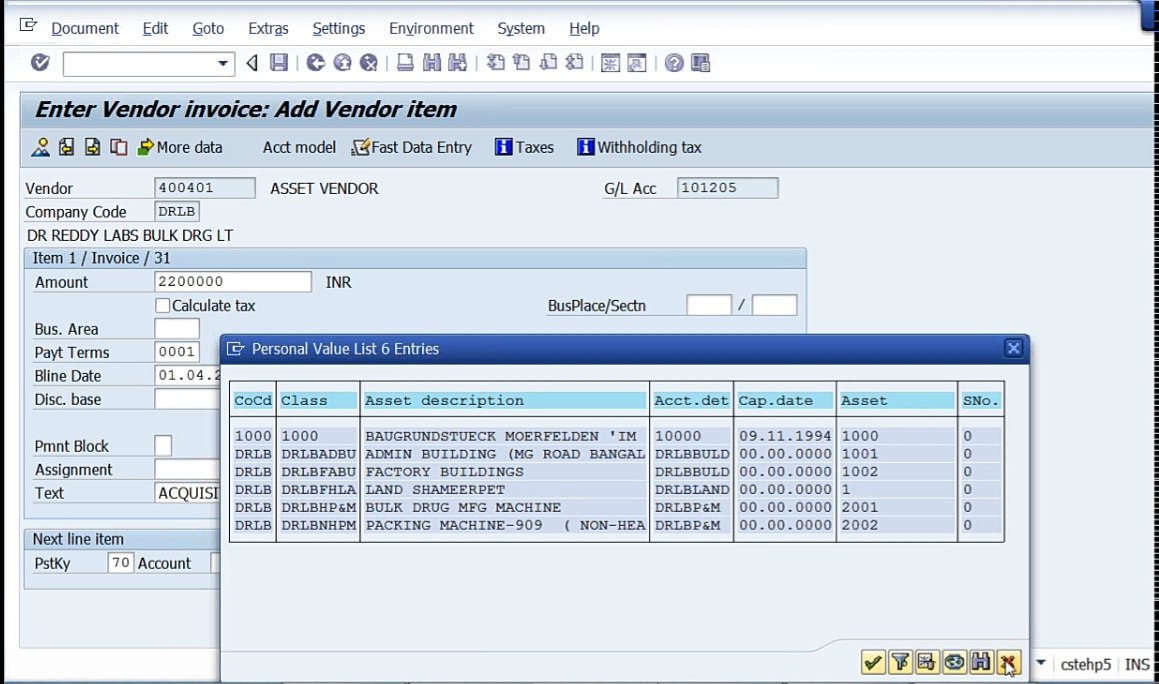

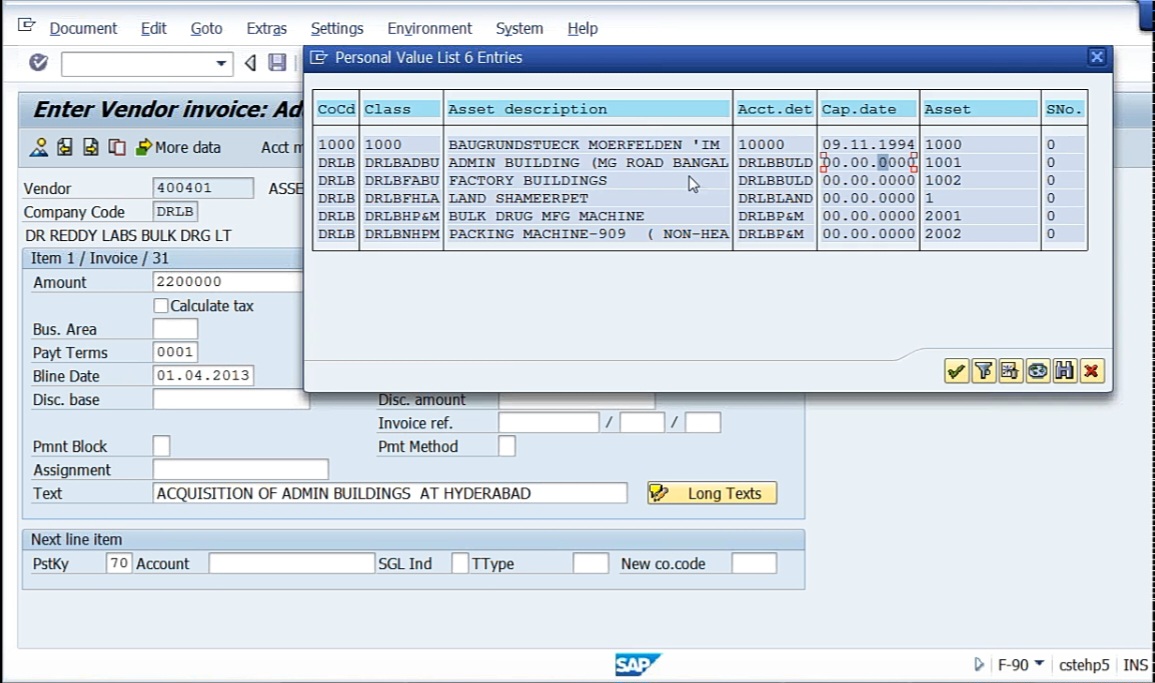

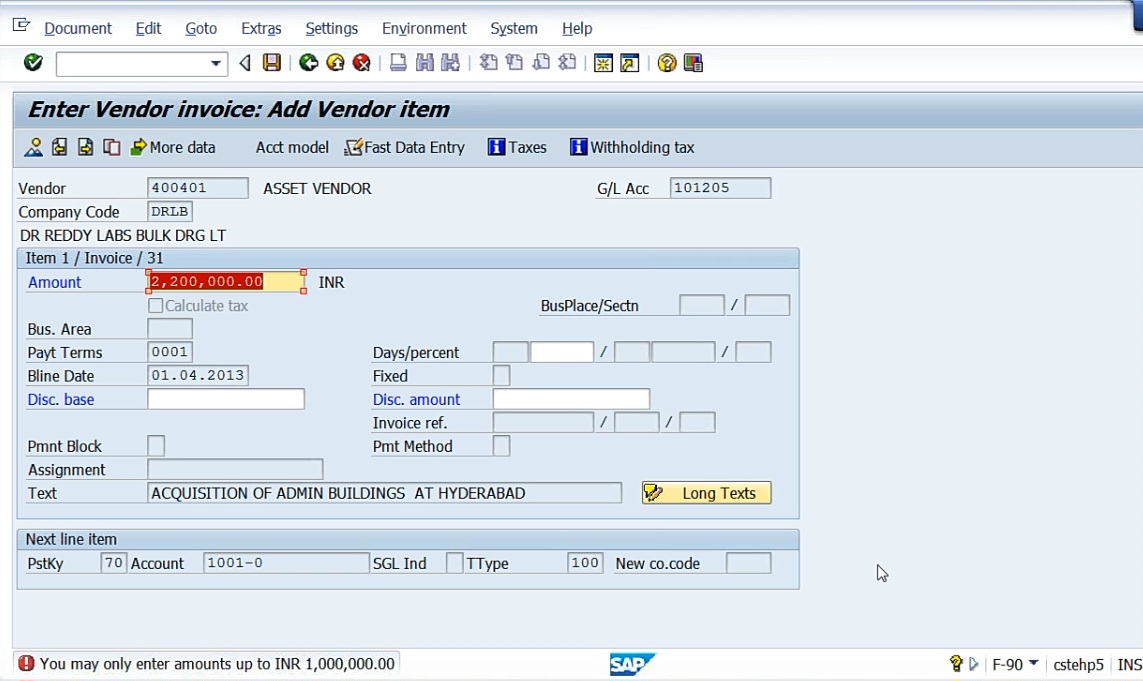

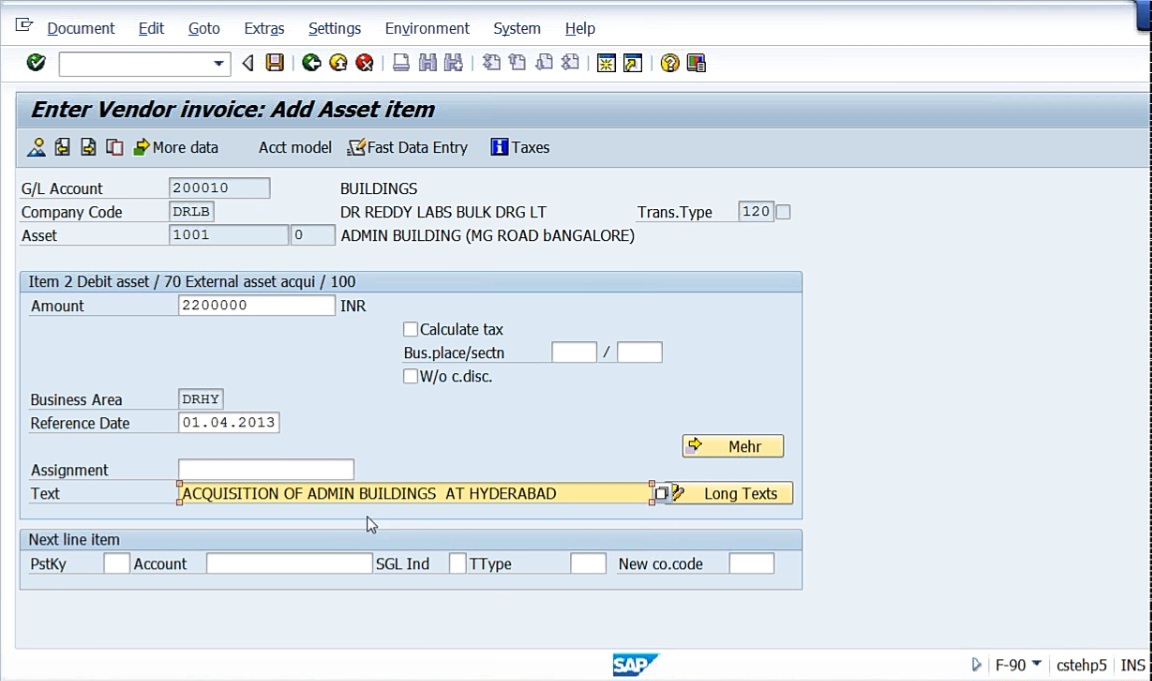

So net due date is in the past. So first of all, what is the asset that we acquire? Let me take, let’s say administrative building we acquire first. So administrative building, let us say around 22 lakhs.

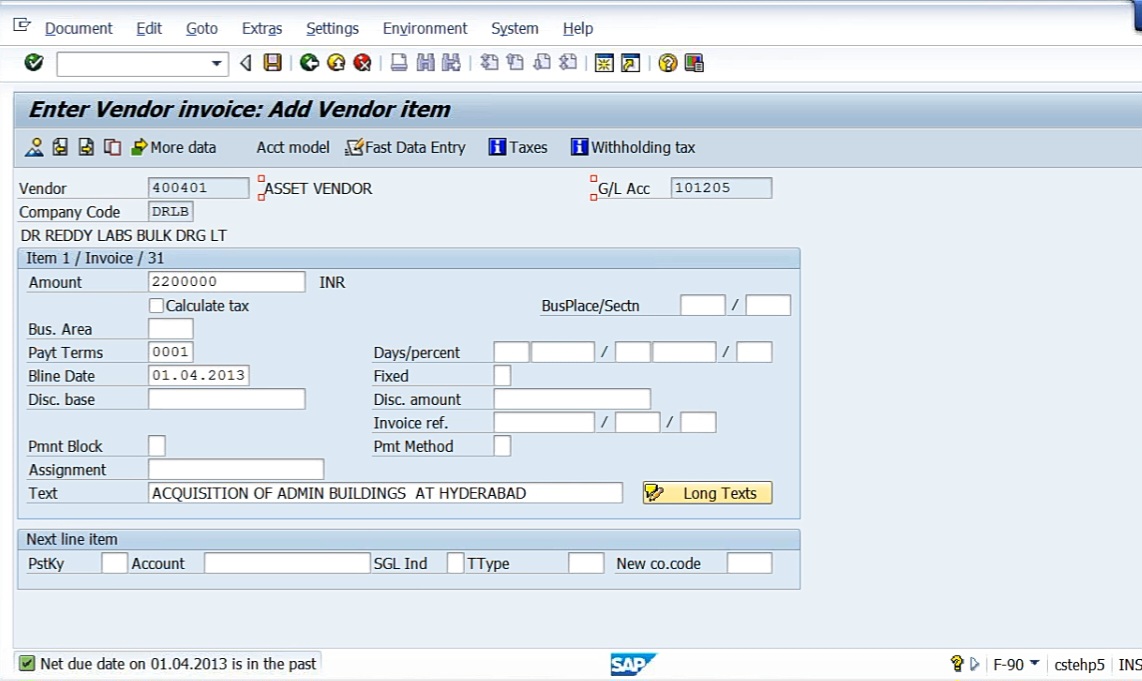

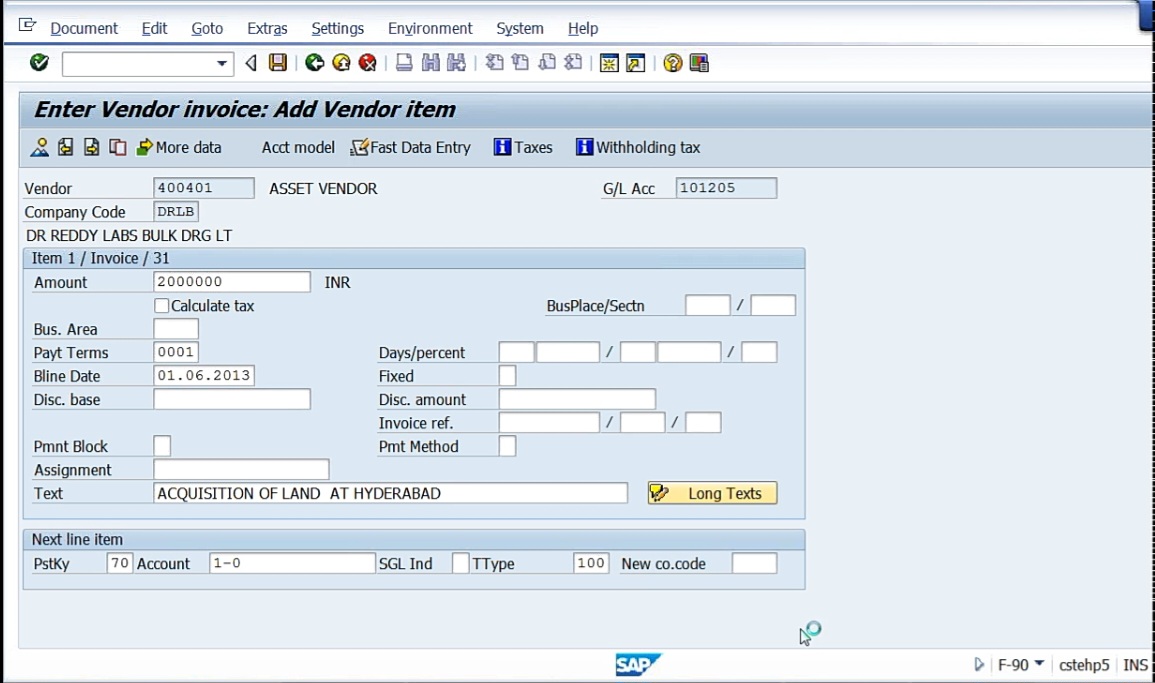

Acquisition of admin buildings at Hyderabad. So here, first vendor account is credited, then asset account is debited. And one more thing I told you on the day we have discussed about the posting key. Asset debit is 70, Asset credit is 75. GL debit 40, GL credit 50. Customer debit 01 Customer credit 15. Vendor debit 25, Vendor credit 31. So for asset debit asset credit, we are using 70, 75, Asset debit is 70, Asset credit is 75. I told you that in case of general accounting, what we do, we use only debit and credit. But here in SAP, debit and credit is not sufficient. It will be associated with this number, 70, 75, 40, 50, 45, 31, like that. Because, as soon as you take 70, let us see what happens here. Here, if I take 70 see here, assets are visible.

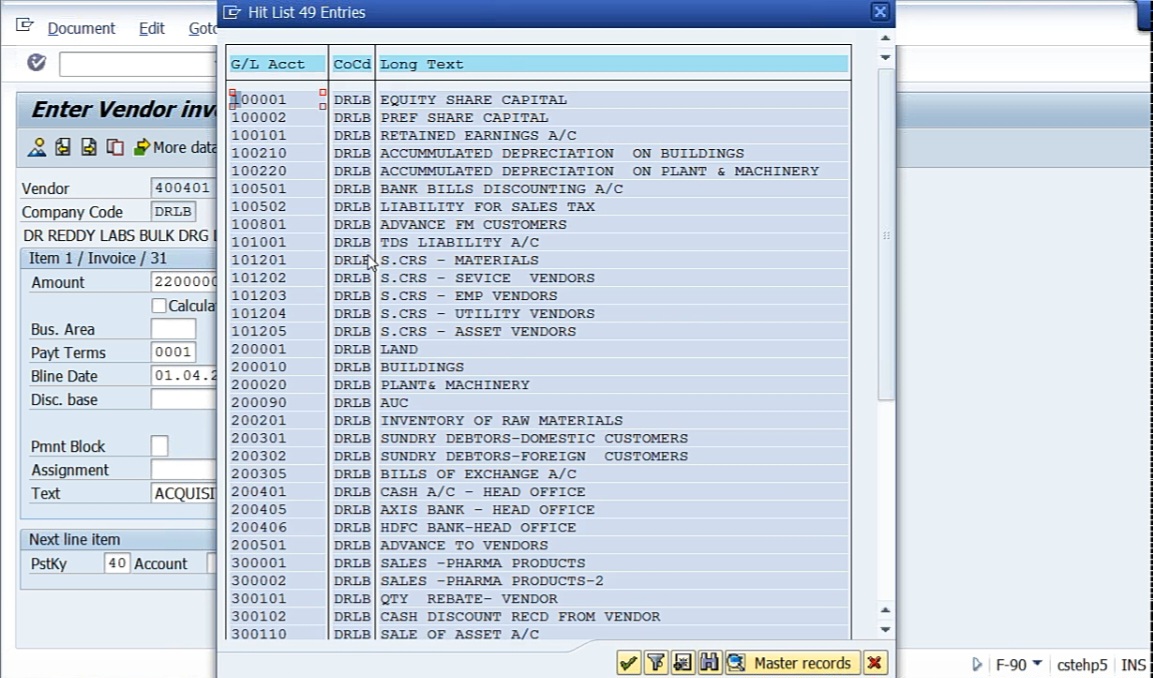

Instead, if I take 40, GL accounts are visible here.

If I take customer debit 1, we can see list of customers. So like that Vendors also. So here for the purpose of acquisition of asset, take 70. So debit what comes in, Asset debit, vendor account credit. So whenever you are going to acquire anything, first line item by default system takes vendor and that vendor account is credited. Then first line item is credit means, second line item is debit. Now let us acquire the asset, Admin building.

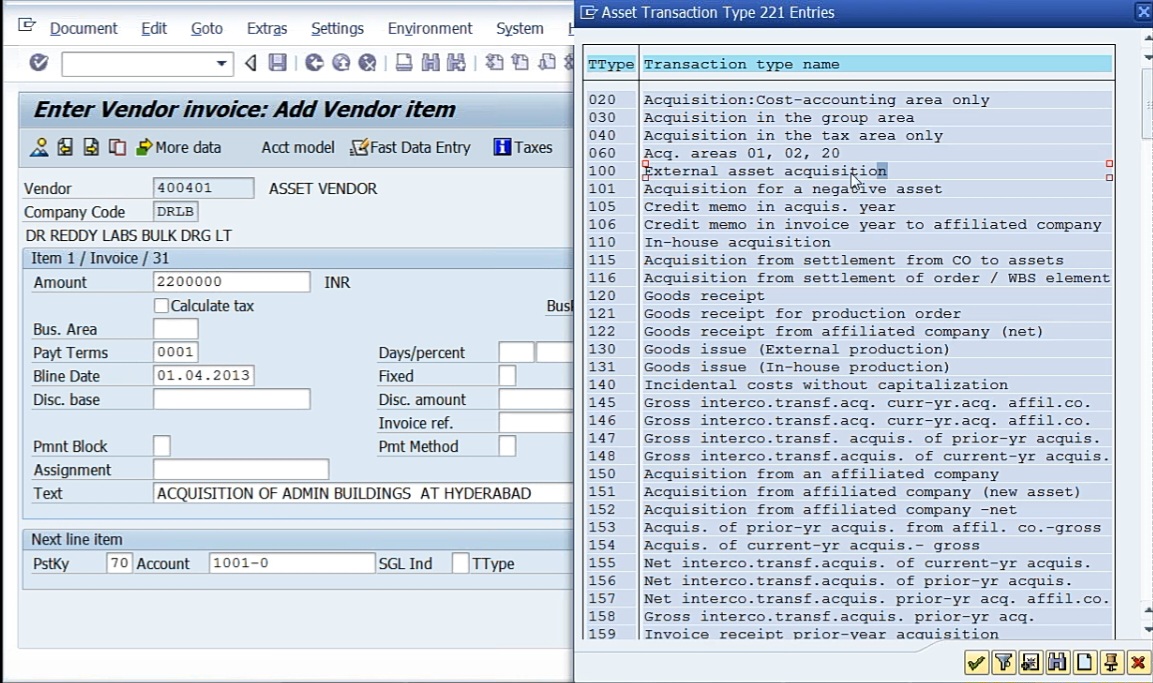

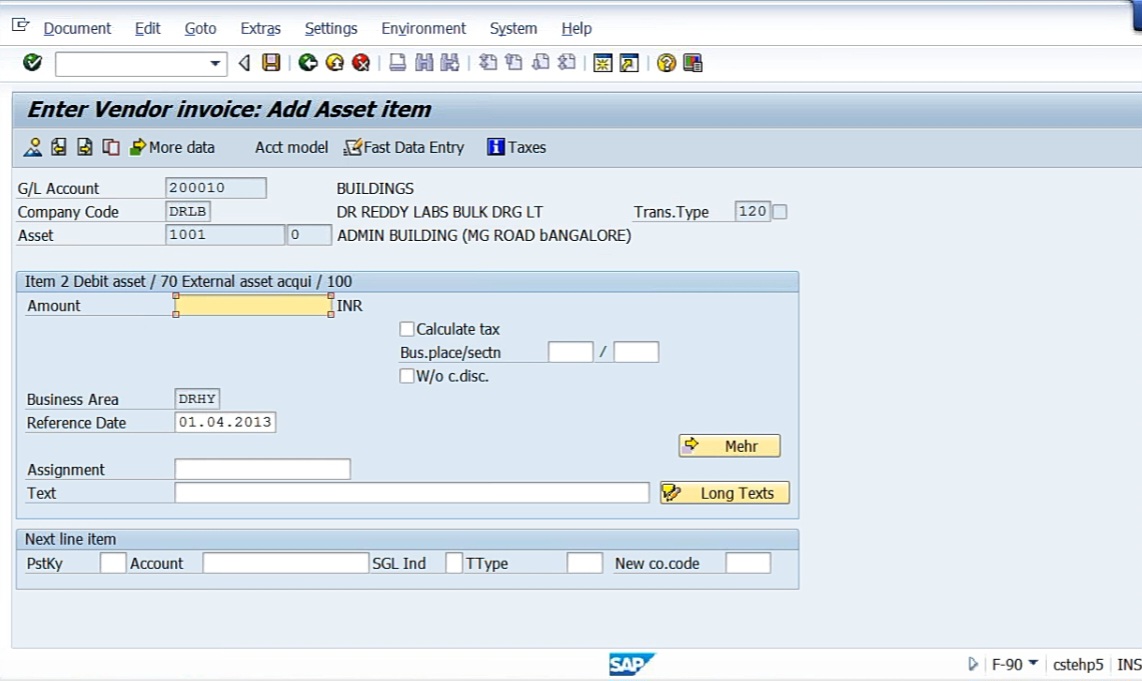

Now it is showing as 0. As soon as we acquire, then it’ll be the date of depreciation and date of assets will be changed. Now a new thing is transaction type. Here, we need to take transaction type also. Whenever we are going to associate it with asset accounting so when acquiring the asset, take 100 external asset acquisition.

So we have to take external asset acquisition. Without this, you cannot post entry. Press enter.

Message: You may only enter up to 10 lakhs.

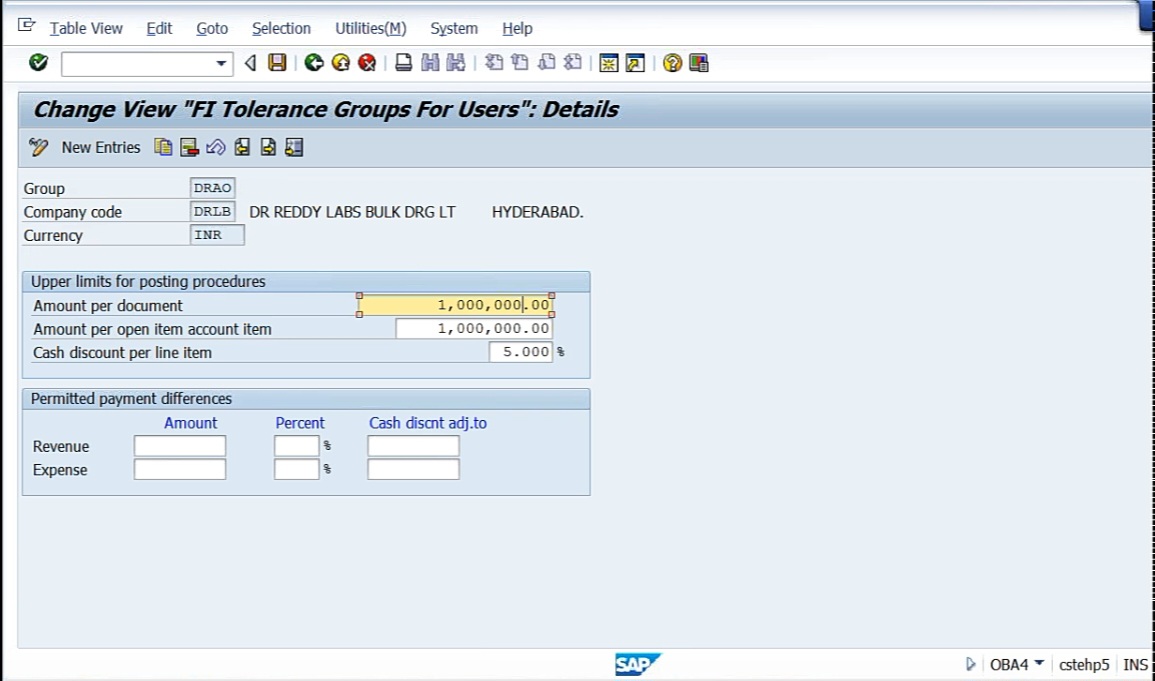

How to rectify this is in Tolerance group. The T code is OBA4.

See here, 10 lakhs. Let me make it 99,999,999 and try again.

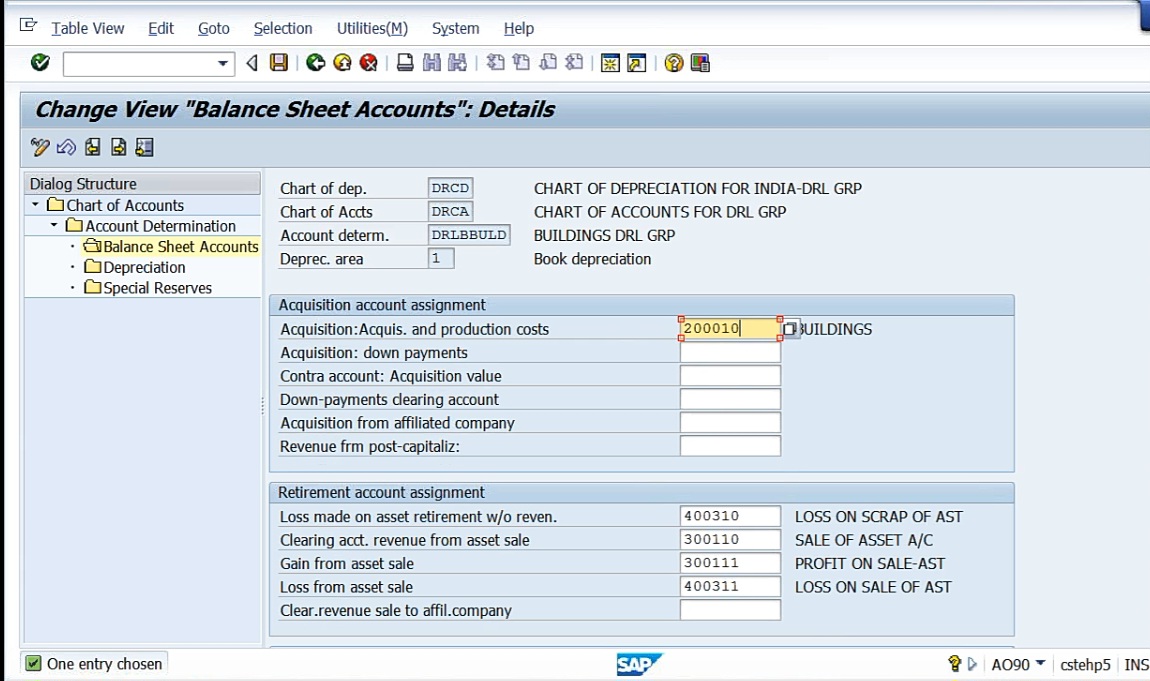

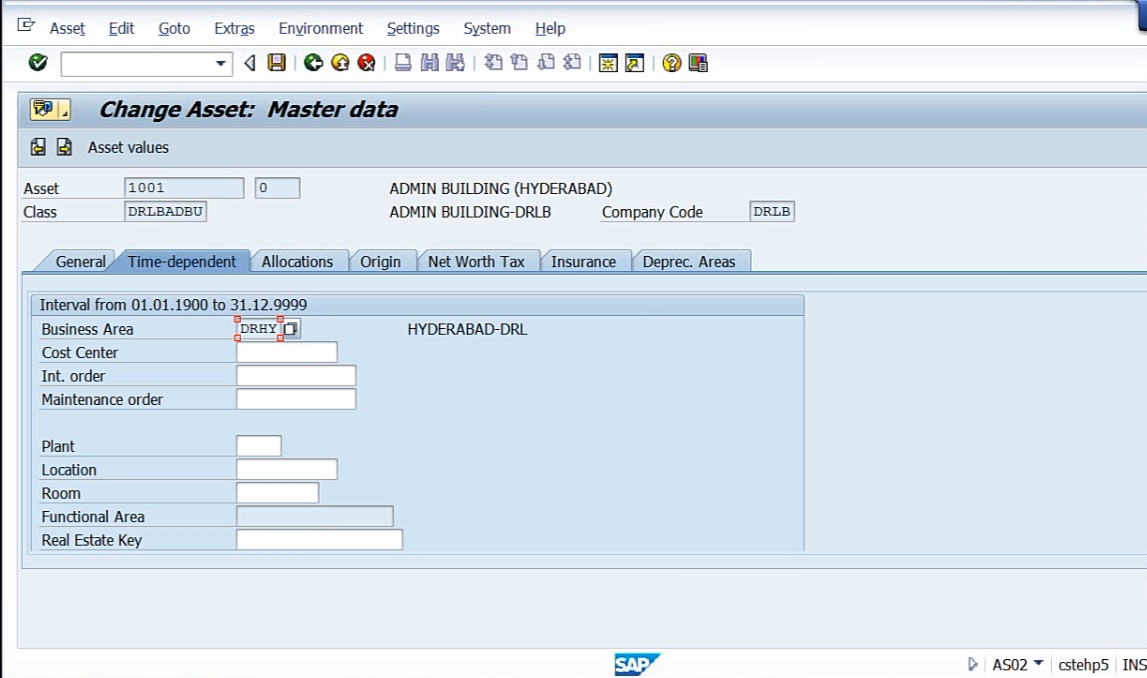

And business area, DRHY. It is grayed out, how come? Because we have already created this asset master 1001 admin building, location we have given as Hyderabad. So that’s why you cannot change now. By default, whatever the master record we have mentioned there, the same thing will be taken up by system here. And one more thing, I have taken only 1,001, I did not take GL account 2 lakh 10. How come system has taken? So we have given only 1,001 but system has picked up these buildings. How come? Because here we have already given in Integration with General Ledger Accounting. Here we have already made assignment under Assign the GL Accounts. See here all the GL accounts have been assigned at account determination level and balance sheet accounts.

Here we have given all the GL account here. So because of this we got the same account by default. And where Asset 1001 and GL account 200010, these 2 are already linked in is AS02. AS01 is creation of asset master record, AS02 is change, AS03 is display. But since we are already working here, it cannot show us. Let me complete it then we can see.

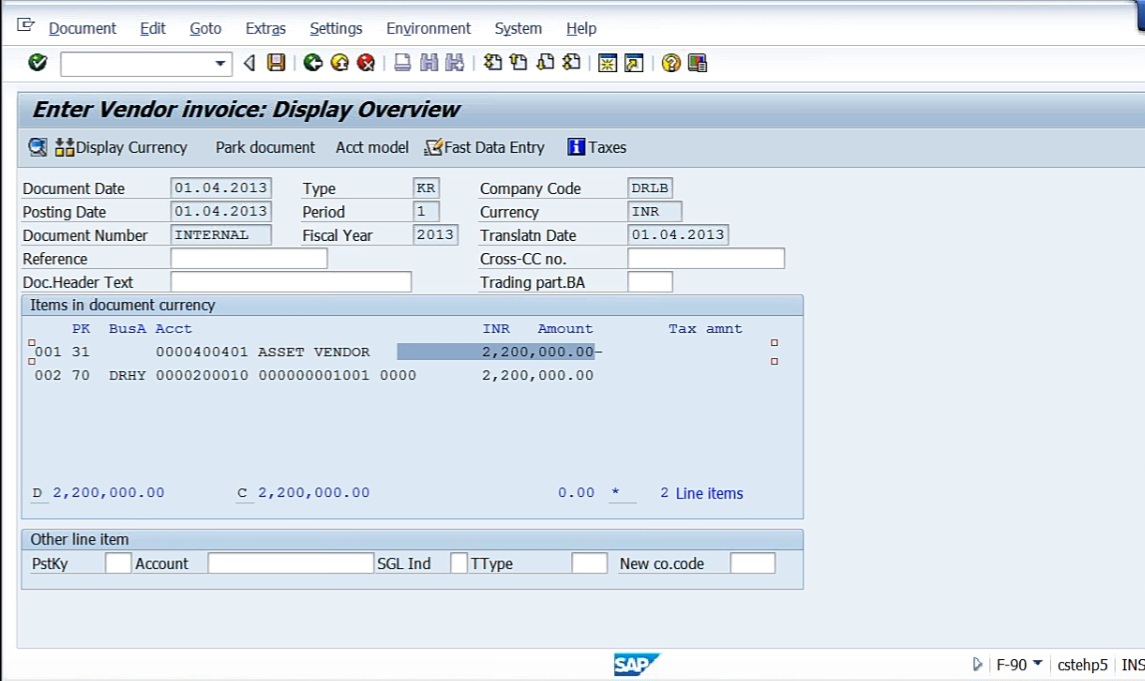

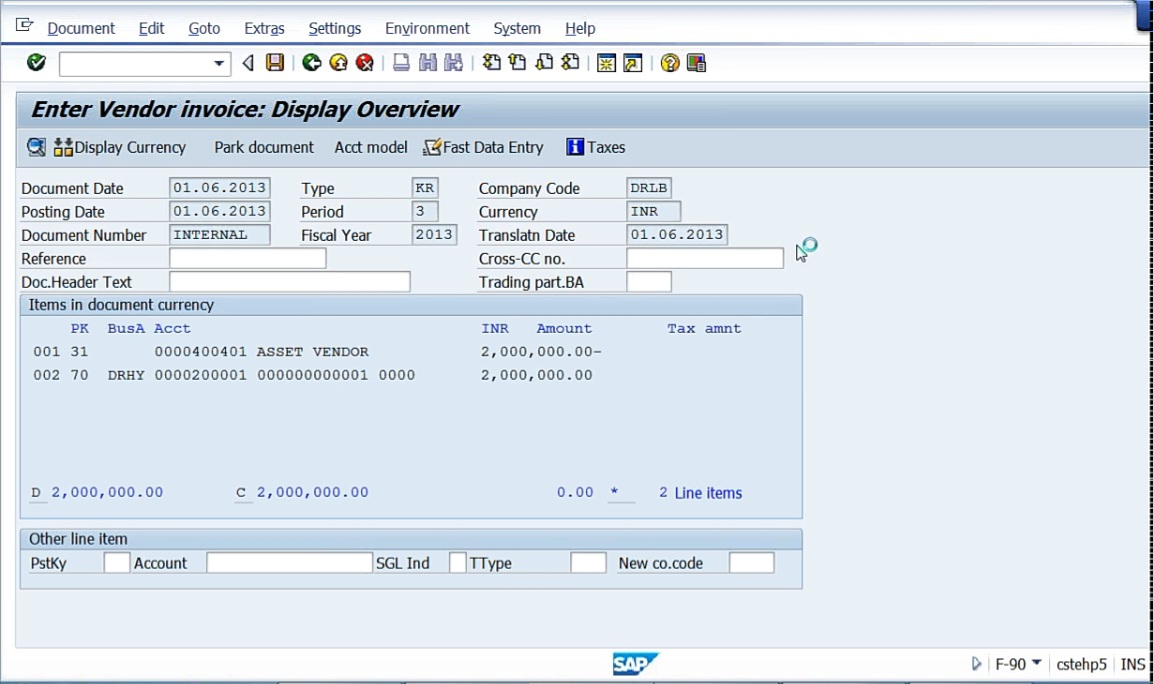

So acquisition of admin buildings at Hyderabad. Click overview.

So asset vendor account is credited and asset account is debited. So debit the asset, create the vendor. Now, just save it. Meanwhile, so in Accounting, Financial Accounting, Fixed Assets, Asset, Change.

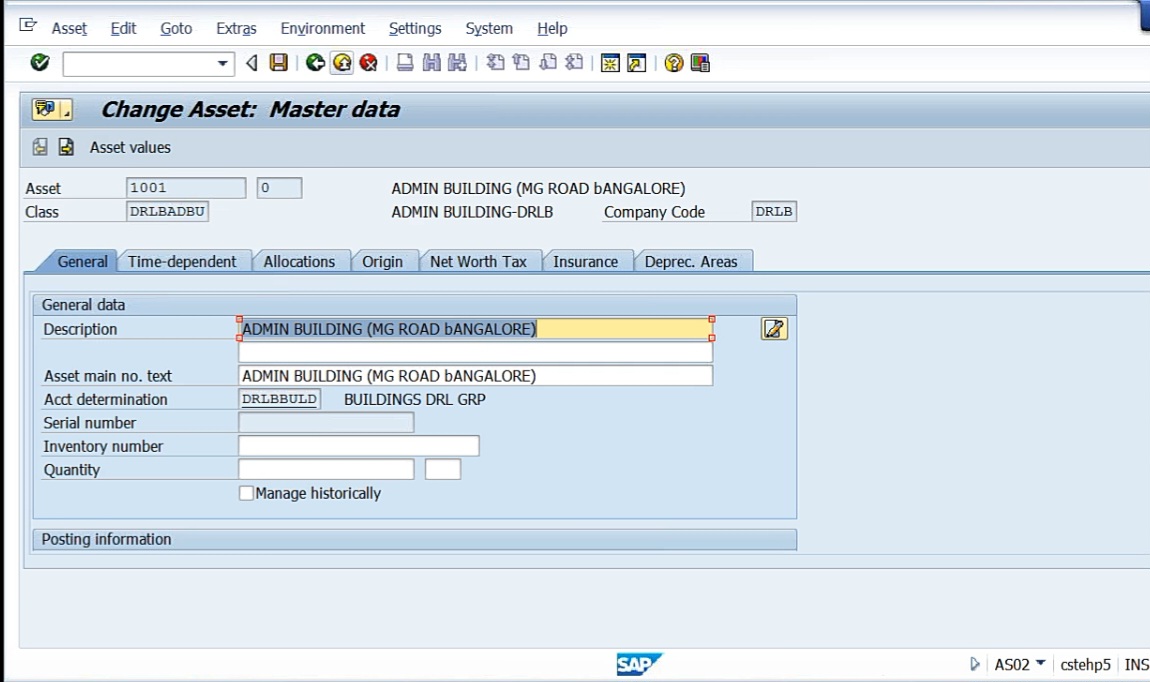

Here, Admin building. So whenever we have created, DRLBADBU is asset class, 1001 is asset master record. And see here DRLBBUILD is account determination. So this account determination, asset class, and asset master record are linked with each other. Now one more thing, we have acquired the asset on 01.04.

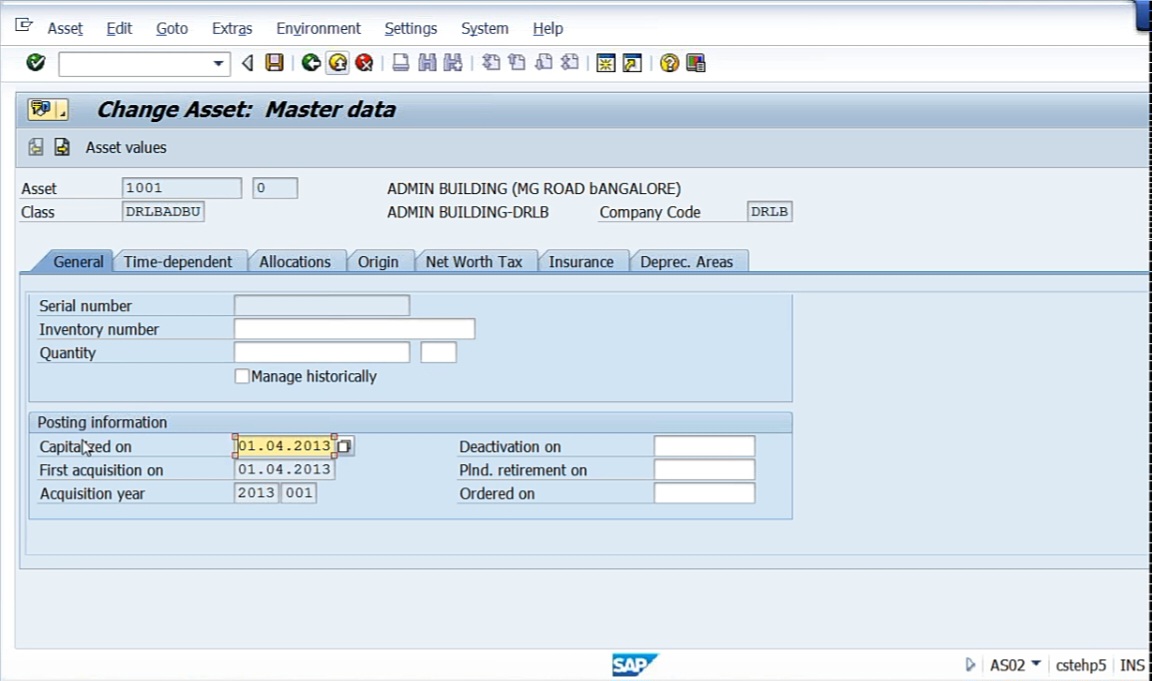

See ‘capitalized on’ 01.04.2013. We have not given at the time of creation of asset master. Capitalization has been done on 01.04, and the first acquisition, 01.04. Year is 2013.

And in time dependent tab, we have given DRHY as business area. That’s why by default, whenever we are going to acquire an asset, you cannot change the business area.

See, it was blank when we have created the asset master. Now by default, depreciation start date system has taken as 01.04.2013 because the date of acquisition is that. From the date of acquisition onwards, system starts providing the depreciation.

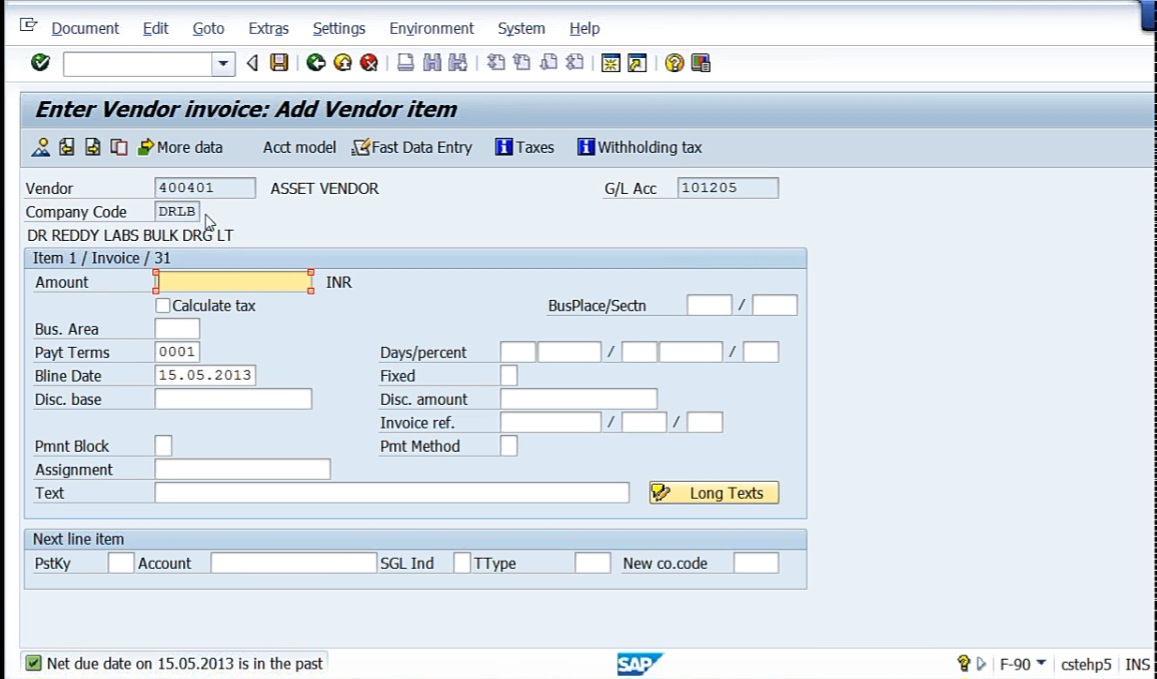

Let me create one more asset. We have taken admin building, let me take heavy plant and machinery, I’ll take from 15.05.2013, i.e 15th of May I’m taking. Type is KR, vendor invoice. First line item account is 400401. Press Enter.

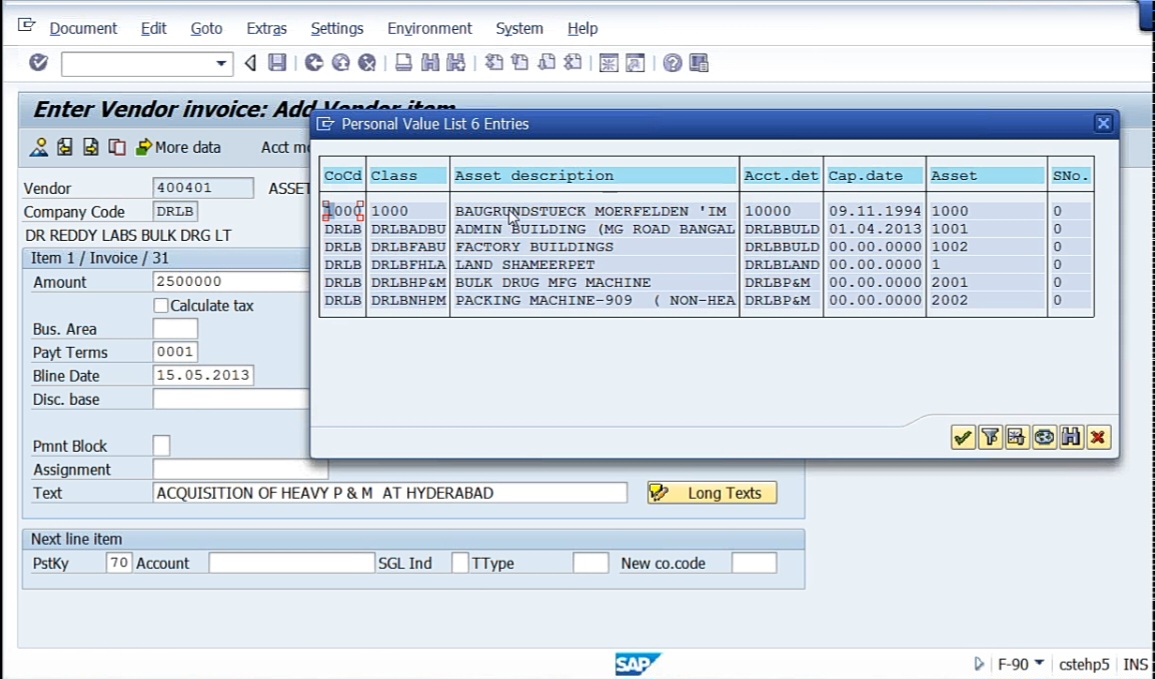

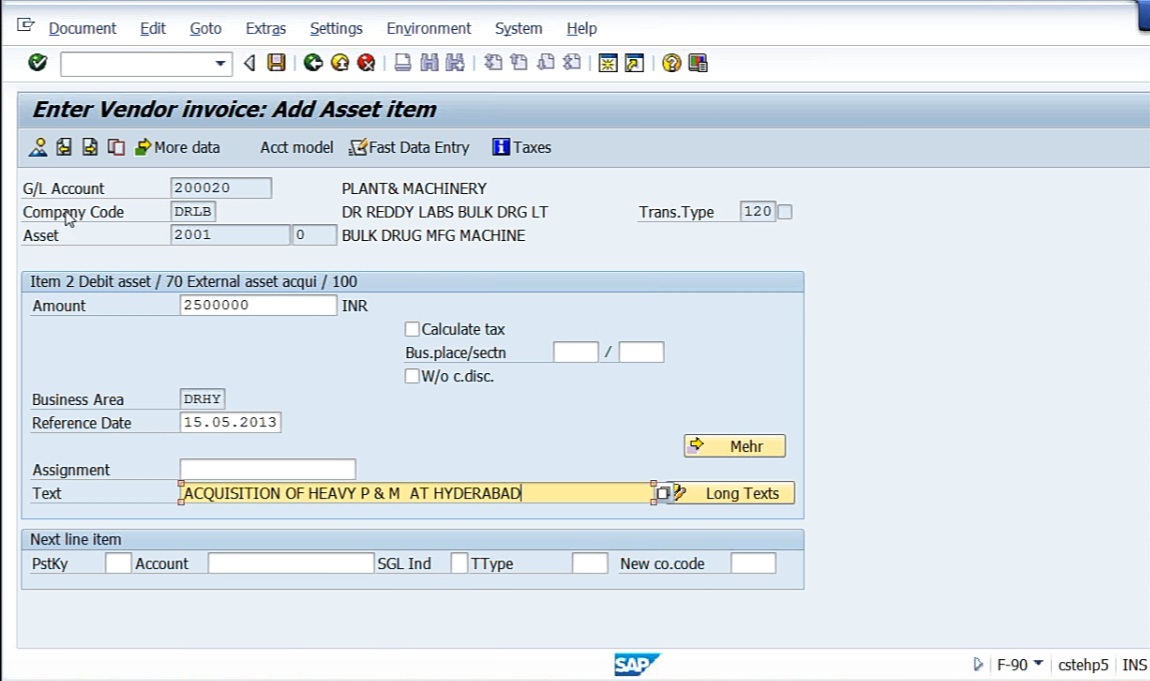

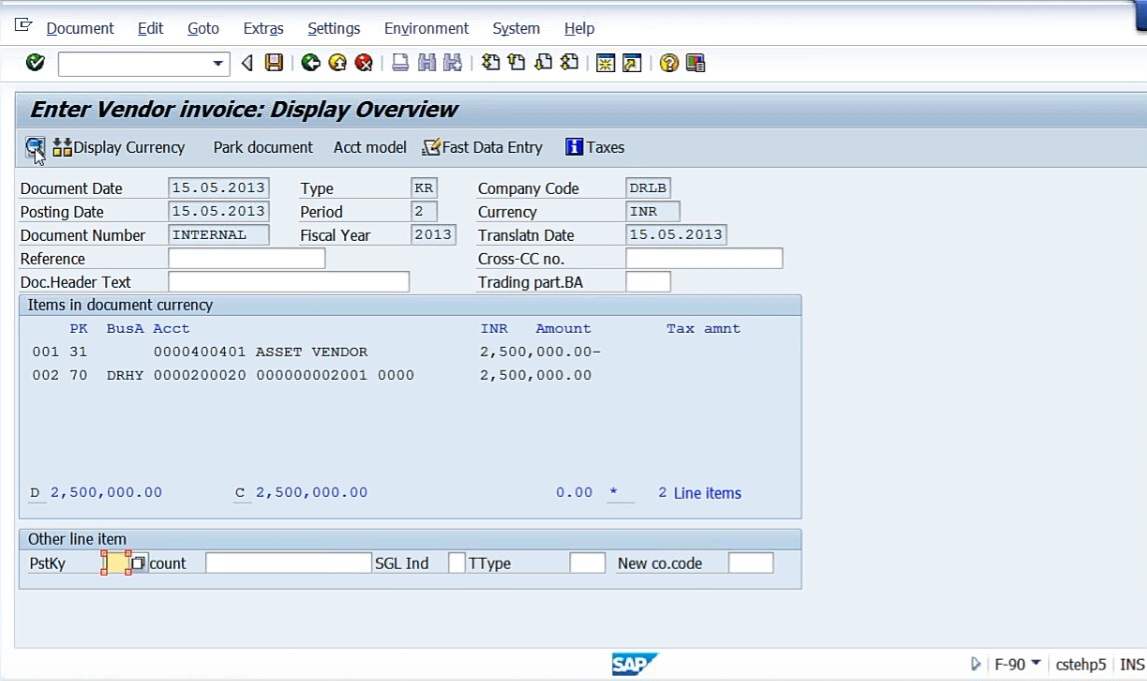

So, Asset vendo 400401. Say heavy plant and machinery. Say, amount 25 lakhs I’m taking. Text, acquisition of Heavy Plant and Machinery. Here again, 70 asset debit and here for account you have to pick up the master record.

So without creation of the master record first, you cannot acquire an asset. See bulk drug manufacturing machine means very heavy machine, take this, 2001-0, Transaction type 100.

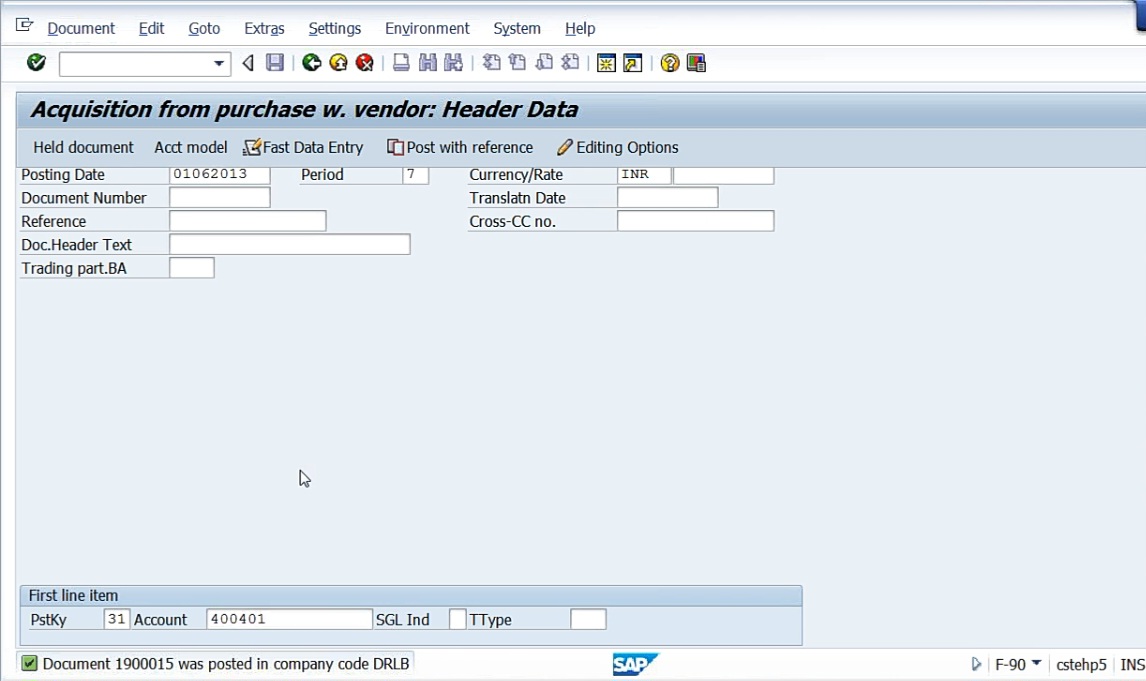

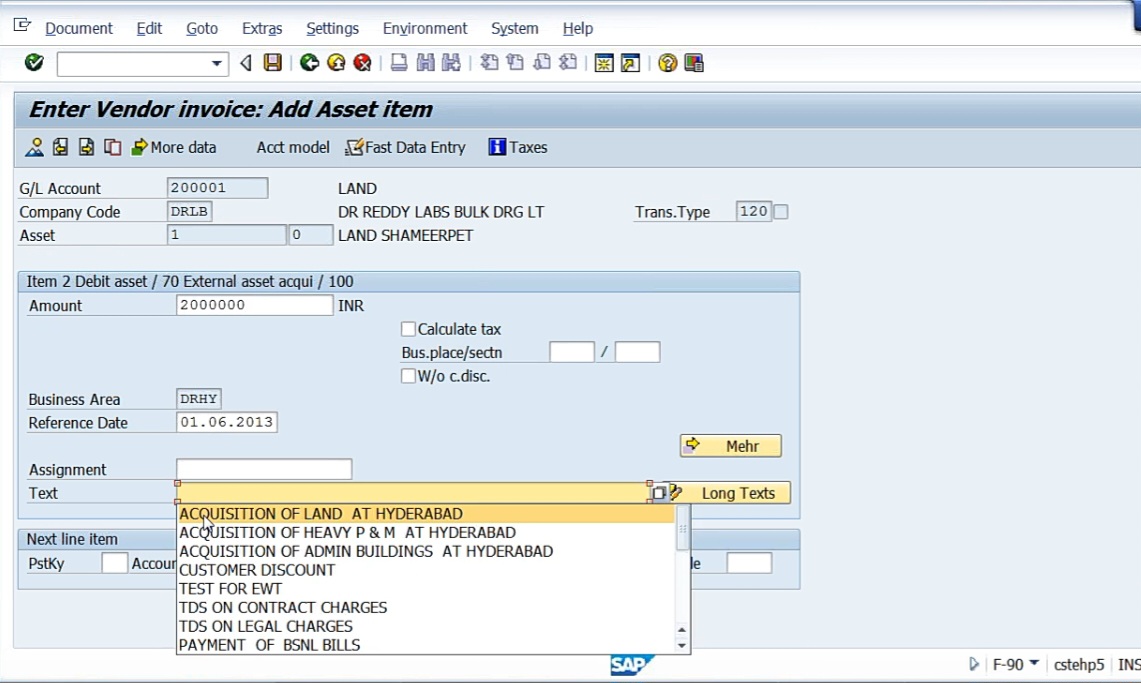

So both the assets we have created. Now let me create one more asset on 01.06.2013. I’ll acquire land, say piece of land.

So here there is no depreciation on land.

Okay. See here,

for admin building 01.04, land 01.06, bulk drug manufacturing machine 15.05. So whenever we have acquired an asset, system will show you the depreciation here. The date of acquisition, of course, and date of acquisition, capitalization date will be in the ‘Change Asset: Master Data window’. And not only that, if you go to the Origin tab there, it’ll show you from which vendor we have purchased this asset. So date of acquisition is nothing but now the date of depreciation start date. So by default, system takes all these things.

Now I want to show you one important thing, that is nothing but asset explorer. Asset explorer contains a lot of information about the asset. So Accounting, Financial Accounting, Fixed Assets, Asset, AW01N Asset Explorer.

So what is meant by asset explorer? It will contain 4 main tabs.

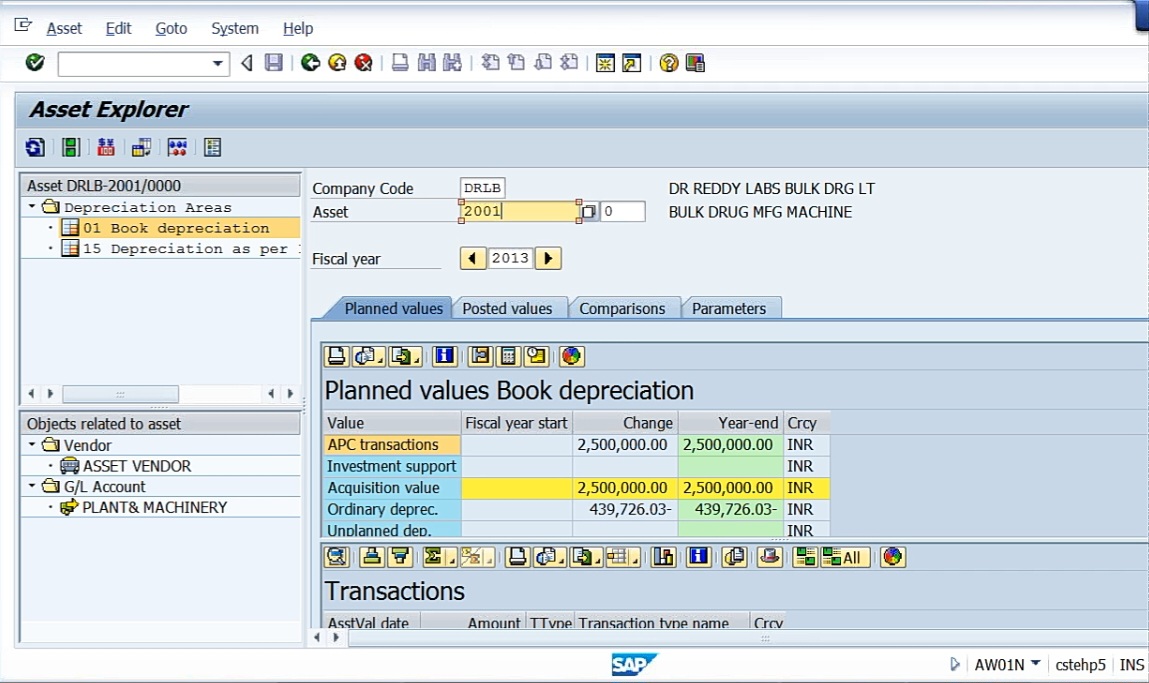

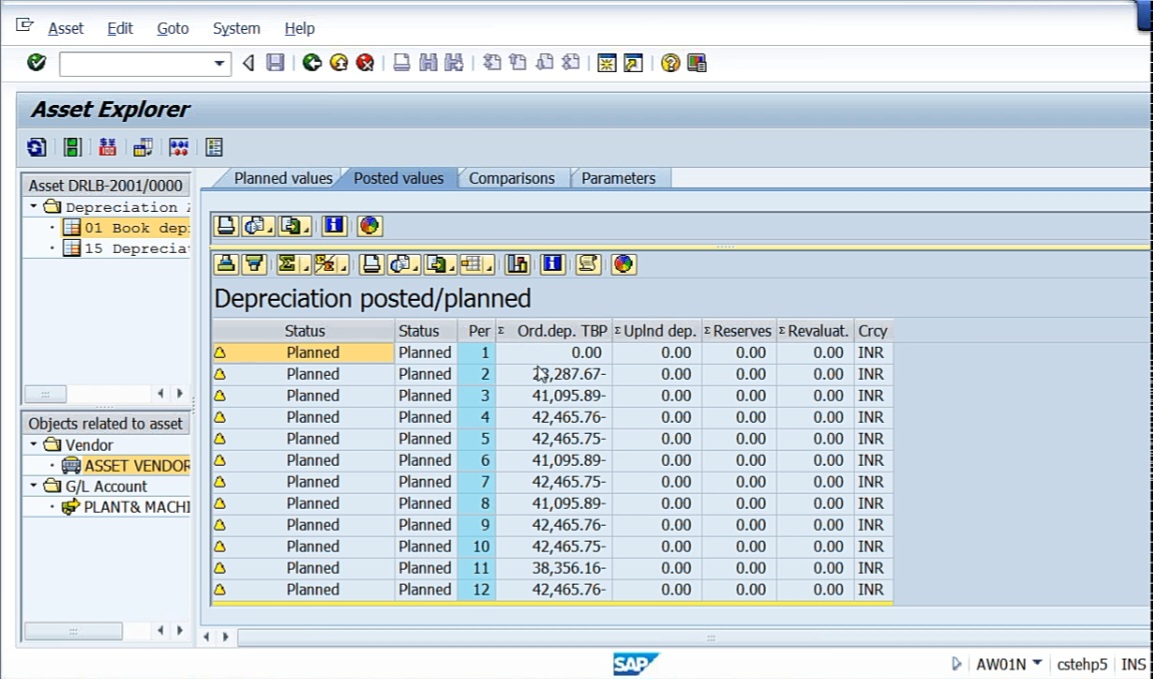

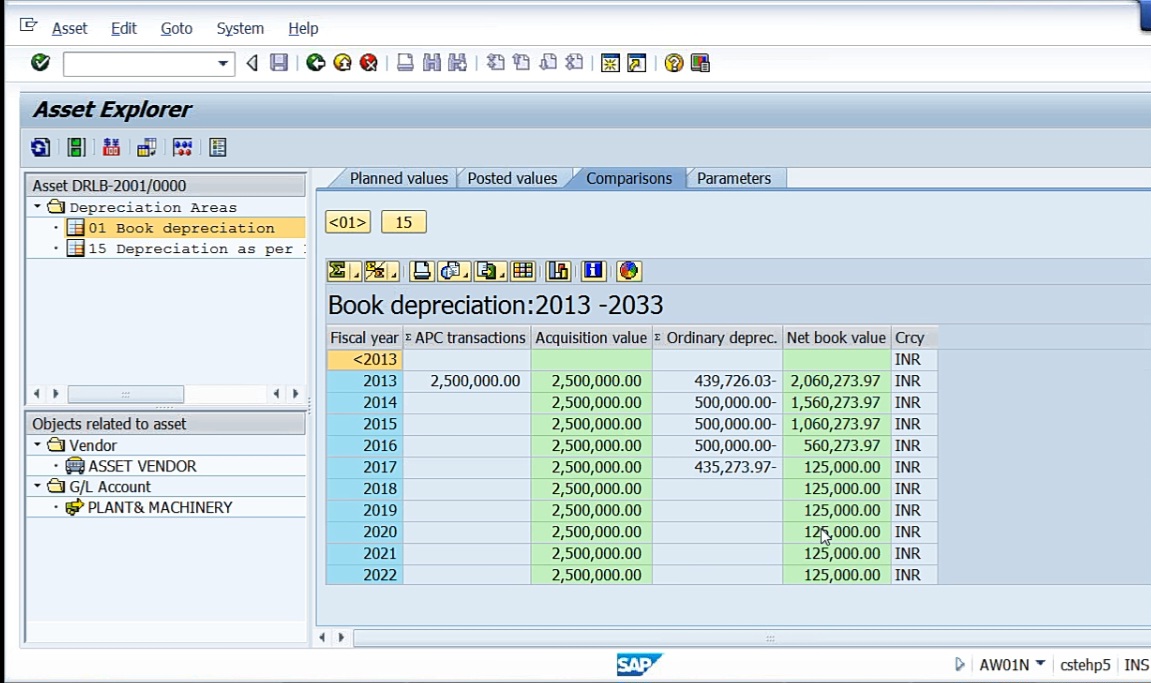

See, asset 2001. Here, this is book depreciation, objects related to the asset from whom you have purchased and to which account this has been posted, plant and machinery account. So here’s a vendor, asset vendor 2001 bulk drug manufacturing machine. It has got 4 major tabs. First tab is brand values, there’s posted values, comparisons, and parameters. Fiscal year is 2013. Asset is 2001. And the first one is planned values. Planned values are nothing but asset procurement, cost 25 lakhs and acquisition value, 25 lakhs. This is ordinary depreciation from 15.05 onwards, depreciation per annum. 4 lakh 39,726.03 is the year-end value, and here system shows after the end of the first year, 20 lakh 60,273 is the net book value. All these are all planned values. Though we have not provided depreciation, system is showing you, yes, in case as for the depreciation rate that you have given from 15th May to 31st March. This is going to be the depreciation. So planned values show everything.

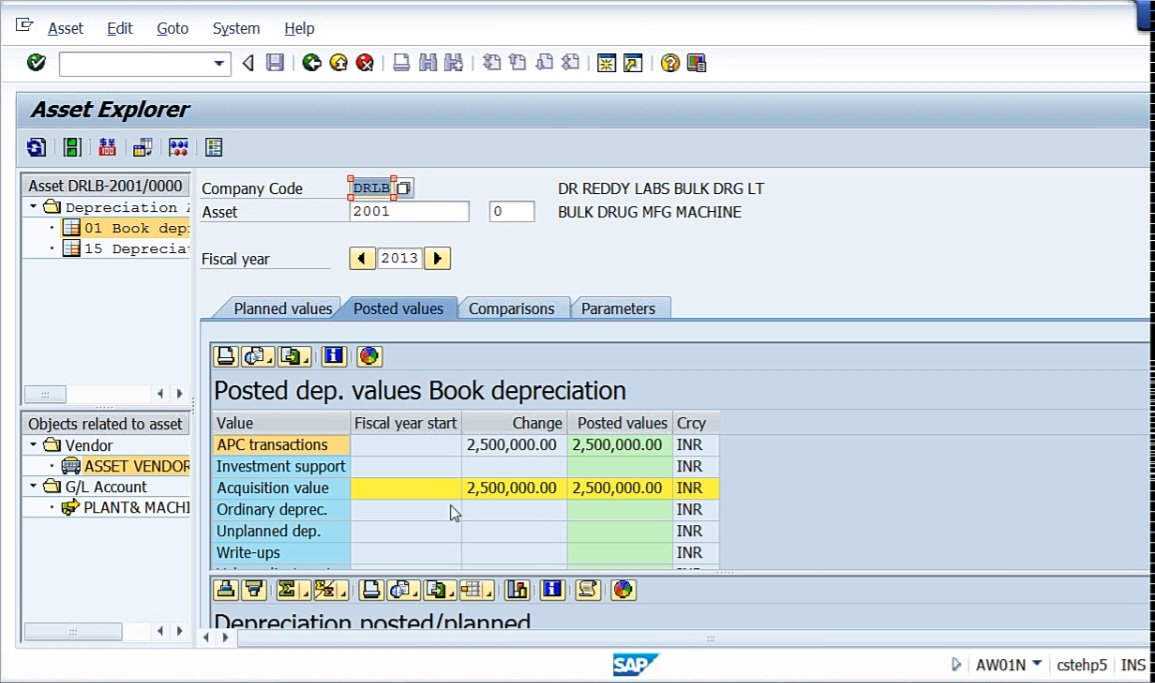

Next posted values.

Here, since we have not yet posted any depreciation, system is not showing any depreciation here. So the book value also as on today only 25 lakhs.

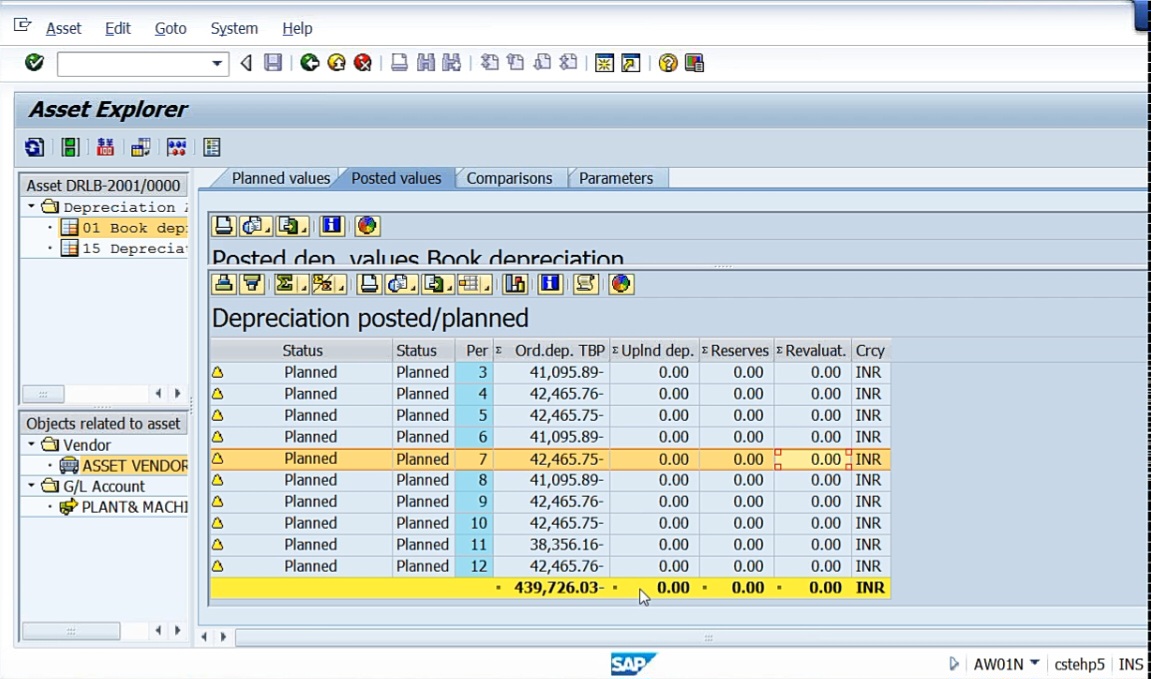

When coming to the depreciation posted/ planned. See, planned depreciation because in the first month, we do not have this asset because we have acquired on 15th of May. So that’s why month of April, no depreciation. May, 15 or 16 days depreciation. And afterwards, 41,095.89, depending upon the number of days, it’ll calculate. 30 days or 31 days, whatever it may be. At period 11 it will be less because of February. February month, the number of days are 28, or 29 if it’s a leap year. The total 4 lakh 39726.03.

So there, the planned values are seen. Here, monthly bifurcation of the depreciation is seen here. But this is planned values, planned values in the sense, the planned depreciation we have not yet posted. Once we post the symbol will become a green symbol then it will post right.

Then comparisons tab,

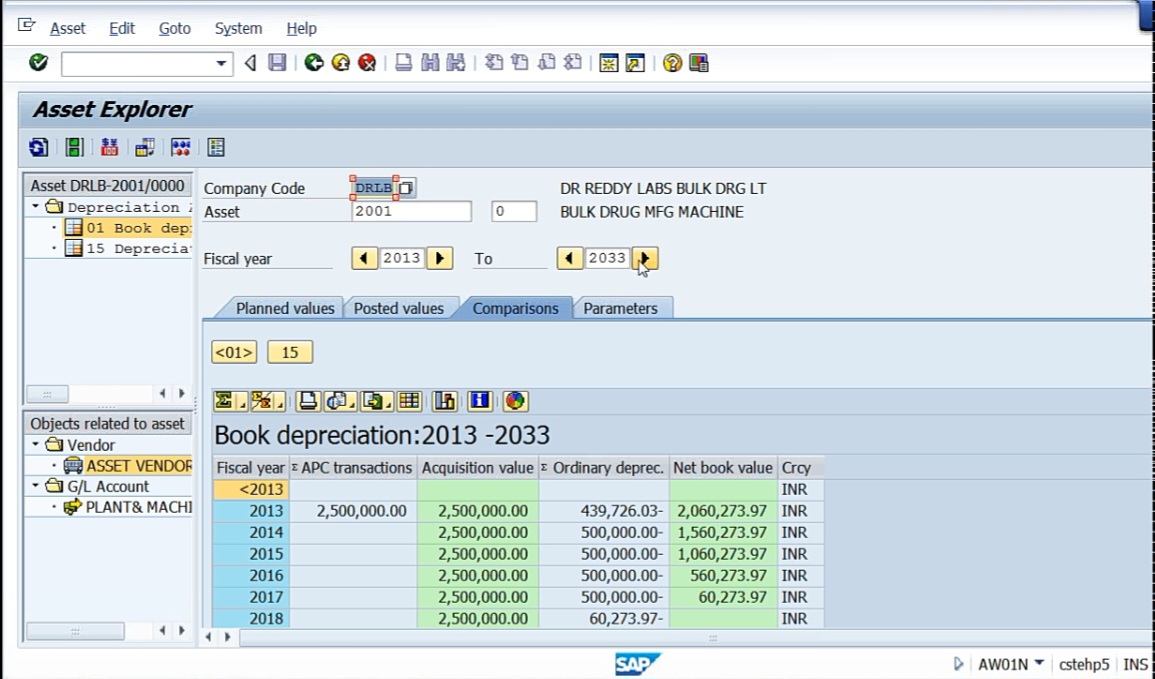

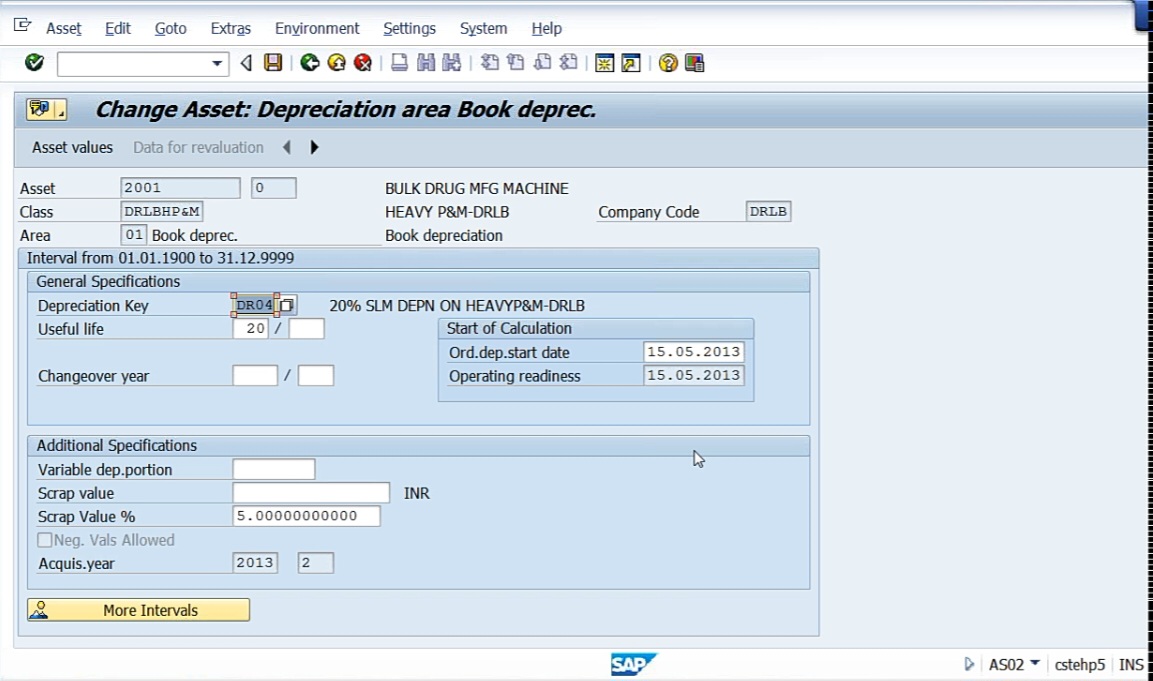

See here comparisons we have given 20 years for heavy machinery. That’s why the system has taken for 2013 to 2033 years. Here the depreciation rate of depreciation we have taken is, I think, 20% or something. So according to the 20%, system calculates, for the month of April we have not taken the asset, so May 15th onwards. So that’s why the first year amount of depreciation is reduced here. And next year the full depreciation, then less again in the last year. So here, the life of the asset is 20 years we plan, and the depreciation is only 20%. So that’s why within 5 years, the asset will get exhausted, the value will become 0. But what we can do here, though here value is 0, I can maintain some scrap value of the asset. Say, heavy plant and machinery, after 5 years, if it is fully used for 3 shifts a day, what is the value of the asset? But what we can do, we can maintain some residual value of the asset because we cannot take it as complete 0 because, physically, the asset is going to be there. Though depreciation has been exhausted within 5 years, asset value cannot become 0 just like that. So that’s why what we do, whatever the asset that is appearing, I can maintain maybe 10% or 5%, whatever the value we want, we can maintain as residual value of the asset here. I’ll show you how to enter that.

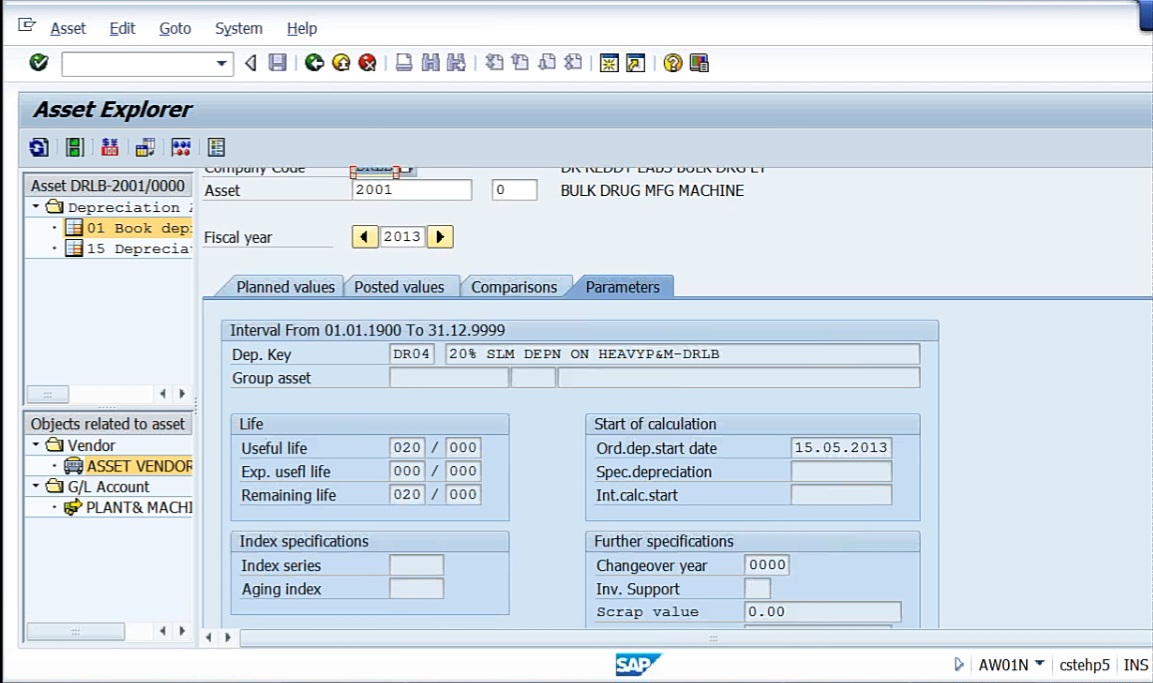

This is the fourth tab, parameters. That is, the parameters are visible completely here. The depreciation, rate of depreciation, everything.

These are the parameters. What parameters? 20% straight line depreciation on heavy plant and machinery DRLB. Useful life, 20 years. Remaining life, 20 years. Scrap value, we have not given anything, so that’s why it’s showing 0 value. But we’ll change it now. Display of depreciation key. So here’s the depreciation key we have taken, 0014 DR4.

And, remember, it’s a multilevel method key we have created. So base value, 01 acquisition value that is. So like this, in asset explorer, you can find a lot of information about the asset.

Now this what I want you to do: create an asset master record, acquire the asset, go to the asset explorer and explore everything. Each and every tab, you explore it. So this is asset explorer. What I I want to tell you now, so these comparisons, I want to put some scrap value here or the residual value of the asset after the end of the 5th year, and we can continue to do like that. So system will not calculate any depreciation on that because there’s a straight line depreciation.

Go to change mode, AS02, 2001 asset. Go to depreciation areas. Double click on book depreciation.

Scrap value, either value I can give directly or percentage I can give here. So scrap value percentage, what I do is, 5% of the asset value, I want to maintain as the residual value of the asset after the end of the planned number of years. Save it.

And what we can do from asset master record itself, I can go to AW01N.

See comparisons. See 125 because asset value is 25 lakhs. On 25 lakhs, 20% depreciation. In the comparisons, you can see here after 5 years, the residual value of the asset is 1 lakh 25,000. We can continue this until the life of the asset.

So this is about asset explorer. And if you want to see 1,001, type it in the asset field and press enter. The values will get changed.

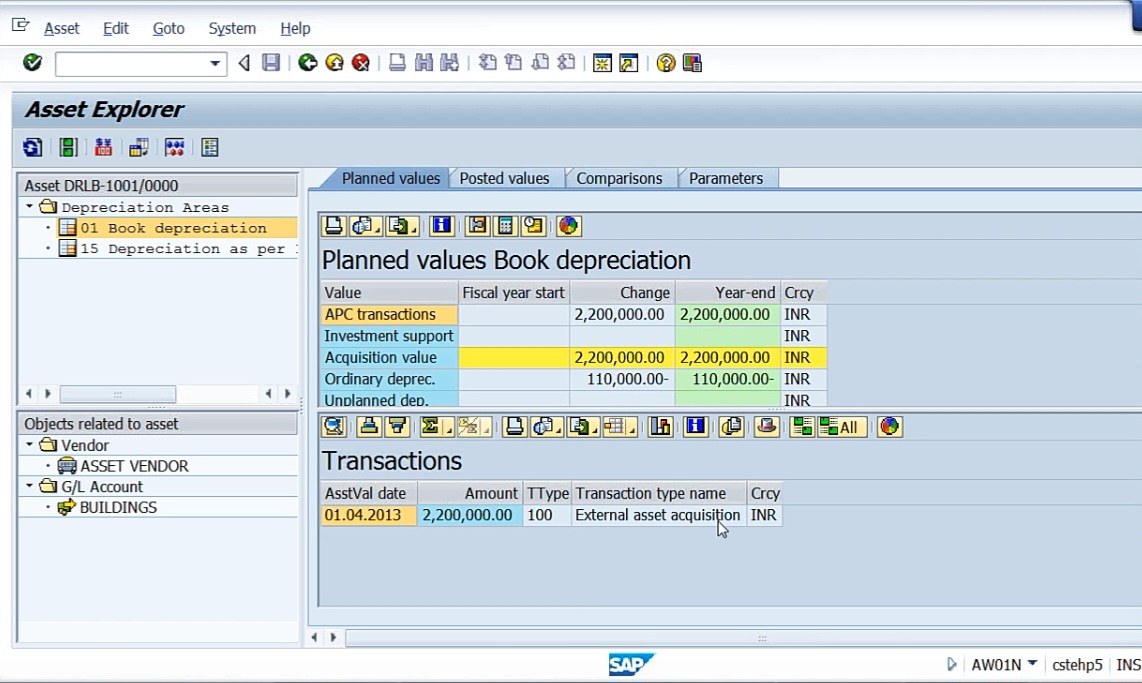

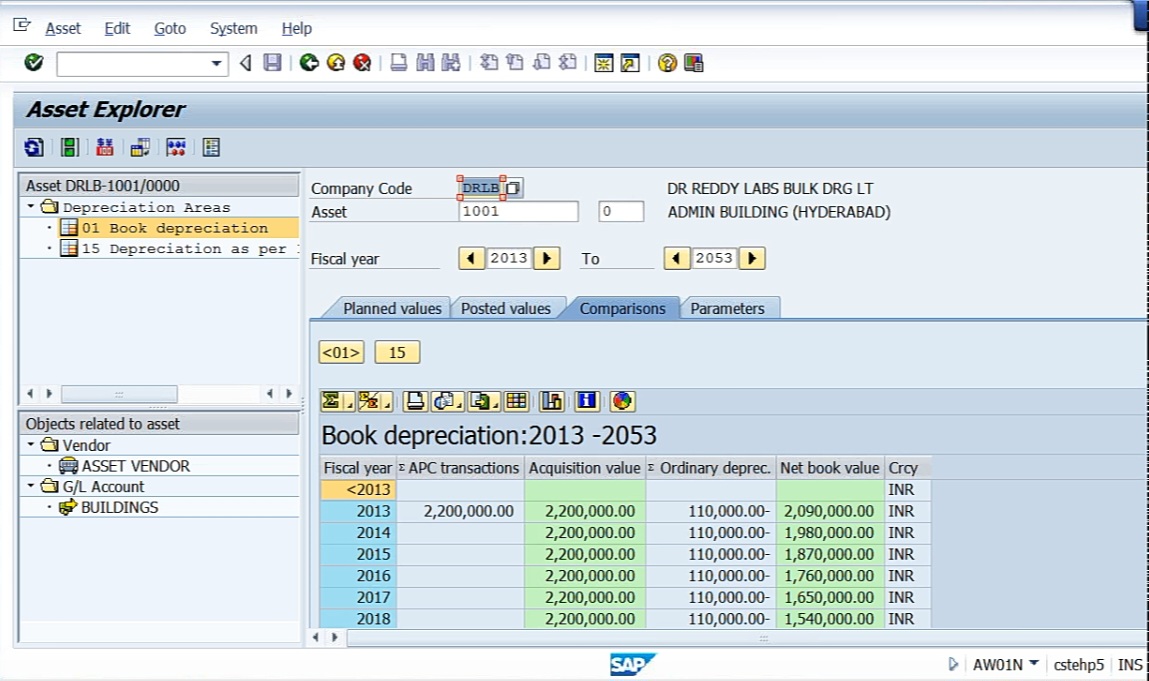

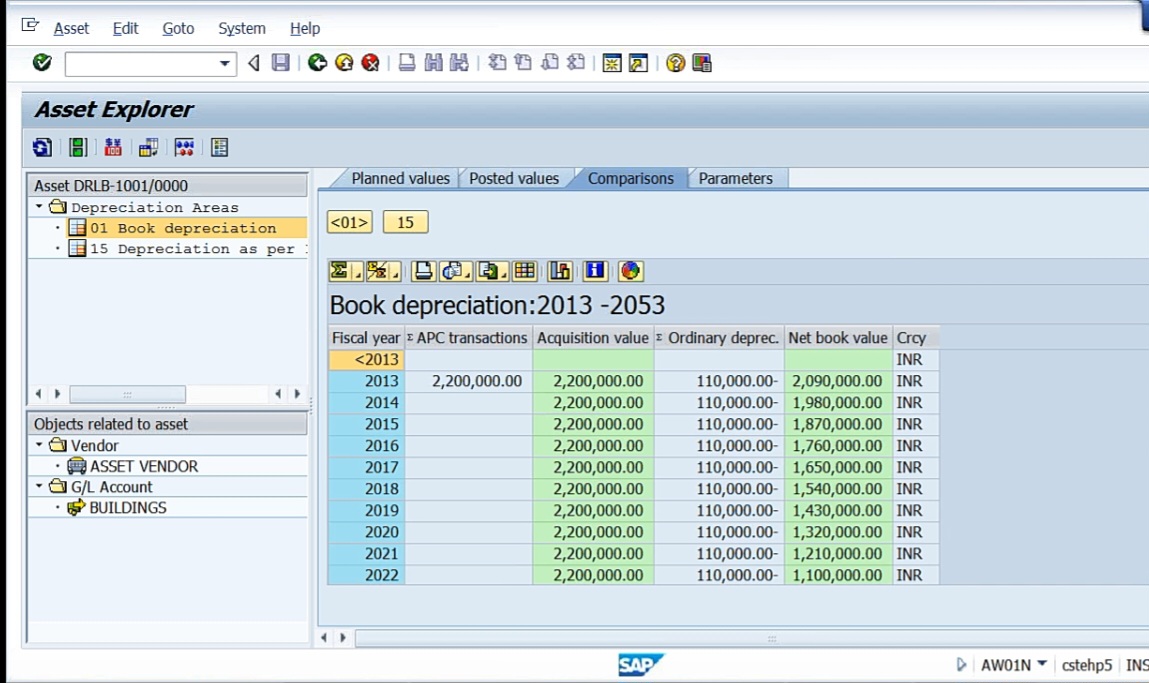

So 22 lakhs external asset acquisition. So this is admin building Hyderabad. Here in the is Aw01N, different tabs will be given. Now see for 1,001 admin building. We have the planned values, 22 lakhs, Posted values. Comparisons. See 2013 to 2053.

Means we have taken 40 years. And the parameters say 40 years useful life of the asset. So whatever the useful life that you have given here, in comparison, system will show you the value of the asset for that many number of years. And even here, for admin building also, I can maintain residual value. So what I will do is go to depreciation areas. Here, scrap value percentage I can give. I am giving 1 lakh, I can give either percentage or I can give straightaway the amount. See now, go to asset values, comparisons. See here. 1 lakh.

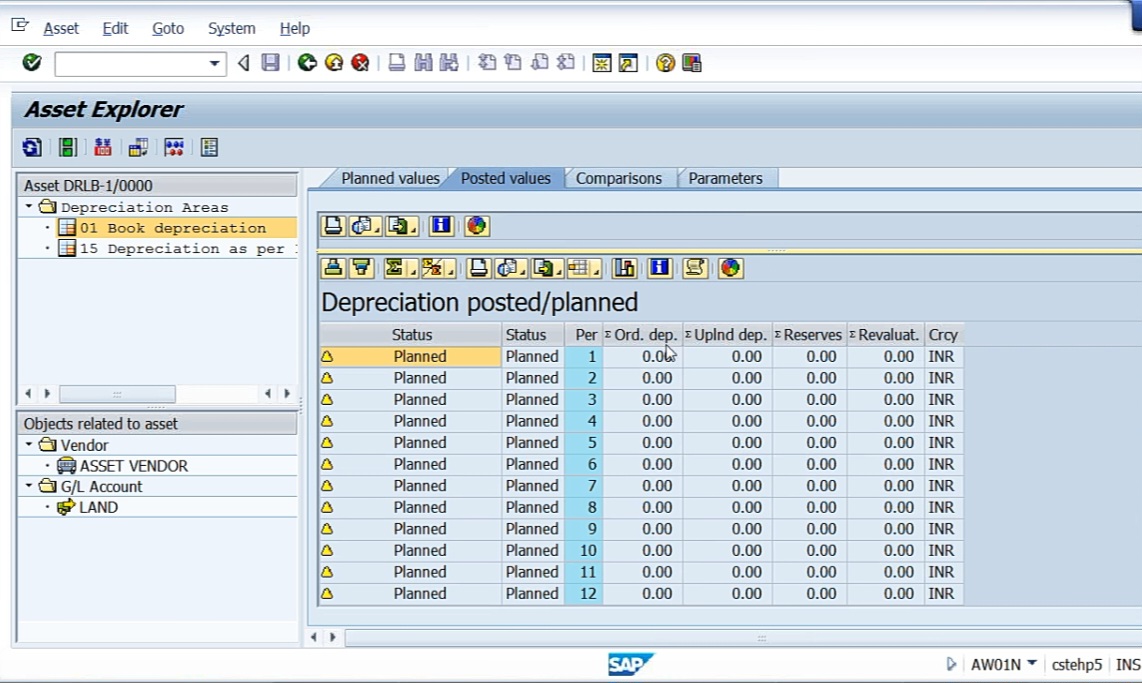

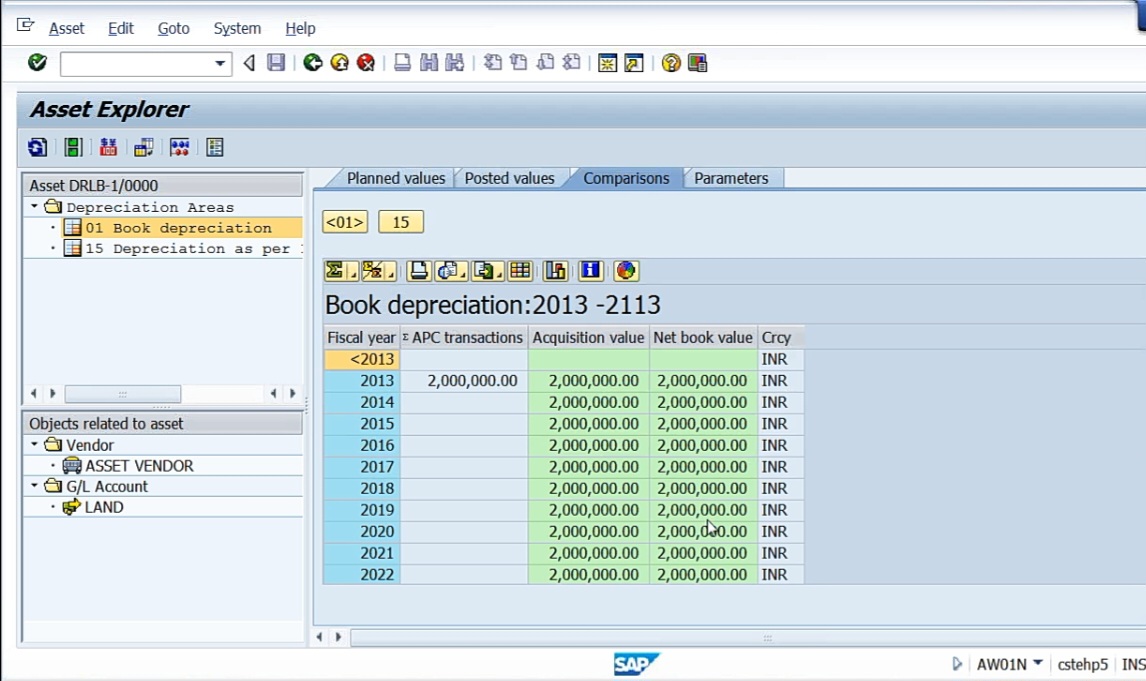

As long as the asset user life is given, system will maintain the scrap value of the asset. And if you want to see asset number 1, land. On land, no depreciation. Land values 20 lakhs. Then posted values.

So here, depreciation is 0 because we have given there’s no depreciation on land. Only appreciation, but no depreciation. Comparisons for 100 years, 2013 to 2113.

The value without any depreciation. So asset explorer is one of the crucial things which will contain so much information with reference to the asset. As soon as you procure an asset, system will plan the number of years and the depreciation, the residual values, everything. So this is about asset explorer.

Now once we acquire the asset, I can provide no depreciation also. Now depreciation is one of the crucial part. See in case of real scenario, providing depreciation on different assets. Other than SAP, if you are going to have, say maybe other software or even when you are doing it manually, the number of assets what you have generally will be very high. So without proper system, it is very difficult to provide depreciation on each and every asset. But in case of real scenario, we’ll have generally, in case of SAP, we’ll be creating asset master record for each and every asset. That is even for 100 chairs I have purchased means all the 100 chairs I need to create separate master records. Why? Because I want to maintain. So of course I can do mass creation of asset masters. But the thing is without SAP, what we used to do previously, 100 chairs, one lot. So we used to take 100 chairs, chairs account return to vendor. We bought 100 chairs, on a single entry, we used to post. But if you do like that, out of 100 chairs, say location of the asset is important now. Location of the asset, say around 25 chairs are in corporate office, 25 chairs are in plant, 25, we have sent it to another branch, again, 25 to another branch. In such case, we have an asset master record. See here in the asset master, we have the location. Here, under time dependent tab, location is there.

Location is there, plant is there. So if one chair we are maintaining here means, here every chair I can give business area or if it’s a plant because, see, this is a heavy plant and machinery. If it’s a heavy plant and machinery, which plant it is going to be linked to? So all those things we can do here. So for that purpose, we have to take if it’s 100 chairs we have procured means each and every chair I can create a master record and I can take the location of the asset, that is business area of the asset we can take. So that advantage we have. Otherwise, what we can do is we can take all 100 chairs in one lot with one shares account return to vendor account, all we can put it into only 1. But in case if you are going to put it into 1, only 1 master record is sufficient for that. That depends upon the requirement of the client. But in such case, you cannot track if any chair is taken to some other place. But if you are maintaining separate master records, I can track each and every asset where this has been gone. So generally, high value assets, every asset will be created separately.

So next, what we’ll do is look at depreciation. Regarding depreciation, it is a periodic processing. And, one more thing, in case of other than SAP, generally, we provide depreciation once in a quarter. Once in a quarter means, say, April, May, June, so on 30th June, we provide depreciation. For once in every quarter, we provide depreciation because on or before, 30th June, means within 1 month/ within 30 days from the date of completion of the quarter, I need to submit my financial statements to the SEBI. For all public limited companies, I have to prepare my balance sheet and P&L account because so many investors have invested funds in my company, it is my responsibility to show my books of accounts to all shareholders, they are the owners of the company. So for that purpose, every company will provide depreciation once every quarter. But since SAP is there, I have a provision to post the depreciation on monthly basis. Every month I can prepare my balance sheet and P&L account. In such a case, no management will leave without creation of balance sheet and P&L account. And if I’m going to create my balance sheet and P&L account, now I need to take all expenses into account, so for that purpose every month I need to provide depreciation. So for that purpose we have to execute depreciation every month. So every month we provide depreciation.

For the purpose of providing depreciation I have four methods. Go to Depreciation Run, AFAB

Planned Posting Run: means nothing but every month the planned depreciation I have to execute it. So for that purpose, regularly we use this only.

Repeat Depreciation Run: this is nothing but say for one particular month we have provided depreciation, say for example take September. September is half yearly closing, so what we have done, we have completed providing depreciation for the month of September. After completion, management again taken addition that to take one more asset into the books of accounts. Because here for assets, we have purchased on 25th of September. And, we thought, let us not take these assets into books of account. So that’s why they have not given us, and we have not provided any depreciation. Because that though they have acquired the asset, they have not taken to the books of accounts. But subsequently after they’re informed that in case if you are going to take the assets into the books of accounts, we can claim 100% depreciation for the purpose of income tax. But as for the Company’s Act, generally, the day on which we have taken the asset from that date onwards, we can calculate depreciation. But whereas in case of income tax, if asset has been acquired before September 30, then I can claim depreciation for the total year. In case if I acquire the asset after September 30, then I can provide depreciation only for the half year. So for that purpose, management has taken addition to take the assets into the books of accounts on, say, September 25. So when they have taken the decision, by the time we have already executed depreciation run. With retrospective effect, I have to provide depreciation now. So for that purpose, I’ll be using repeat depreciation for those assets which are taken into the books of accounts after the execution of depreciation run.

Restart Depreciation Run: restart is nothing but when during the depreciation run, say for example in real scenario, you’ll find in case of bigger companies, one lakh assets, one lakh 50,000 assets or two lakhs, like that, it must be huge in number. In case bill of the depreciation run, some runs stopped working, then in such case, we take a restart run.

Unplanned Posting Run: so whenever after completion of the year for the purpose of finalization of accounts, etc, you want to post any separate depreciation, then we can use unplanned posting run.

So how to provide depreciation etc, we’ll see in the next class.