Asset Accounting 1

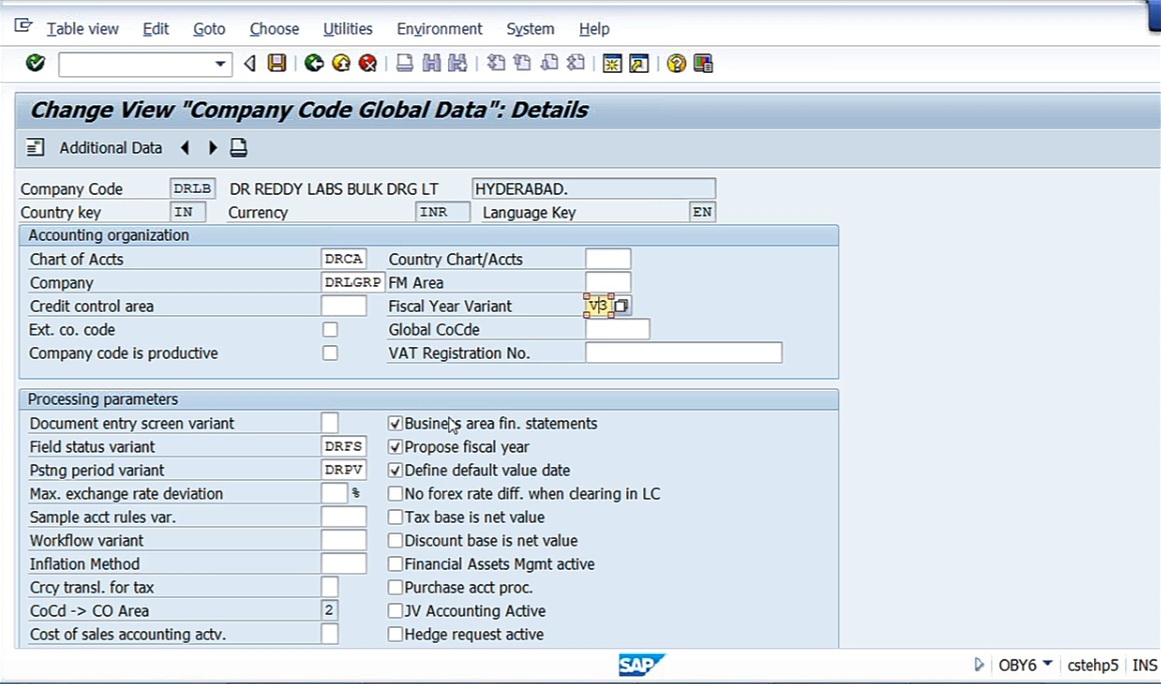

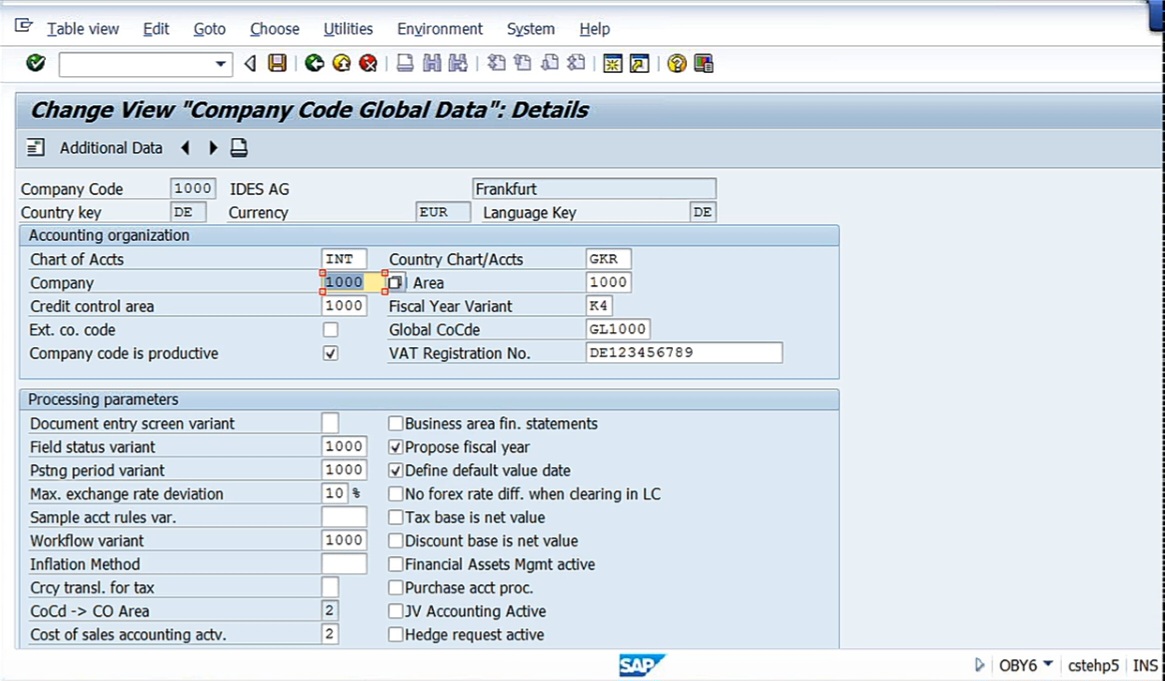

We are looking at the integration that has already been done for a company called 1000 company code and chart of accounts is INT chart of accounts. See, our company is Doctor Reddy Lab DRL. DRLB is our company code, and DRCA is our chart of accounts. Similarly, in SAP the standard company codes are there. The standard company codes are, say 1000 company code, and INT is the chart of accounts. See, if you see the transaction code, OBYC6. Global parameters, we can see.

Thank you for reading this post, don't forget to subscribe!

So here, see, we can see our company code, DRLB, chart of accounts, what is the group company, what is fiscal year, what is field status variant, posting variant, all these things we can see. So like this, when we buy SAP, this SAP IDS version, here we have standard company code.

Standard company code like 1,000. 1,000 is the standard company code, and all these things are already defined for this. The FI MM integration, SD integration, everything has been defined. So for this company code, 1000 is the right company code. And, so DE, that is nothing but Germany is the country key. Chart of accounts, INT. The group company also, 1000. And, country fiscal year, variant K4. Like this, all the parameters you can see here. So we are going to watch how this fellow has done integration, right, in OBYC. OBYC is the t code. So in OBYC, we are going to see the standard settings, what integration settings have been done by this company. So we have gone through some of these things already, what is meant by valuation class, what is meant by moment type, the material types, ROH, FERT, HALB, HAWA. So raw material is ROH, finished goods FERT, and HALB means semi finished goods like this. And for each type of material, system identifies the valuation class. This valuation class will be defined in the material master record. And the same thing we are going to see here in the OBYC configuration settings.

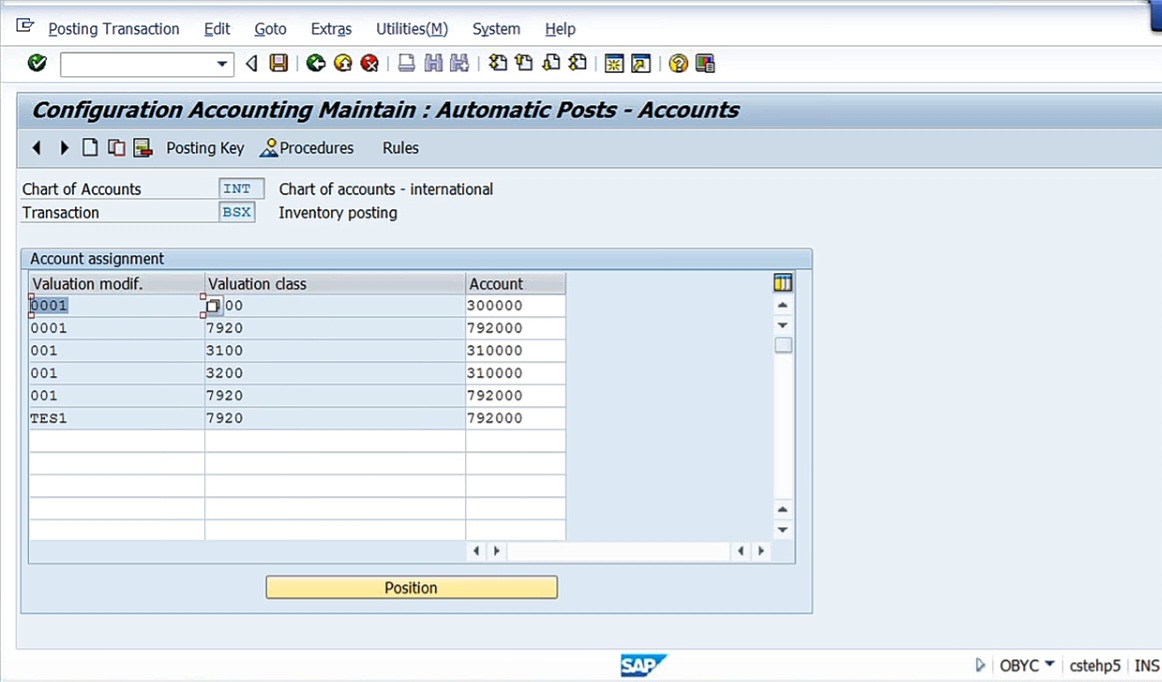

So first is BSX, inventory posting. And, also, I told you what are the accounting entries we require when goods are received. Inventory of raw material account at return to GR/IR clearing account. And, so here, the receipt of material is done in 2 phases. One is when raw material is received, another one is when invoice is verified. So invoice is verified means one person is going to receive the goods and another person is going to verify the invoice with reference to the purchase order. So purchase order is an order, is a document which is given to the vendor in which all the supplying conditions, pricing, and all other conditions will be given. So with reference to that purchase order, how much material has been received, and how much is still pending, all those details will be there. So when material is received in the plant, inventory is recorded and taken into the books of accounts, and material is physically taken and stored in the warehouse. Then subsequently so the T code, what they use is MIGO. And, in that MIGO transaction code, the receipt of material will be executed. At the time inventory of raw material account returned to GR/IR clearing account is the accounting entry. Subsequently, when invoice is verified, this GR/IR clearing account will get nullified, and ultimately, vendor account will get credit. So when commercial invoice is received by the finance department, then the sender will be asked. So for that purpose, for getting that entry, we need to configure, like, say here, in OBYC, for inventory posting, the accounting entities are BSX. Double click on this. INT is the chart of accounts.

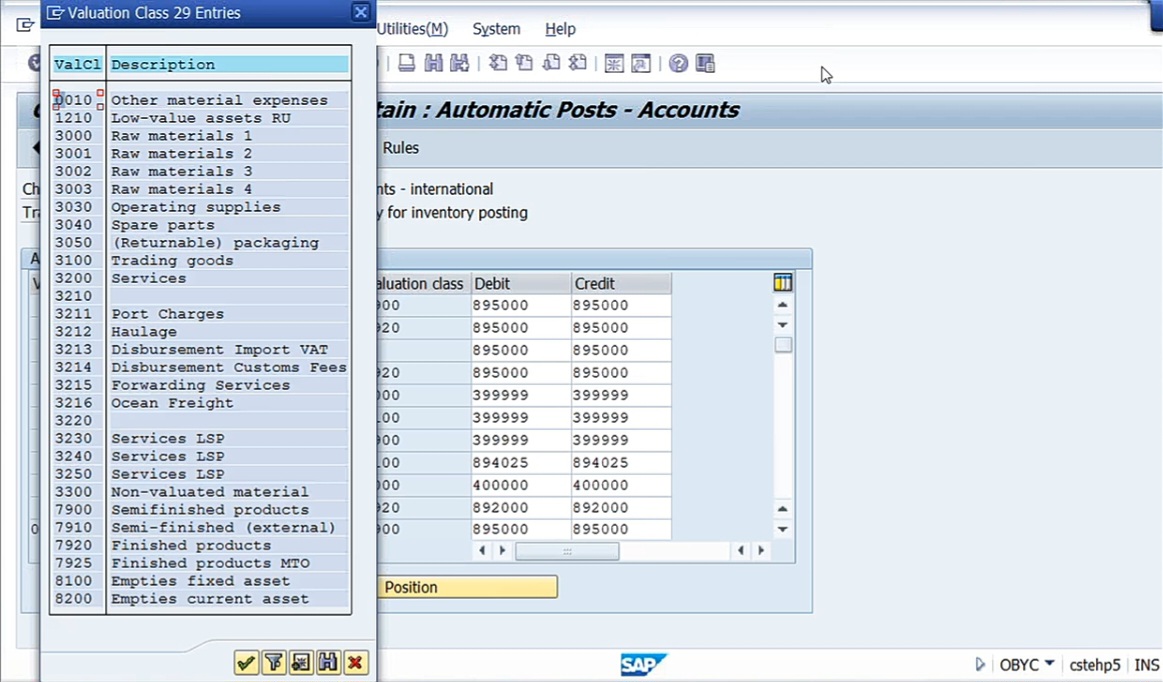

Here for 0001 is nothing but a plant that is referred as valuation modifier, and 3000 is valuation class, 7920 is finished goods, 7900 is semi finished goods. So, in case raw material is received, this is the account to which it has to be posted. All these things we have seen, and the offsetting entry. See, this is when inventory is received. When raw material is issued to the production order, the accounting entry is going to be raw material consumption account is debited and inventory of raw material is credit.? This is the accounting entry. But I told you there are several types of material issues. It may be raw material issued to the production, raw material issued to the sample quality report, and raw materials may be issued for scrapping, etc. So how system should identify, for that purpose, general modification has been given. General modification key has been given. So here, in order to post this accounting entry, whenever raw material is issued, raw material consumption account is debited and inventory of raw material account credited. So in order to get this accounting entry, what we need to do is so, here in OBYC.

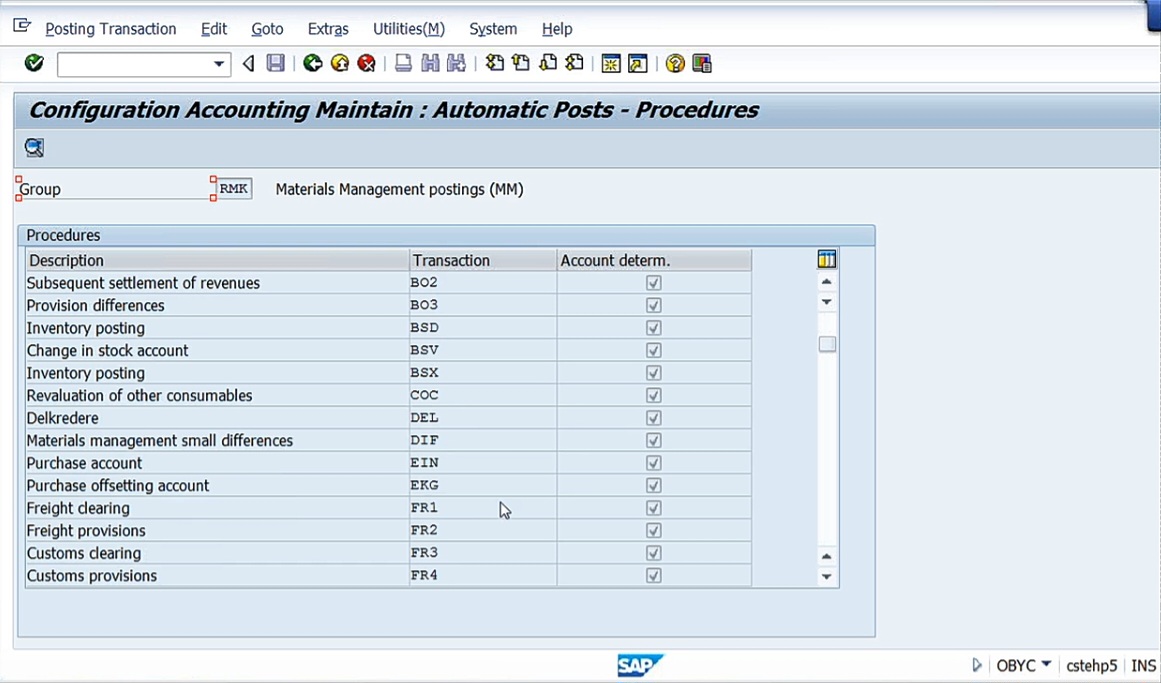

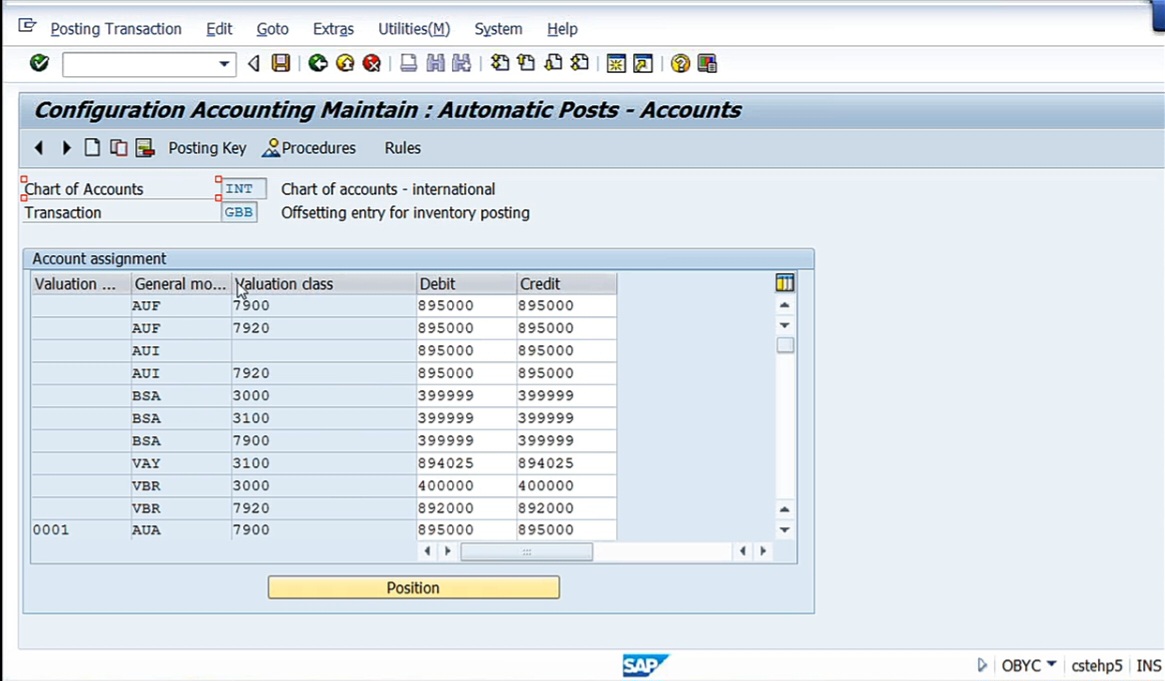

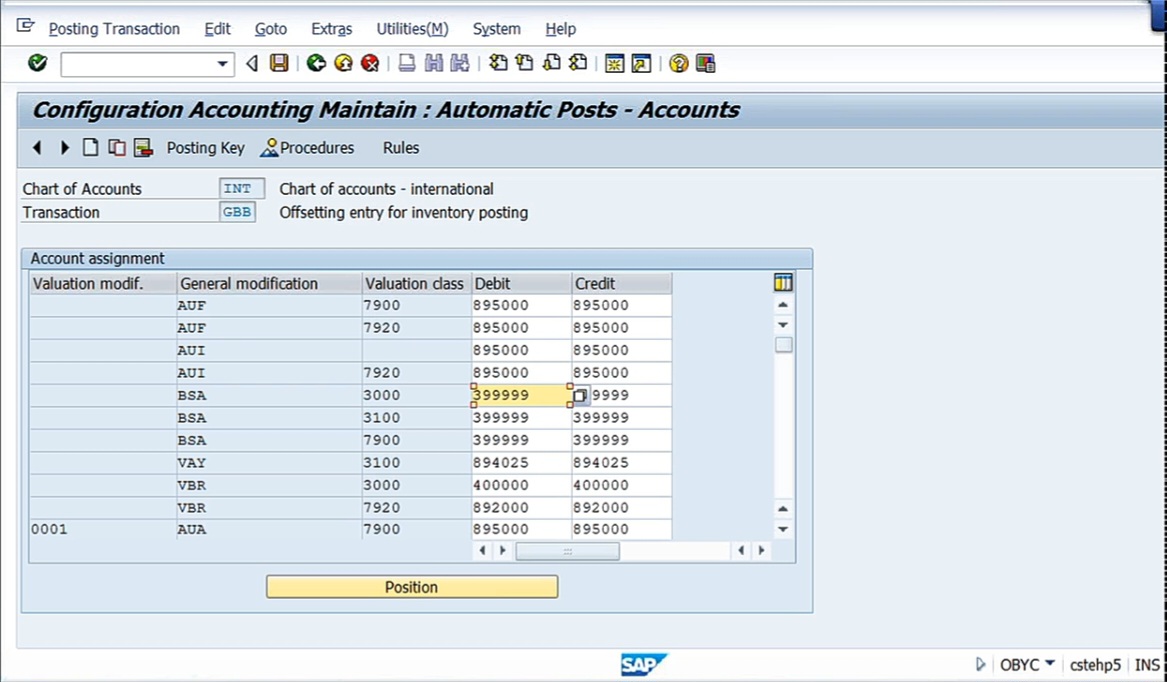

BSX is for receipt of raw material, then GBB is the transaction key for offsetting entry for the inventory posting. Double click on GBB.

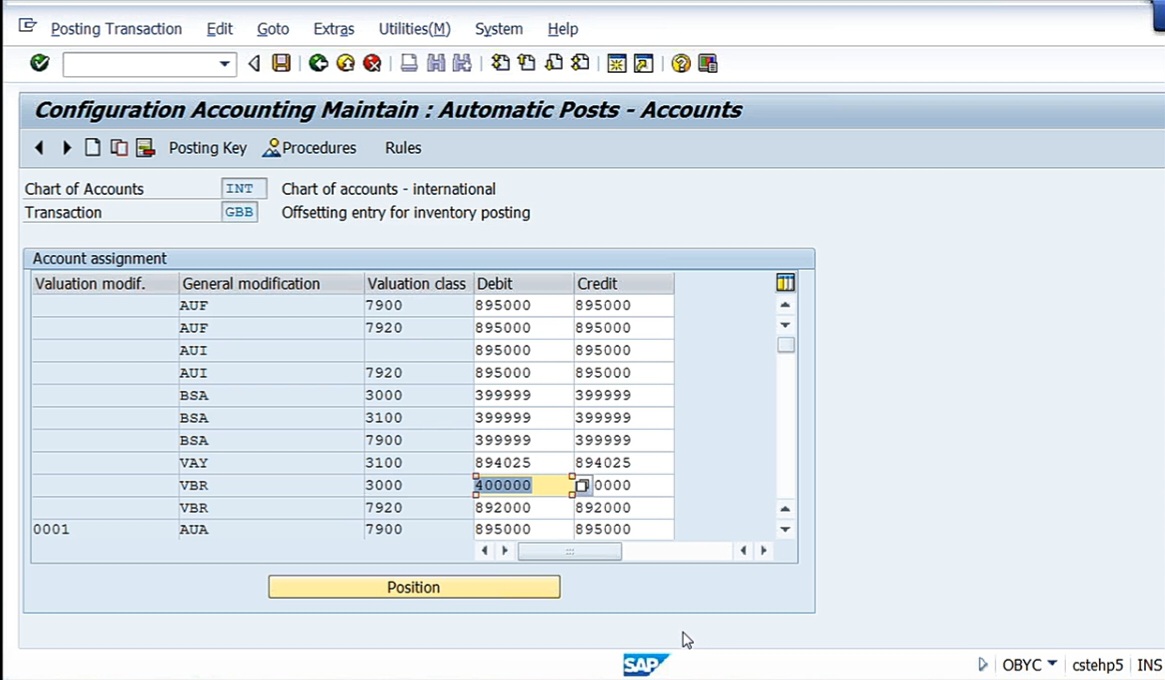

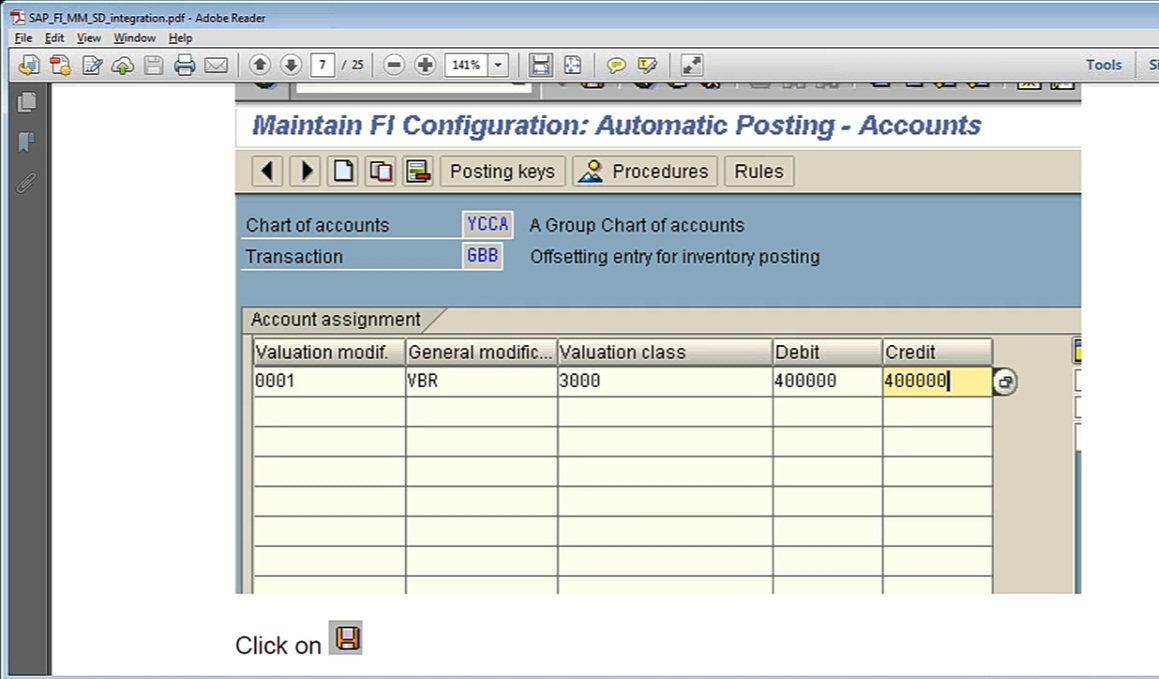

Then here, these are the configuration settings. See, let us see here. See, as an FICO consultant, our job is just to give the GL accounts. But before we give the GL accounts, we need to understand what is meant by valuation class, what is meant by general modification key, etc, we should know. In the notes below, raw material consumption account is debit, inventory of raw material is credit. So, inventory of raw material, we need not do any configuration further. The reason, already BSX has been given. BSX in combination with 3,000 valuation key will be posted to this account. So that will be credited. So that’s why there we have given credit as well as debit both. See, everywhere the credit and debit is given. When inventory is received, that is debited. When inventory is issued, that is credited. So that’s why for the second line item, we need not do any further confirmation. But for the first line item, I need to give. So raw material consumption account is debit. In order to give the debit, means here raw material is consumed. For that, GBB is the account key. But a raw material is issued out here. Raw material issue may be for different purposes. Raw material issue for sample, raw material issue for consumption, raw material issue for scrapping. So like that, the issue of raw material may have different purposes. So for that purpose, we need to inform the system because depending upon the purpose, we need to give the GL account. So for that purpose, what we need to do is, this GBB should be associated with a general modification key. Instead of writing here consumption, here BSA, something like that is given. The transaction key GBB needs to be updated. GBB key is used for various offsetting posting entries. For various offsetting posting entries means consumption, for sample, for scrapping, like that for any purpose, raw material can be issued. So within GBP transaction, there are various account grouping that is general modification. In this case, you need to update general modification VBR with raw material consumption account. What is VBR? VBR indicates consumption of material. Just to simply imagine that VBR is nothing but consumption of material. See also for 1000 company code and international chart of accounts, see here, VBR. VBR means nothing but consumption. 3000 indicates raw material and 400000 here indicates the GL account. So GBB is nothing but offsetting entry, that is issue of raw material. VBR indicates for production, that is raw material consumption for production, and 3000 indicates raw material. If raw material is going to be used for the production purpose, against VBR, I have to give GL account 4 lakhs. Let us see what is 4 lakhs. Go to FS00.

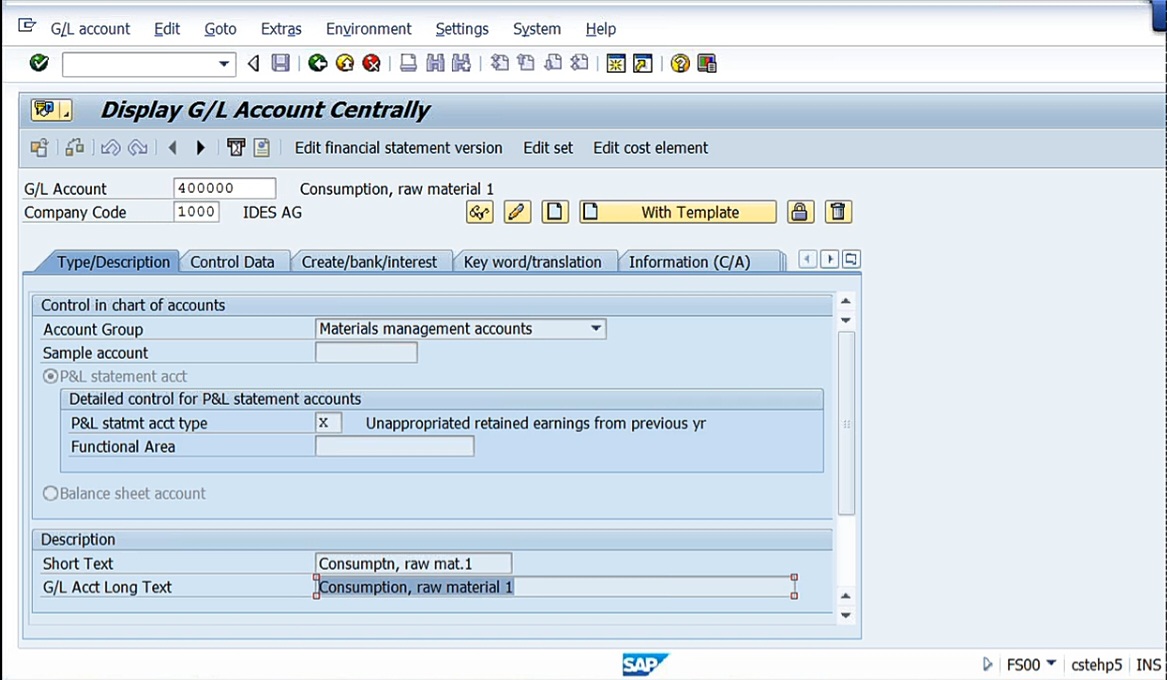

See what is the GL account? Consumption of raw material.

So consumption of raw material means here, see 3 lakhs against VBR, 3,000 valuation class indicates raw material and 4 lakhs indicates consumption of raw material. So as an FICO consultant, see our MM friends will say that, boss I have already configured these things, you give the GL accounts. So what we do, we give them the GL accounts. During the blueprint stage itself, we’ll finalize all the GL accounts, what is the GL account to be given for raw material consumption, what is the GL account to be given if raw material is issued for scrapping, what is the GL account if raw material is issued for sample quality reporting. So for all those purposes, for each purpose, there is a GL account because if the raw material consumption means consumption account, scrapping means loss account, sample means sample testing account. Something like that you have to give.

So VBR always indicates, issue for consumption of raw material. So that’s why it says that, in this case, you need to update general modification VBR with raw material consumption account.

So 0001 is the plant, VBR is the general modification key. 3000 valuation class indicates raw material valuation class and 4 lakhs is nothing but condominium account. Similarly, when initial stock is uploaded for raw material. Initial stock uploaded means what? Taking up or uploading the opening balances. Because when you are uploading more opening balance, raw material account is debited. So one stock data takeover account is going to be credited, one debit, one credit. There should be double entry bookkeeping. So that’s why when raw material is taken, inventory of raw material is debited and stock data takeover is credited. So inventory of raw material, for that already we have given that setting, that is BSX is the transaction key and against that, value valuation class 3,000, and then we give the GL account. So for raw material account, we need not give any setting again. But second one is stock data takeover is credit. This is the opening balances we are taking up. So for this purpose, the transaction key GBB needs to be upgraded, general modification key BSA needs to be upgraded with the stock data takeover account. Let us see this. Against GBB, BSA.

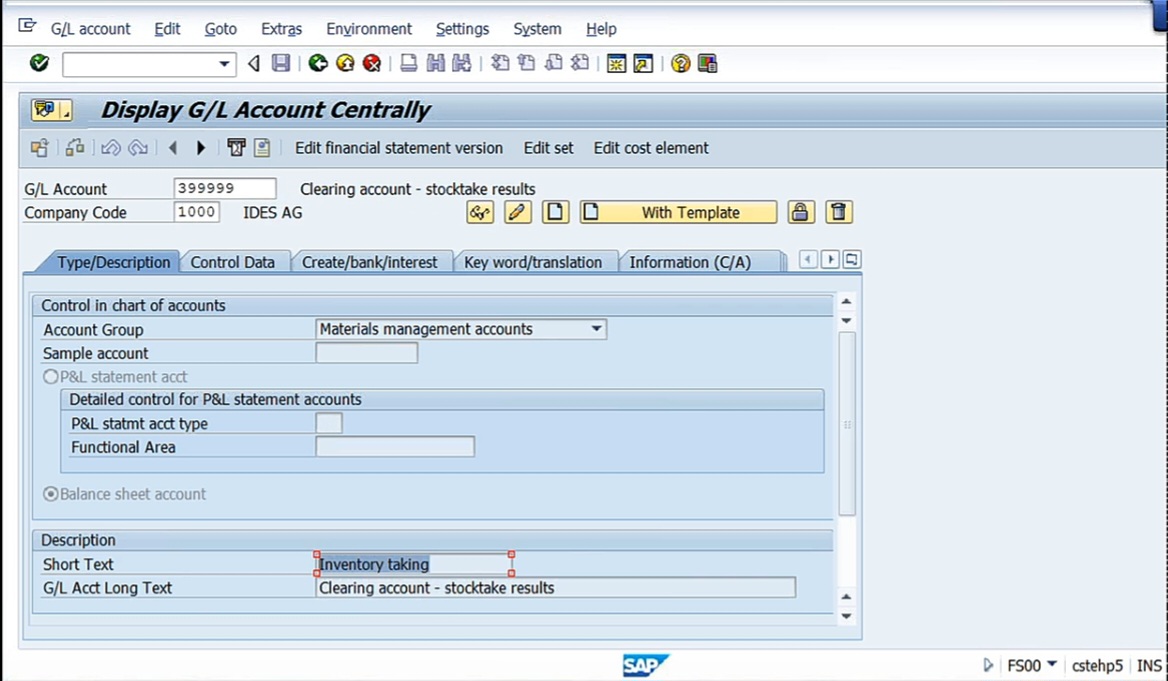

See, this is GBB and BSA. BSA raw material. 3 lakh 9999. So this is opening balances upload account. Stock data takeover, that’s called.

See inventory taking. Stocktake results clearing account. Inventory taking, this is nothing but inventory, opening balances we are going to upload. So if we are going to do these settings here, the standard settings, INT chart of accounts, GBB, so for each thing, either BSA or VBR or all these things, again, for each and everything. So this is raw material. 3,100 is nothing but trading goods. 7900 semi finished goods, that also will be consumed. So the transaction with GBP needs to be upgraded. Similarly, when goods are received, goods receipt is made for finished goods against production order. Whenever we receive the goods from the production, then the accounting entry is finished goods is debited and change in finished goods is credited. And here, the transaction key BSX for the validation class so and so. For the change in the finished goods, we need to create, GBB against AUF. See here.

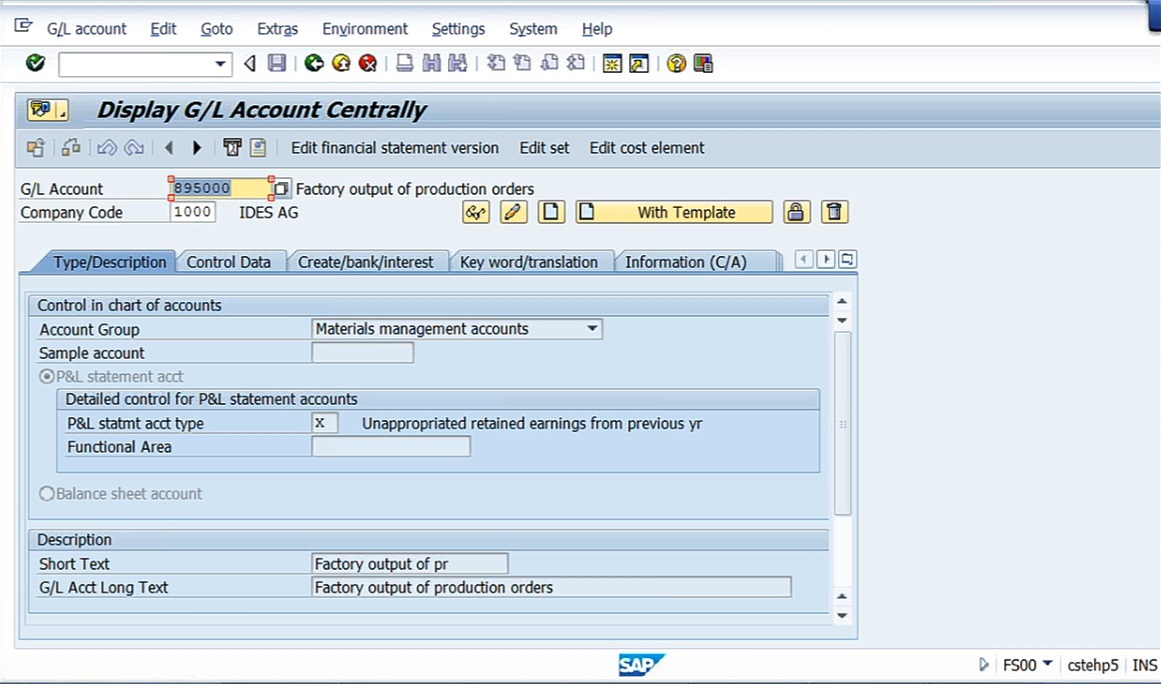

GBB, AUF. 7,920, nothing but finished goods. See this account.

Factory output for production. Means, whenever finished goods are going to be generated from the production, so we post to this account. So, like this for every accounting entry, it has been given. Try to understand, okay, what we do after some time, once we go to certain stage, if possible, I’ll tell you how to create MM records because when we go to the controlling, I’ll tell you how to do the configuration for the materials management, and certain settings will do and certain integration settings also will do it, so that you’ll understand how integration actually works. But here, let us stop here to this this extent. How integration works, that’s what we have seen. We have heard about the new terminology like valuation class, moment type, all those things we have seen. So let us close this and see the MIS, then we’ll start asset accounting. So asset accounting is a little more complicated topic when compared to the GLERAP. GLERAP seems to be a bit simple, and asset accounting we need GL accounts, we need the AR, we need AP, all these 3 are required. The configuration settings will be a bit more and then execution of the business process. So let us see the MIS report, then we’ll go ahead with the asset accounting.

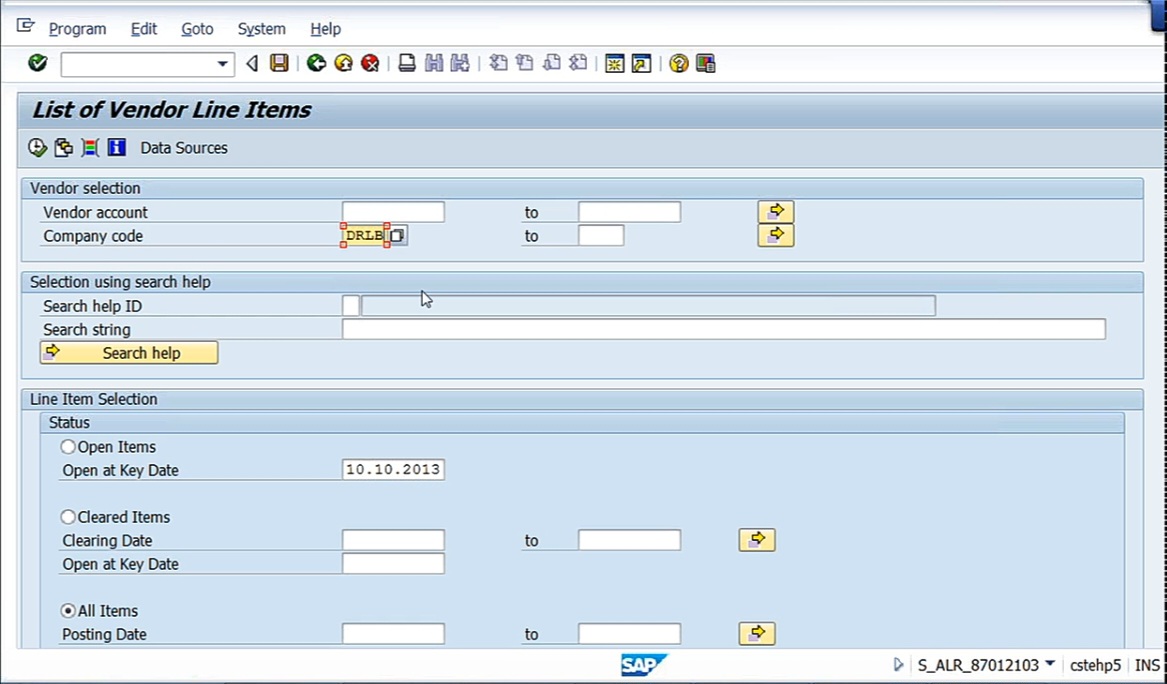

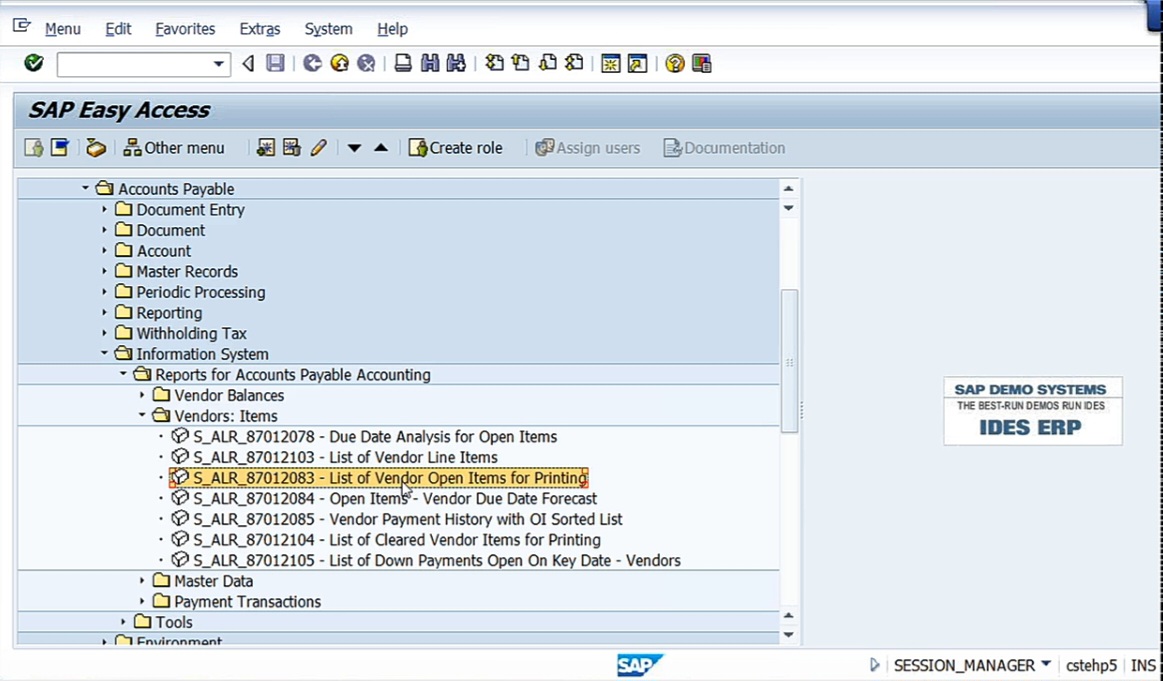

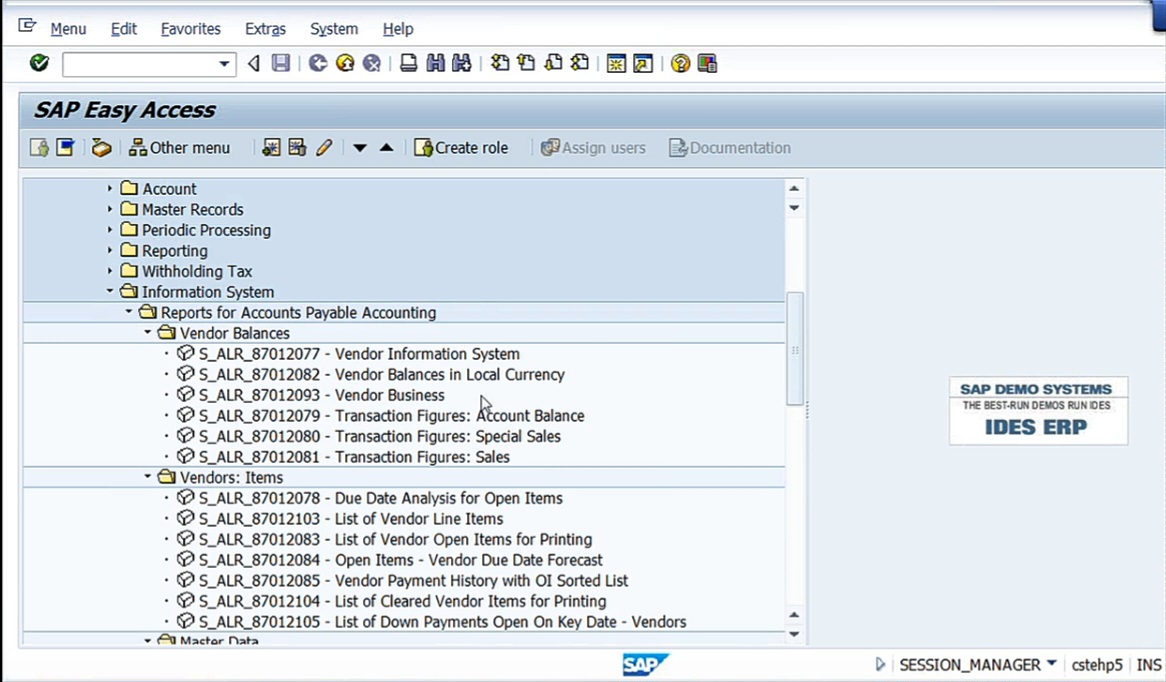

In case of MIS also, whatever we have posted, now we just need to execute the reports and we have to take it out. Here, there’s no further configuration. What you do? Go to the information system. Reports for accounts payable, vendor items, list of vendor line items. If you post more and more entries, you can see the big reports.

Here, just give only company code. Nothing more than that. You can see here the total vendor accounts and what are the transactions that we have posted to the vendor.

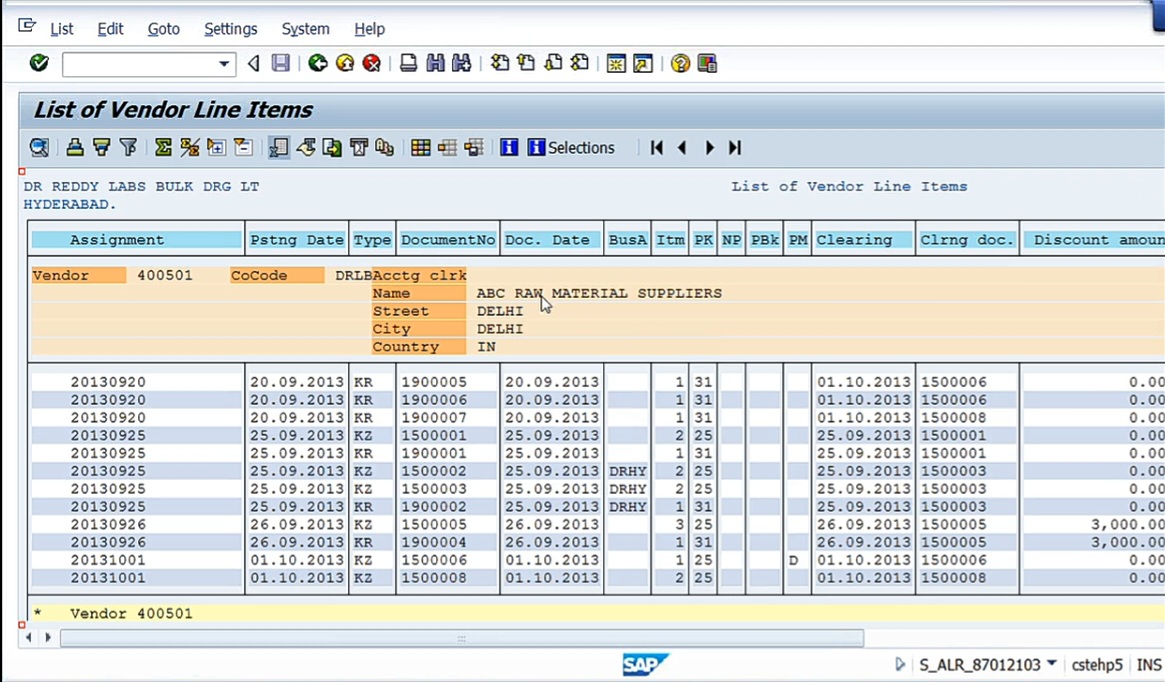

ABC Raw Material Suppliers, Delhi. So whatever the total transaction that we have posted, KR indicates invoice, KZ didn’t indicate the payment, and KG indicates credit memo like that. And 3,000 there means there’s a discount. So this is the 2nd party.

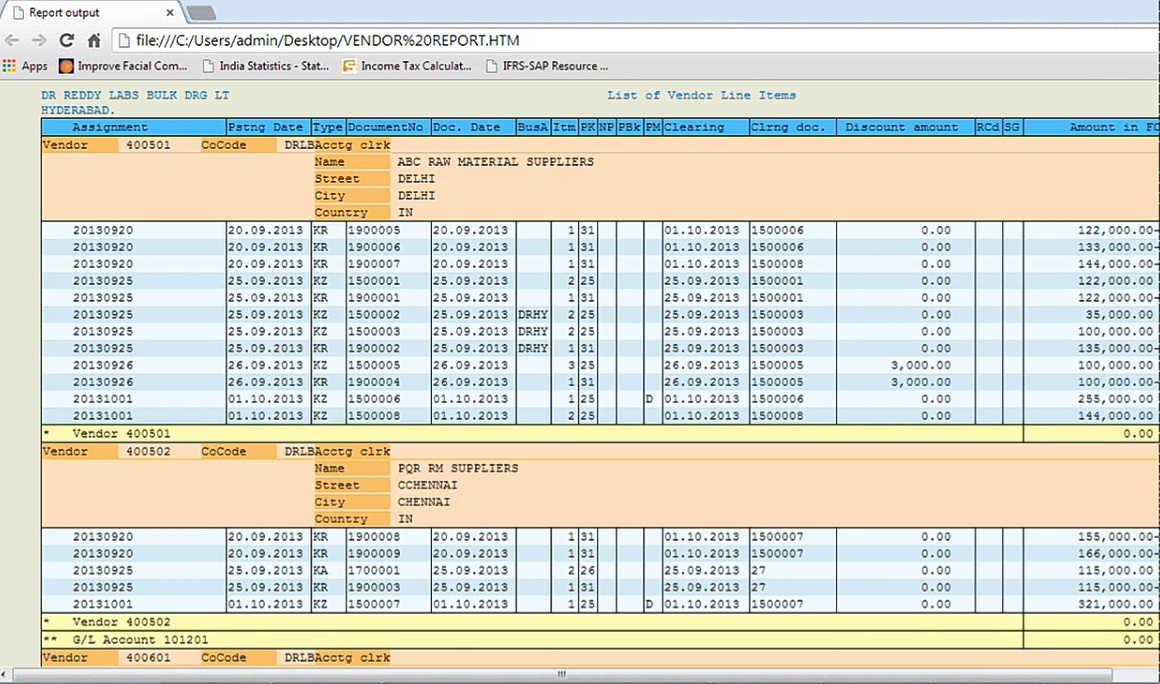

What we can do? We can go to List, Export, Local file, check HTML format. Just stick it onto the desktop with Vendor report HTML filename. Then Save.

Insert 24:32

Insert 24:32

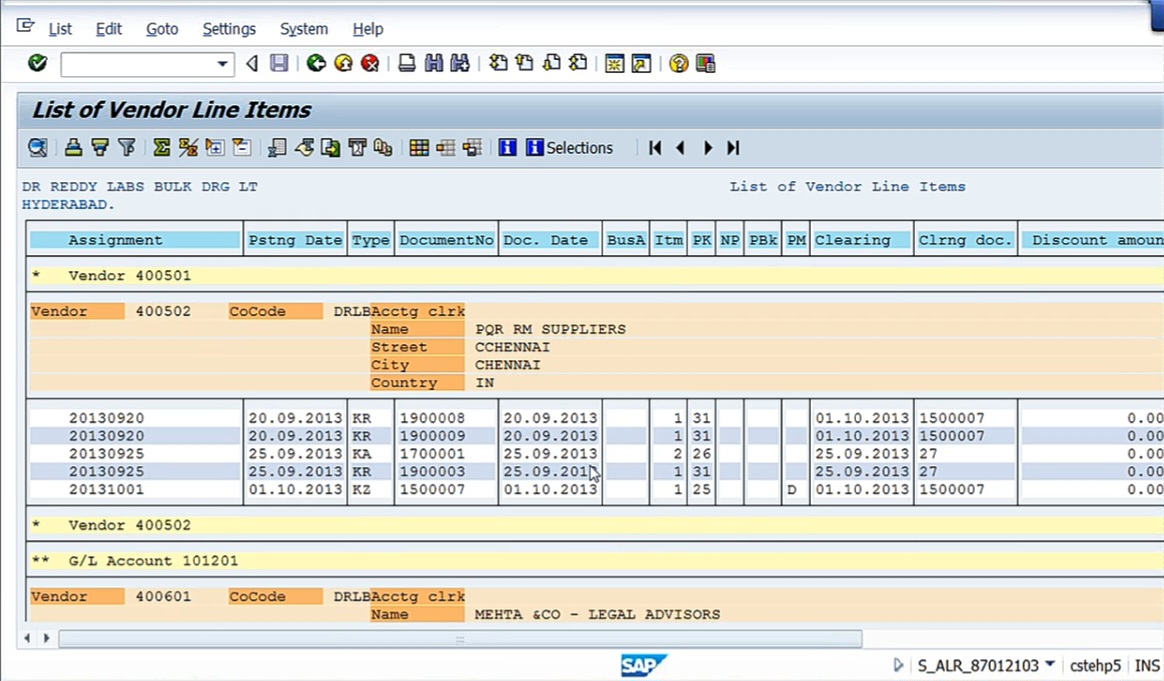

So here, you can see you can copy. As it is, that will be copied. So Doctor Reddy Lab, and here’s the name of the vendors. There’s PQR, there’s Mehta legal adviser. Like that, whatever the entity that we have posted, everything can be seen as a GL account.

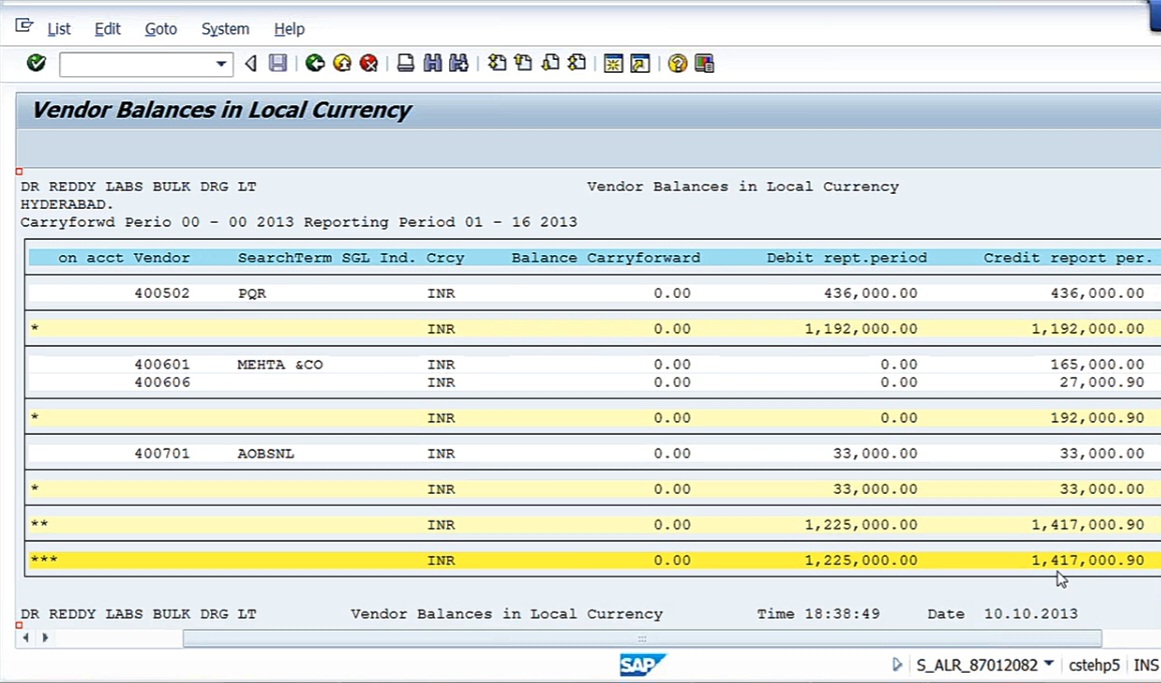

So then coming to List of open items for printing. So each and every report, just drill down and see the report. There’s master data and vendor balances. All the first one will just give you the overview, that’s all. We’ll not have any report. I’ll show you here. Vendor information system under vendor balances will only show you the tree, what reports are available, all those things will be seen here. That’s why for the time being, it is not useful for you. And vendor balances in local currency, only the total outstanding balance will be shown. That’s all, nothing more than that here. And any report you want to generate, other than this, it has to get downloaded with the help of ABAP consultant. And total purchase are around 14 lakhs 17,000.

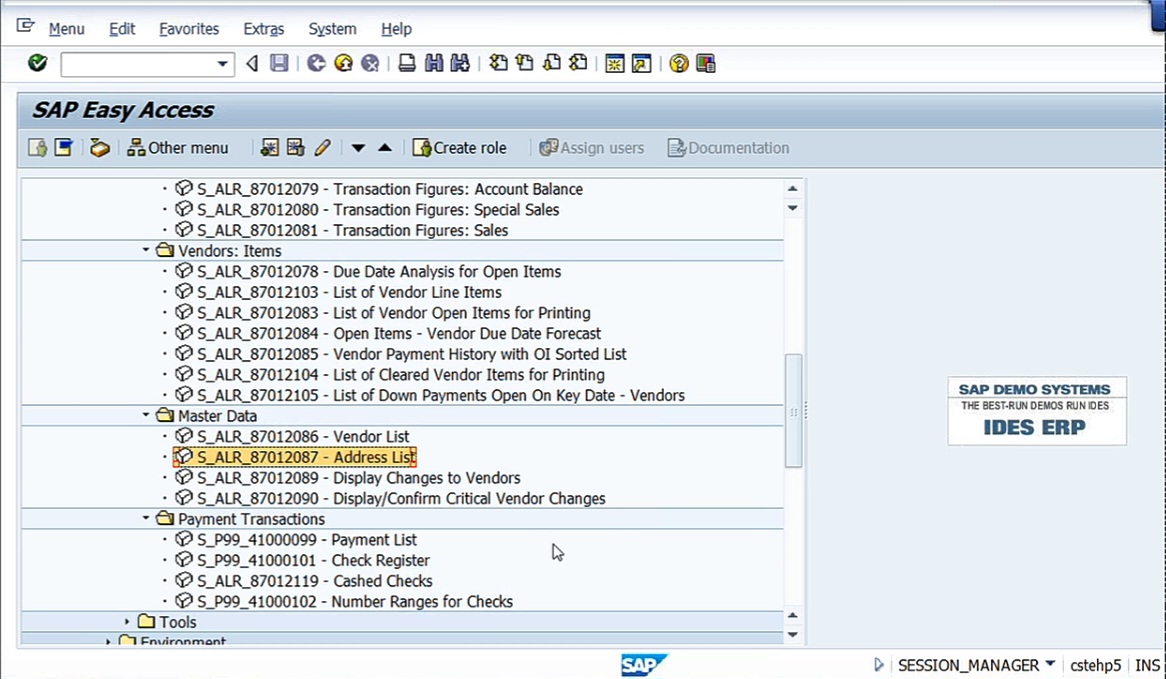

So like this, each and every report, drill down the easy Access menu and see. Vendor list, these address, the address list, etc, And under payment transactions, payment list, check register.

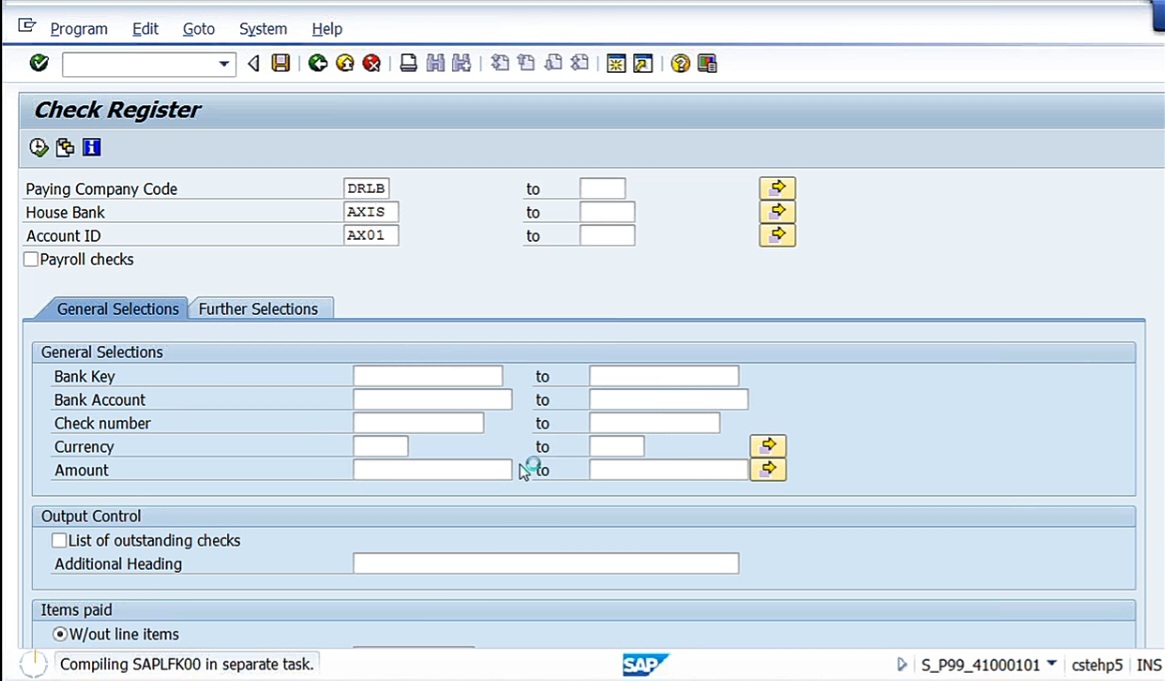

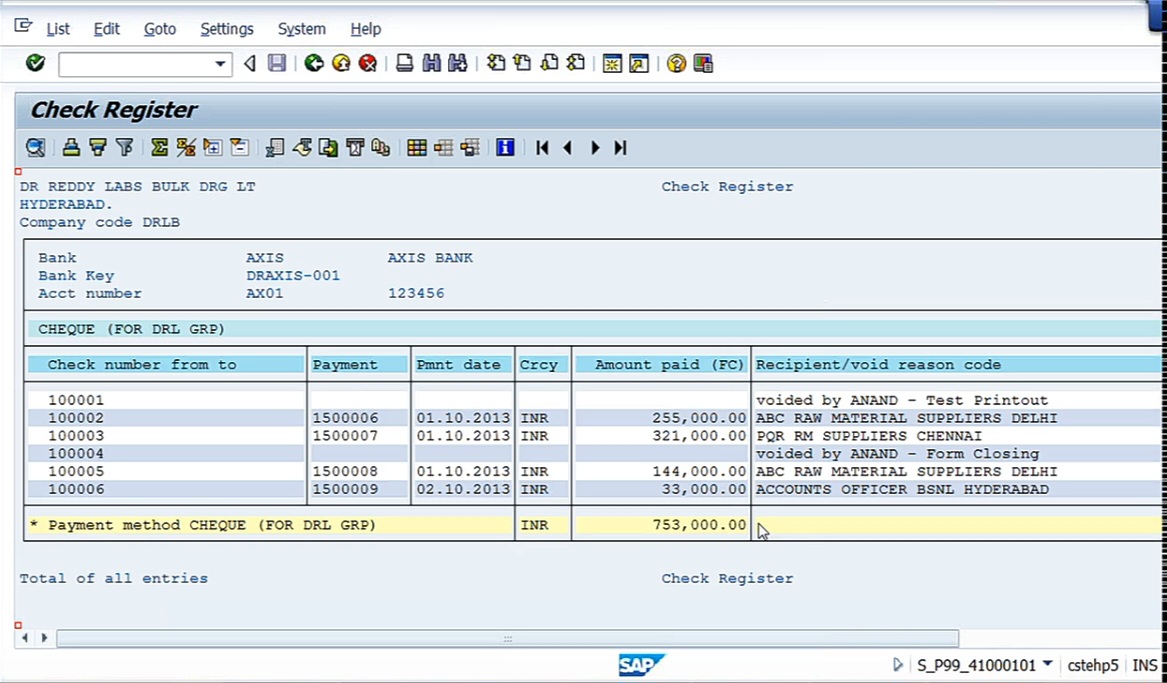

Go to check register. So paying company code DRLB, House bank Axis, Account ID AX01.

See what are the checks that we have issued.

Check numbers, up to 6 checks, payment, payment date, the currency, the amount released, the total checks will be received. And here, it it says that it has wasted 2 checks. When you exclude automatic payment program, first check and last check is wasted, and the blame is thrown on me stating that ‘voided by Anand’ and test printout. So it has been designed like this in SAP IDS version because people should not use this version for real purpose. So that’s the reason they don’t allow certain facilities.

So like this, you drill down each and every report just so you can look into that. So, we have seen this, what you call accounts receivable, accounts payable.

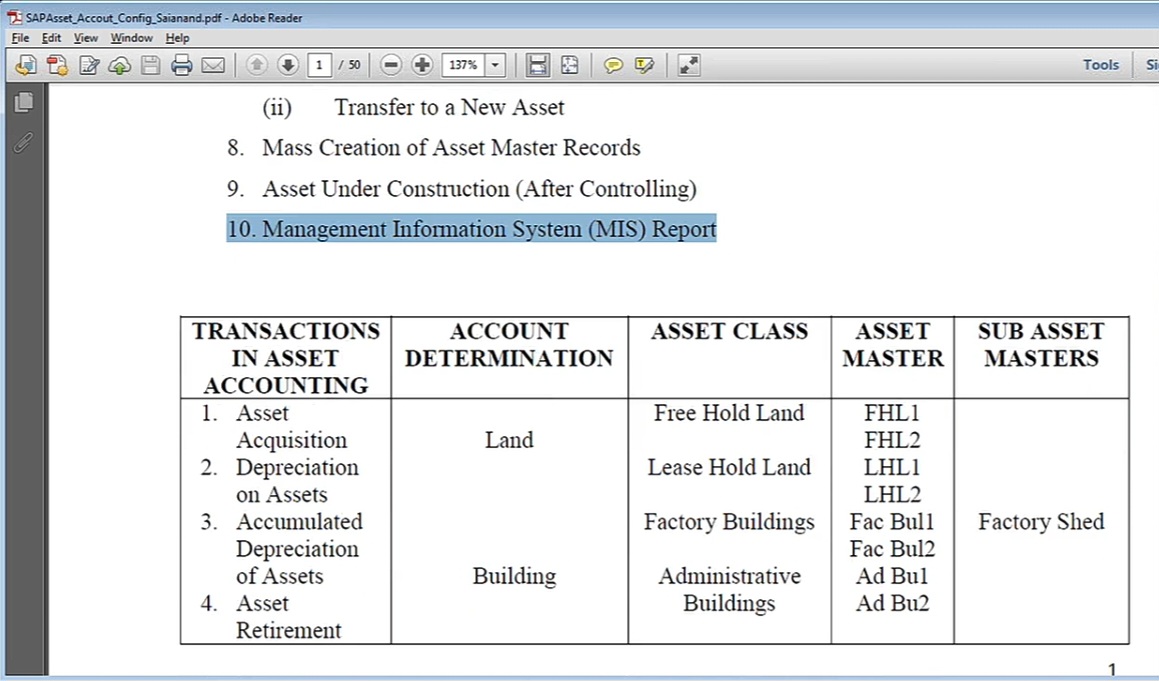

Now, we are going to see the asset accounting. So asset accounting topics, again basic configuration settings in IMG. Here, the basic configuration setting itself, it will have around more than 15 to 16 steps there, which is very much crucial. Then creation of asset master records. Then business process, acquisition of assets, how to acquire an asset. And every month, how do we provide depreciation. Generally, we have seen depreciation provided once in three (3) months whenever we make any finalization of quarterly accounts or once upon a time, we used to see once in a year or once in half year. But in SAP, we provide depreciation every month because when SAP is there, management will definitely ask for the reports on a monthly basis. All monthly, maybe, P &L account and balance sheet and asset reports and the accounts receivable reports, accounts payable reports. So monthly, we generate it. So that’s why, depreciation here, we execute monthly. We’ll also see asset retirement. What is meant by asset retirement, retirement with customer, without customer. Scrapping of an asset because when the asset is outdated and its useful life is over, we can scrap it. And transferring the asset, transfer to an existing asset, transfer to a new asset. And the mass creation of assets, assets under construction because for certain assets like buildings, a factory building is there. You cannot acquire the factory building. You can acquire an administrative building, but factory building… okay, if you are acquiring a completely new factory, you can take it as acquisition of factory building. Otherwise, if you are going to construct the factory building, how to do that? Because stage by stage, maybe 1 year, 2 years, or 3 years. Years together, the construction activity will take place in case of big companies. So as long as we are incurring the expenses, all those expenses are debited to an account like asset under construction, then that will be capitalized subsequently. That we’ll see in case of asset under construction. But asset under construction to configure, we need even controlling, that is cost accounting also should be done. So though this topic belongs to asset accounting, this topic we cannot see unless we have controlling configuration in place. Then coming to the management information system. So these are the 10 topics we’ll see in asset accounting.

See, if you take a company, typically, you’ll find certain assets like, land, buildings, plant and machinery, furniture and fixtures, vehicles, low value assets, assets under construction.

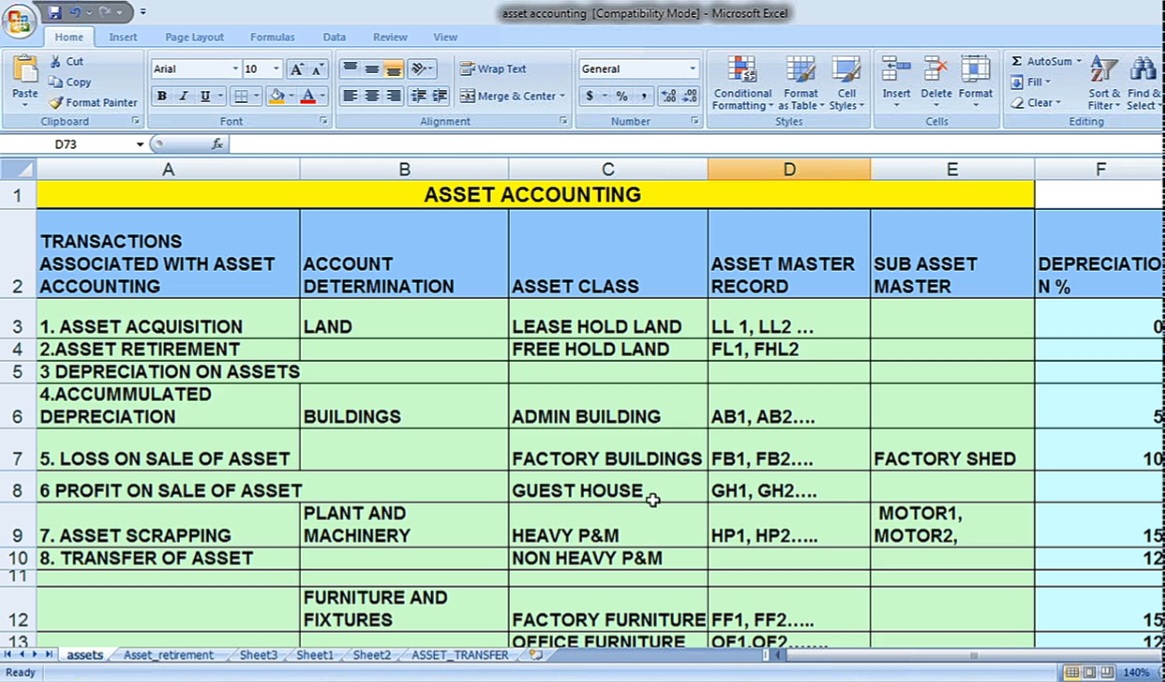

So like that, different assets will be there. Like this in SAP, we call it as account determination. Account determination is nothing but see this table also given to you.

Here, it is given. So, assets may be the main assets. See, if you observe, these are the main assets which you can find out even in the balance sheet of a company. Assets, land, billings, plant and machinery, furniture and fixtures, vehicles, low value assets, whatever it may be, all these assets, the main headings are going to appear in the balance sheet.

Asset class: Now, depending upon the asset, what we do, we classify the assets. Say, for example, land is there. Land can be divided into is leasehold and freehold. Nothing but the land which is taken on lease and land on which there is no lease, freehold. So we can hold certain lands. Maybe if in future we want to construct some factory or maybe buildings, so for that purpose, you may acquire certain lands and keep it. That is called freehold land. If you have acquired an asset, like, for example, in a prime locality, you have a big site wherein you want to construct a building on that. So building owner says that, sorry, I’m not going to sell that property. But you want it, so you can ask for a lease. So generally, land can be taken lease for 49 years or 99 years, like that. For example, here we have in Hyderabad, we have our old airport. Now we call it as Begumpet Airport. In front of the Begumpet Airport, there is a huge land there and that has been taken by one of the 5 star hotels, from airport authorities of India. And they have taken for 99 years lease, and since for 99 years that land belongs to that 5 star hotel people, they have constructed a very big hotel. So they’ll have terms and conditions, after completion of the lease period, the building, the lease can be revised or the building along with the land will be handed over to the party. For that building cost, whatever the book value, maybe that land owner may have to pay. So those terms and conditions will be written in the lease agreement. So we can classify the land into freehold and leasehold. For buildings, we have buildings like administrative building, factory building, guest house, any type of building. So we are going to classify the assets into this type. For plant and machinery, again we have heavy plant and machinery and non heavy plant and machinery. Furniture and fixtures, maybe factory furniture, office furniture. Vehicles, factory vehicles, Office vehicles. So factory vehicles means the vehicles which are used in factory like, even the buses which will carry the plant employees etc. Apart from that, say, tippers, bulldozers, so what are the heavy assets that are being used in the plant, so that can be divided into factory vehicles or office vehicles. Office vehicles are cars and jeeps, any other assets which are used for the office, even the buses also will come under that. Low value assets are an asset, say for example, calculators and certain little small or cash machines, cash registers, we call it. All those things, the value of the asset may be less. So as per the policy of the company, any asset which is less than 5,000, I can write it off as an expenditure. So initially, they’ll be shown as low value asset. At the end of the year, everything will be written off with 100% depreciation. So we call it as global asset.

Next is AUC, asset which is under construction. So asset under construction can be classified again, say maybe, factory buildings under construction or any other administrative building under construction. So like that, we can classify even that. So that is called asset class. First one is account determination, this is called asset class. Asset classification, we can do depending upon the client requirement. So before we classify it, we need to study and understand the client requirement and even the finance department, the finance people will help us, what is their requirement, in future how they want, something like that. Then coming to Asset Master Record. For each and every asset, we need to create a master record. For example, here administrative buildings are there. If you have administrative building 3 or 4, then administrative building 1, 2, 3, like that we give numbers. For each asset, we are going to create a master record. Again, master record is a permanent nature. Permanent nature means, say, GL account is a master record, customer master is a master record, vendor is a master record. So like that, everywhere we’ll find a master record, the main record. So we have to create asset master record for each and every asset. If I have 10 buildings, I have to create 10 master records. And each master record will contain a lot of information; the name of the asset, when this asset has been acquired, when this has been capitalized, what is the date of depreciation applicable, what is the location of this asset, from whom we have purchased it, any insurance there, if so, what is that, how many years this asset is going to stay long, and after completion of the useful number of years, what would be the approximate value of this asset. Oh, not one or two, so much information is available in the asset master record. Each and every asset including a chair, we have to maintain a separate master record. Say, even if you buy a 100 chairs at a time, it is better to have 100 master records so that you can identify each and every asset. Otherwise, I can take like, say all 100 chairs, I have purchased it and 100 chairs, maybe for 1 lakh we have purchased it. And you can take all 100 chairs as one asset, but you cannot identify where each and every asset has been deployed or even given. Say for example, few of the chairs may be kept in corporate office, few may be in the plant, few may be in the branch office. So to identify the location of the asset etc, better to maintain master record for each and every asset including maybe a chair, maybe a table or whatever it may be. So that’s why here we are going to create asset master record. So admin building 1, 2, 3. Factory buildings, factory building 1, 2, 3. For each and every factory building, I need to have a master record. So heavy plant and machinery 1, 2, 3, 4. Non heavy plant and machinery 1, 2, 3, 4, like that we have to have. So furnitures, vehicles, for each and every vehicle, you need to have a master record.

Now, Sub Asset Master. So account determination, asset class, asset master and sub asset master record. What is sub asset master? Say for example, you have heavy plant and machinery. Like, I think you might have heard about lathe machine. Lathe machine is a machine which cuts, used in the heavy engineering industry. Even it cuts pipes and other things, shapes it. And, one lathe machine will have a sub motor. Say for example, 1 motor associated with that main machine. And, the presence of sub motor, that small motor is necessary in order to run the main asset also that is associated with. So in such a case, we can call it a sub asset. Say for example, 1 jeep is there and a trolley is there, always this trolley is associated with jeep. So jeep is main asset, trolley is a sub asset. Main machine, say, you take offset printing machine. Offset printing machines are huge machines and there’ll be some small, okay maybe, UPS stabilizer associated with it. So you can take stabilizer as a sub asset. Say, similarly, when fridge is there, a stabilizer is there. So that stabilizer is used for the purpose of fridge. So, sub asset is stabilizer, main asset is fridge. And, generally, what we do, even the rate of depreciation applicable is on main asset, subset both will be same. So, account determination, asset class, asset master, sub asset master. You have to have clear understanding of this classification before we go ahead with the asset configuration.

Then coming to depreciation. Say for example, on the land, we have 0 depreciation. Admin building, maybe 5%. Factory building, maybe 10% and plant and machinery, 15%, 12% like this. So we have to identify what is the rate of depreciation. Again, rate of depreciation as per the company’s act, as per the income tax act. In India, the rates of depreciation are different as per the Income Tax Act and as per the Company’s Act. Why is there a difference? Because the rate of depreciation is very high in case of Income Tax Act and, one more thing is the method of depreciation also depends. Again, we have different methods like, WDV method that is nothing but return down value method, straight line method. So depending upon the nature of depreciation, your percentage changes. But anyhow, we’ll see when we go to the chapter depreciation.

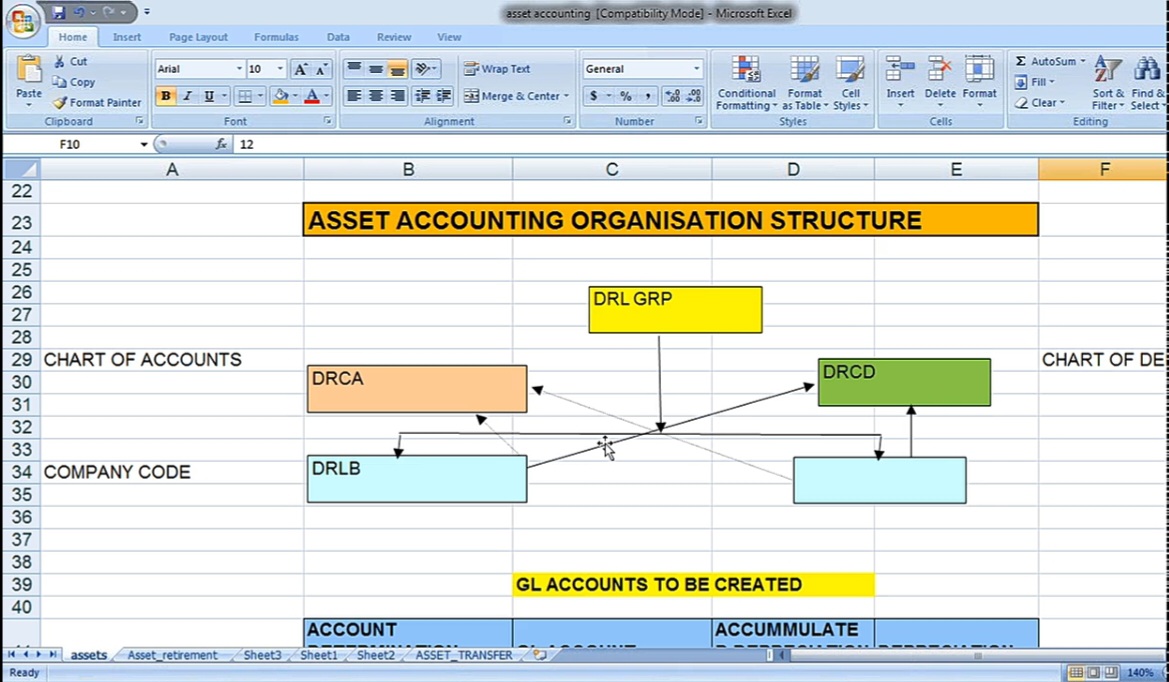

Then Asset accounting organization structure.

Whenever you are going to create asset accounting, the first and foremost step we have to create is the chart of depreciation. You know chart of accounts. Chart of accounts is client level, at high level this is. Client level means any number of company codes can use the same chart of accounts. We have the fundamental principles. For this, you need to read the documentation there in the IMG, against each and every configuration step I told you to go through that documentation. Apart from that, you can even read the SAP library. In SAP library also, you have all this information. So this is the group company. These are the company codes and I have this chart of accounts. Chart of accounts is higher than the company code, nothing but client level. And, similarly, I’m going to create one chart of depreciation that is DRCD, chart of depreciation. Just like chart of accounts, chart of depreciation. Now, what we have done here, each and every company code is linked to chart of accounts. Whenever any GL account is there, this GL account can be used by any number of company codes. But, there is a condition I told you, if you want to assign the same chart of accounts, the companies should have one more thing, better to have the same fiscal year breakdown. Similarly here in chart of depreciation. Fiscal breakdown means each and every company better to use the same financial year for the company. Say, generally, even under the group, whatever the companies that you are going to link up, I told you in the beginning itself, it is better to have the same fiscal year. Of course it doesn’t mean that we should not link up a company which is having another fiscal year variant. We can do it, but the thing is we cannot consolidate it because the periods will be different, years may differ. Here, we are using April to March and if the other company is using January to December, then that is different. You cannot club both. Similarly, in case a company is having a fiscal year like July to June, generally UK companies do that. So whatever it may be. But there are certain fundamental rules out there. We need to define chart of depreciation, that chart of depreciation has to be linked to the company codes. First of all, what is a chart of depreciation? We know chart of accounts. Chart of accounts is a chart wherein you’ll have all the GL accounts defined, which are required for the company codes. Any number of company codes can be linked to one chart of account. So like that, we have the chart of accounts. Now chart of depreciation is nothing but a chart wherein it holds different types of depreciation. Maybe depreciation as per company’s act, depreciation as per income tax act, depreciation as per the consolidation requirements, depreciation as per the group requirement. Something like that, I’ll show you. Once we go to the chart of depreciation, I’ll show you different options that will be available to you. But mainly, we use even depreciation for controlling area also, because I cannot use the same rate of depreciation, which I’m using for financial accounting. So that’s why as per my controlling requirement, I can have different depreciation methods. So like this, this chart shows you the group company, and company codes are here and chart of accounts and the chart of depreciation is also client level. Any number of company codes can be linked to one chart of depreciation. But provided the same chart of account should have been linked here earlier. And I told you account determination, asset class, asset master, sub asset master, all those things. Here, there are certain notes given here:

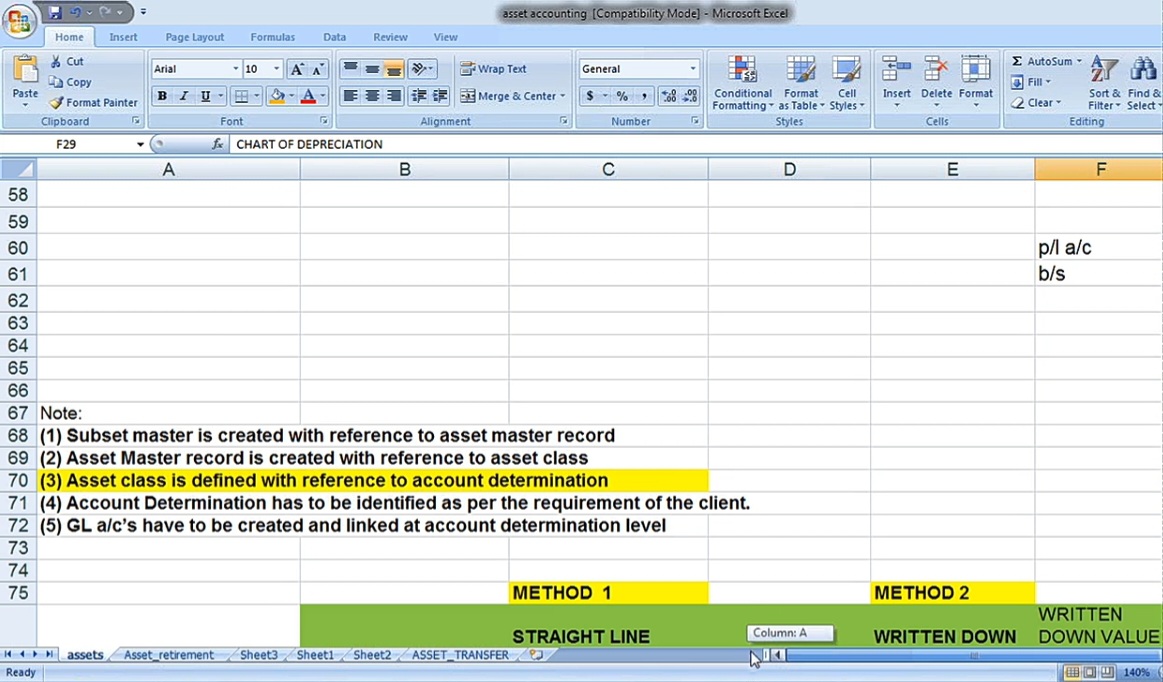

See here, sub asset master is created with reference to the asset master record. So whenever you are going to create a sub asset, it has to be created with reference to the main asset master record. Asset master is created with reference to the asset class. So whenever I’m going to create asset master, it has to be created with reference to the asset class. The exact meaning when we do the configuration, you’ll understand. But these are the things you need to understand here. Asset class is defined with reference to the account determination. So depending upon the account determination, I’ll be defining the asset class. And account determination has to be identified as per the requirement of the client. So whatever the main account determination, it will be defined with reference to the client requirement. GL accounts have to be created and linked at the account determination level. So here, we are going to create GL accounts at this level. Then at account determination level, we create the GL accounts and subsequently, what we need to do is we need to integrate those GL accounts with asset accounting. These things we’ll see next class. So, let us stop here with this introduction.