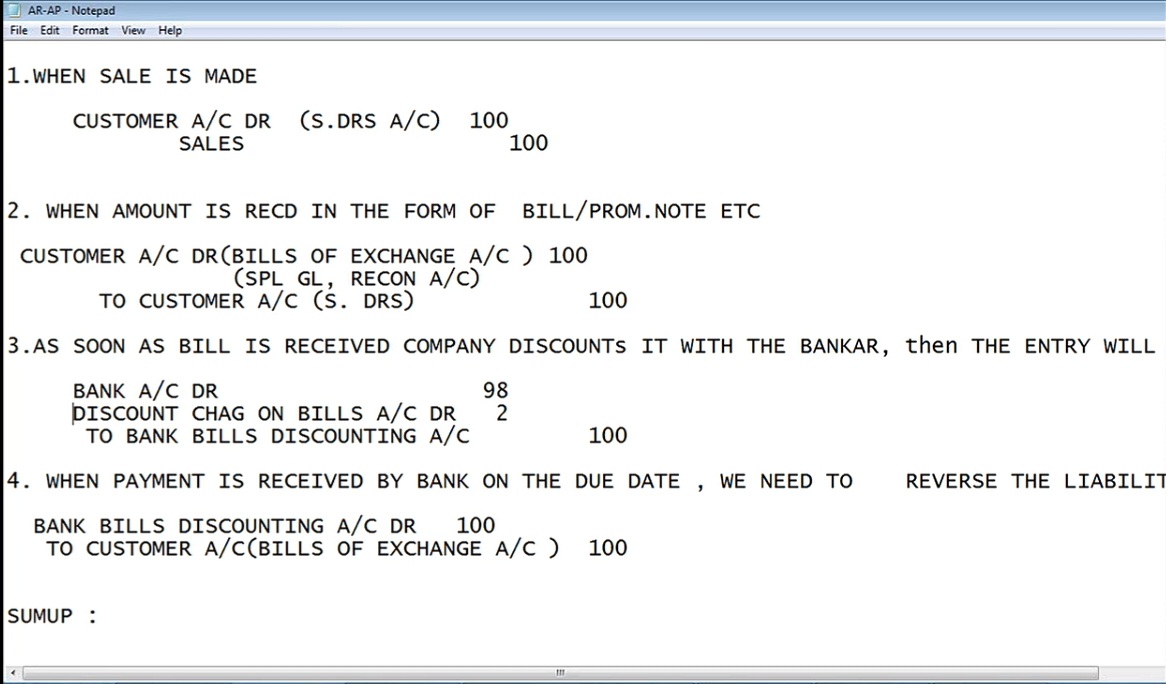

AR – Bills of Exchange

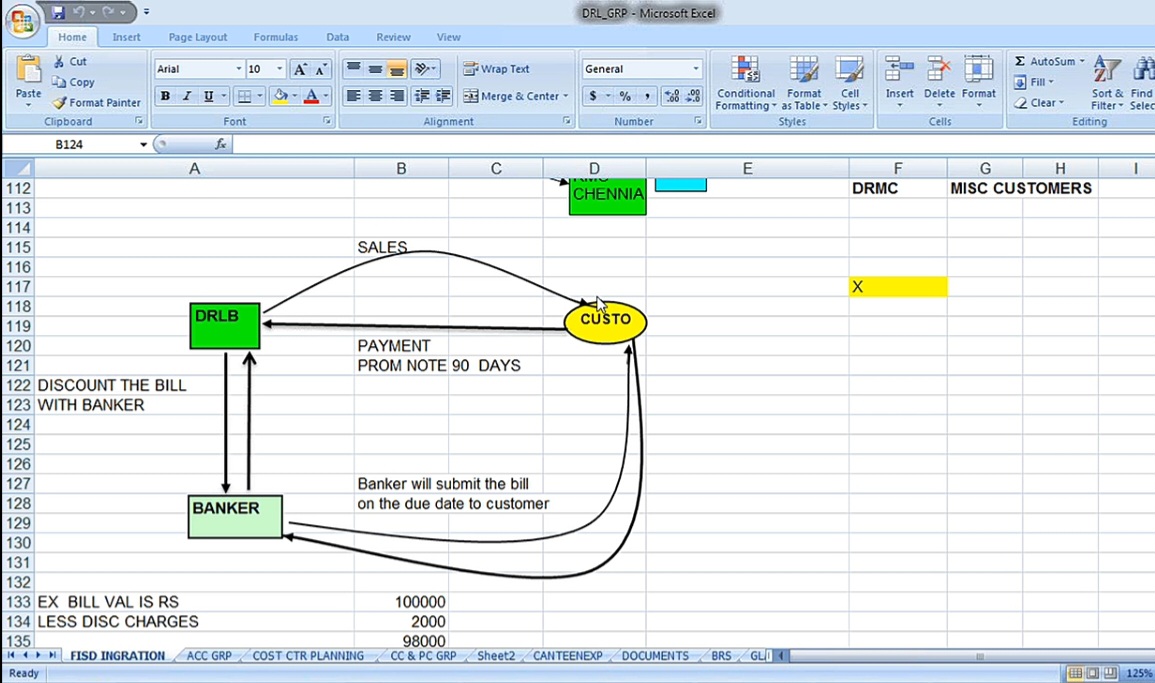

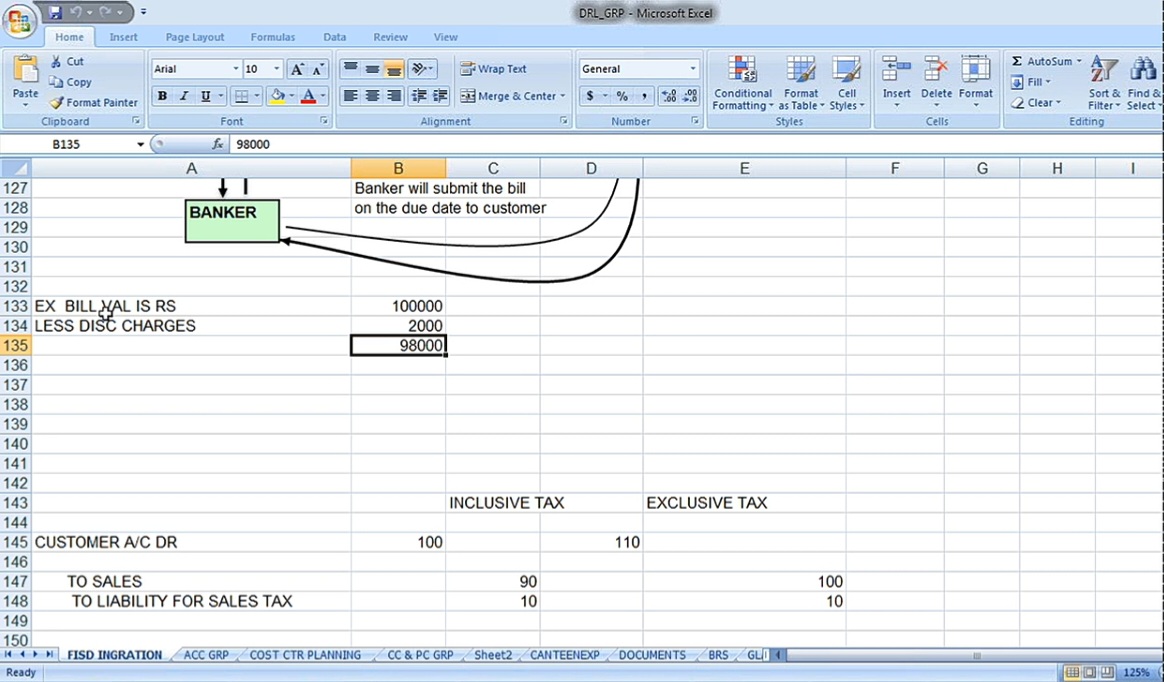

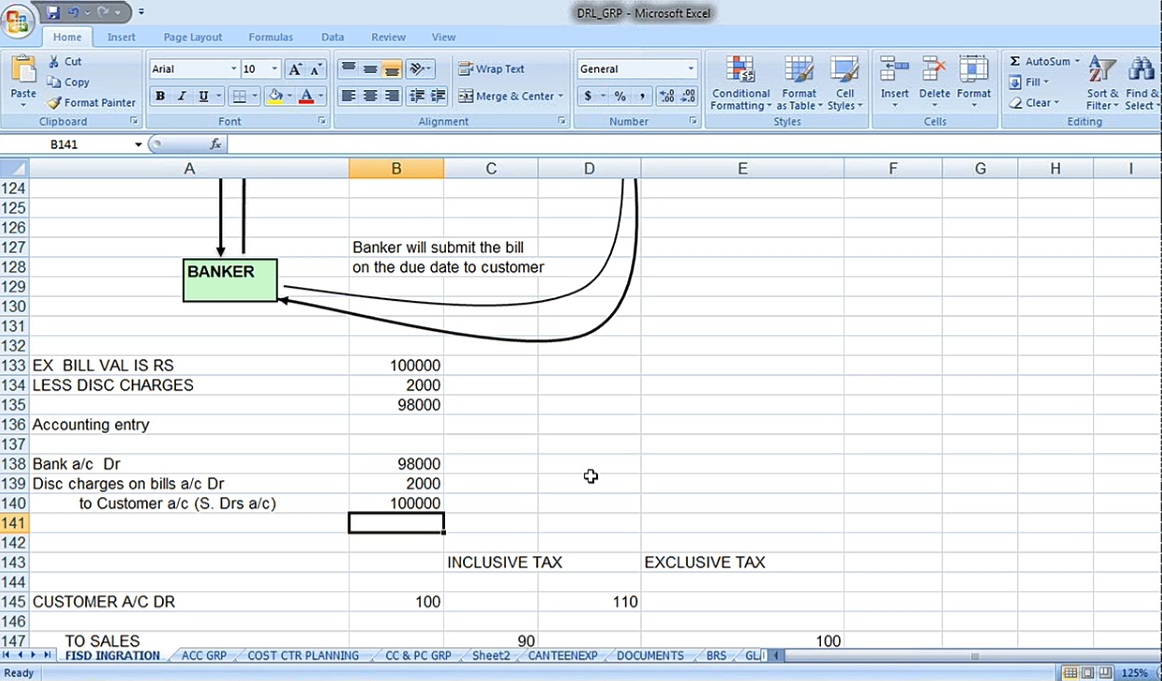

Here, company is DRLB, sale made to customer. And, when we make the sale, we’ll be receiving the payment, say, 90 days or 30 days, whatever it may be. And what we do as soon as we receive it, we discount the bill of exchange with the banker, and the banker gives me, out of 0.5 lakh, 2,000 he’ll keep. 98,000 is given to me. At the time, my accounting entry is going to be here.

Customer account will be created with 1 lakh. Bank account return, 98,000 and 2,000 is discount on there are some there is a discount, bill discount account. So here the accounting entry will be, since we are receiving cash, that’s why bank account, bank account return. How much we are receiving? 98,000, and discount is a expenditure for us. So discount charges on bills account return 2000 to customer account.

Right? So this is the accounting entry that will be posted. At every stage, we have, of course, accounting entries. We’ll see that.

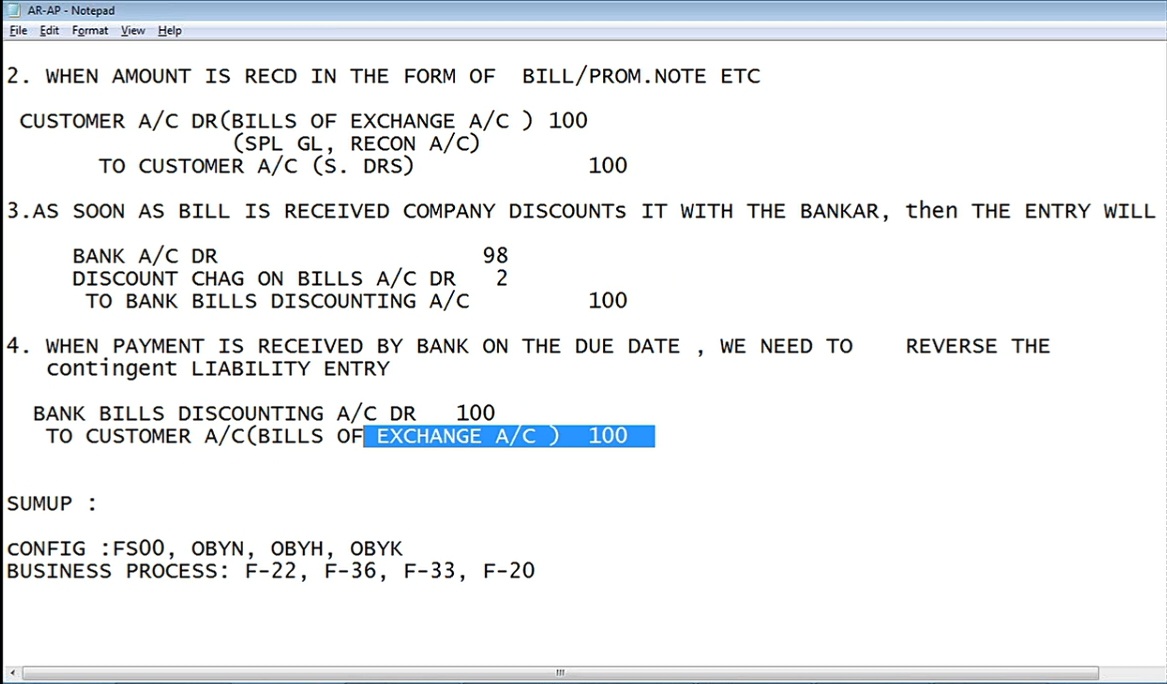

Say, when sale is made, say, bills of exchange, when sale is made, customer account return to sales, 100 rupees. When amount is received from the bill of exchange. When amount is received in the form of bill of exchange, customer account return to customer account because this customer account return because bills of exchange is going to be asset, current asset. This bill of exchange received from whom? Customer. So that’s why customer account return, bills of exchange account to customer account, sundry debtors. But because we have to credit the customer account. Special GL account is debited but regular customer account is credited. The special GL is debited. Normal GL is credited and here for the sale, this will get nullified. But since that fellow has given me bill of exchange, the amount is going to be due for after a 1 month until that 1 month or 90 days whatever it may be, his account is going to be, special GL account is going to be debited with bills of exchange. So as soon as bill is received, company discounts it with the banker, then the entry will be bank account data 98. Discount charges on bills account that are 2 rupees. 2 bank bills discounting account, 100 rupees. As soon as bill is received, company discounted with the banker. So bank account return, discount charges on bills account return to bank bills discounting account. What is this bank bills discounting account? This is nothing but one liability account we are creating because we are liable to bank until customer make the payment to bank. Remember that we are discounting their bill with the banker and until the due date, bank will not get the amount. In case, if the banker is not going to get the money from customer, we have to make the payment. So that’s why there is a liability for us. Here, bill of exchange is a current asset. We are showing it as an asset. And here, customer account will be debited with bills of exchange. So here in number 2, 100 rupees is being maintained as bill of exchange current asset. And here in number 3, this is going to be maintained as current liability. So my balance sheet tallies now. As per the accounting principles, bill of exchange is the current asset. That will be shown in the asset side. Same amount we are creating as a liability because we are liable to make the payment to banker in case customer fails to make the payment to bank. That’s why there’s a contingent liability. It’s a contingent. What is a contingent liability? Contingent liability is a liability which is going to be taken to the books of accounts based on certain future things to happen. So that’s why here, future thing is nothing but here, in case if the customer is going to dishonor the bill, then we have to make the payment. Until customer is going to clear, I have to show it as a liability. That’s a contingent liability. Right. When payment is issued by the bank on the due date, we need to reverse the that contingent reverse the liability entry reverse the contingent liability.

So bank bill discounting account. Here it is showing credit is debited. Customer bill of exchange account will be debited. Let us go ahead with the confirmation document now.

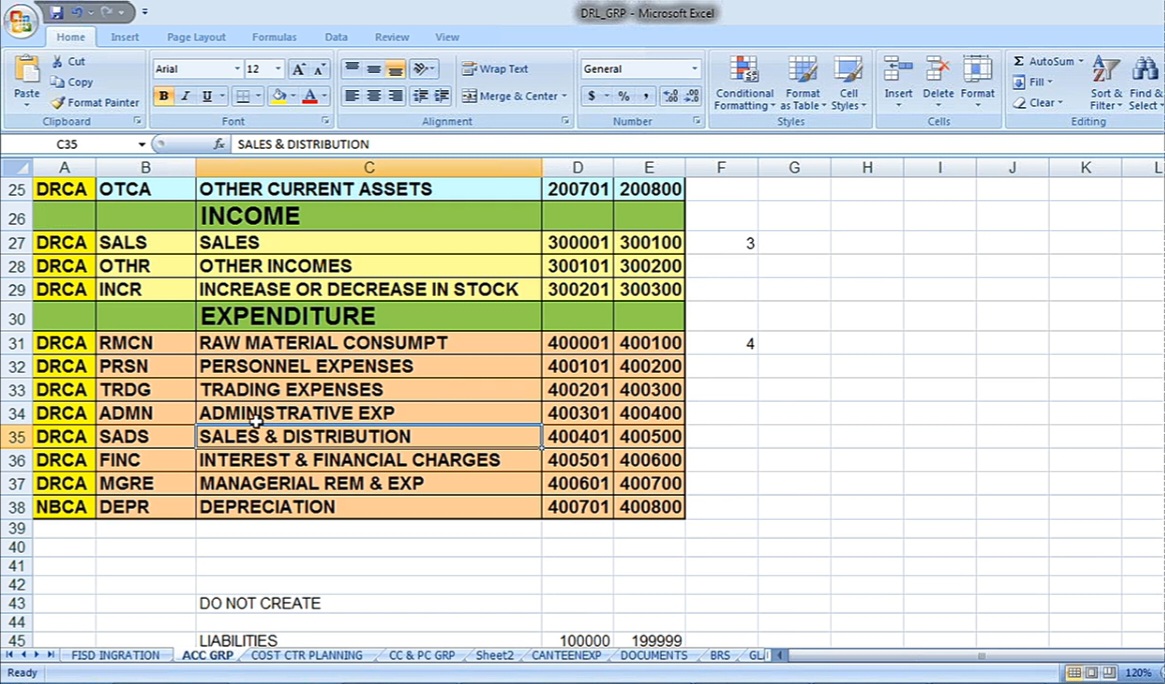

Now let us go for the configuration steps. Right here, we need 3 GL accounts, special GLs. one is bills of exchange account we need to create and discount charges on bills and the bank bills discounting account. Don’t get confused with these 2. Discount charges on bills is expenditure. Bank bills discounting account is a liability account. Just like a bank account we create. This is a liability.

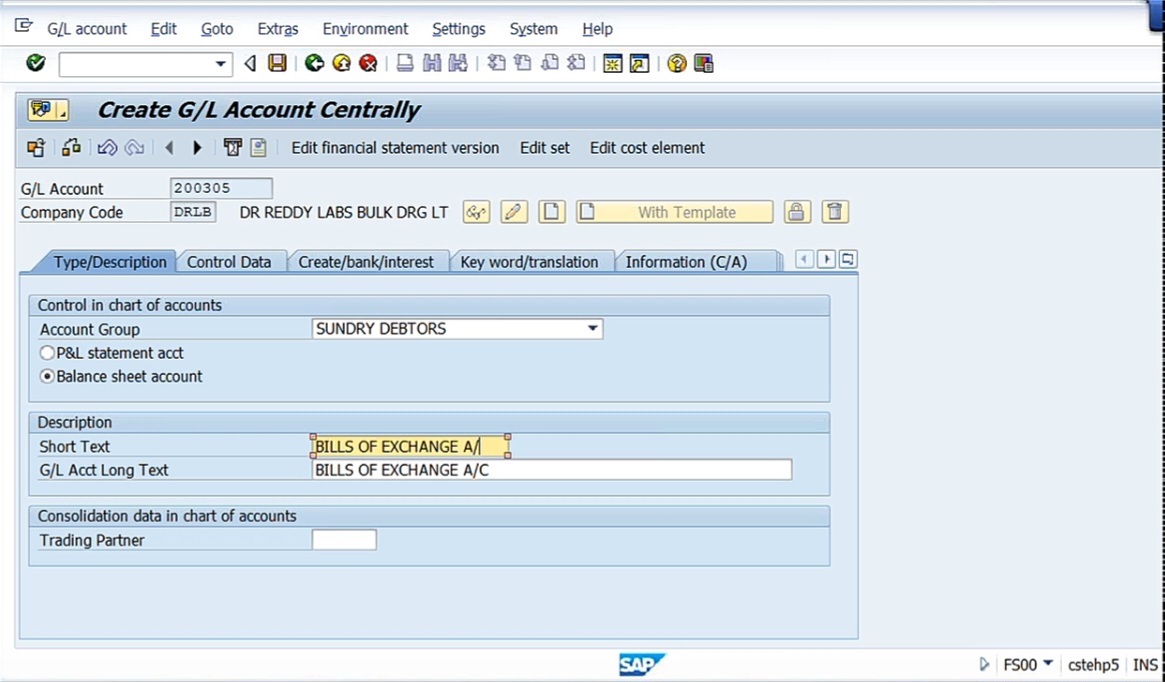

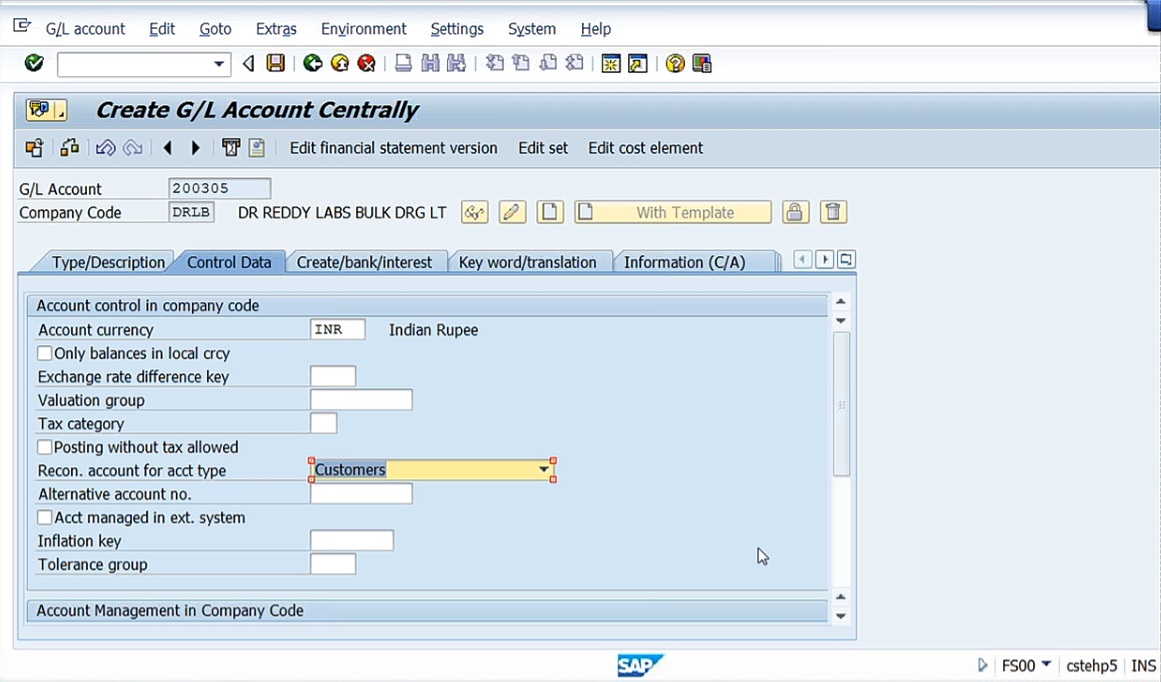

First of all, create GL account. Go to FS00. So in the sundry debtors, we have so many things are there. That’s why 200301 is given for sundry debtors. And, bills of exchange, I’ll take it as 20305. Account group is sundry debtors only. Balance sheet account.

Here, this is a recon account.

Bills of exchange because I can receive bills from different customers. There is a special GL account. This is going to be special GL and that to recon account. Recon account means I cannot post directly to this account. Sort key is 031.

Yeah. Since it’s a recon account, take G067 and save.

Next, discount charges on bills. So discount charges on bills mean nothing but see here,

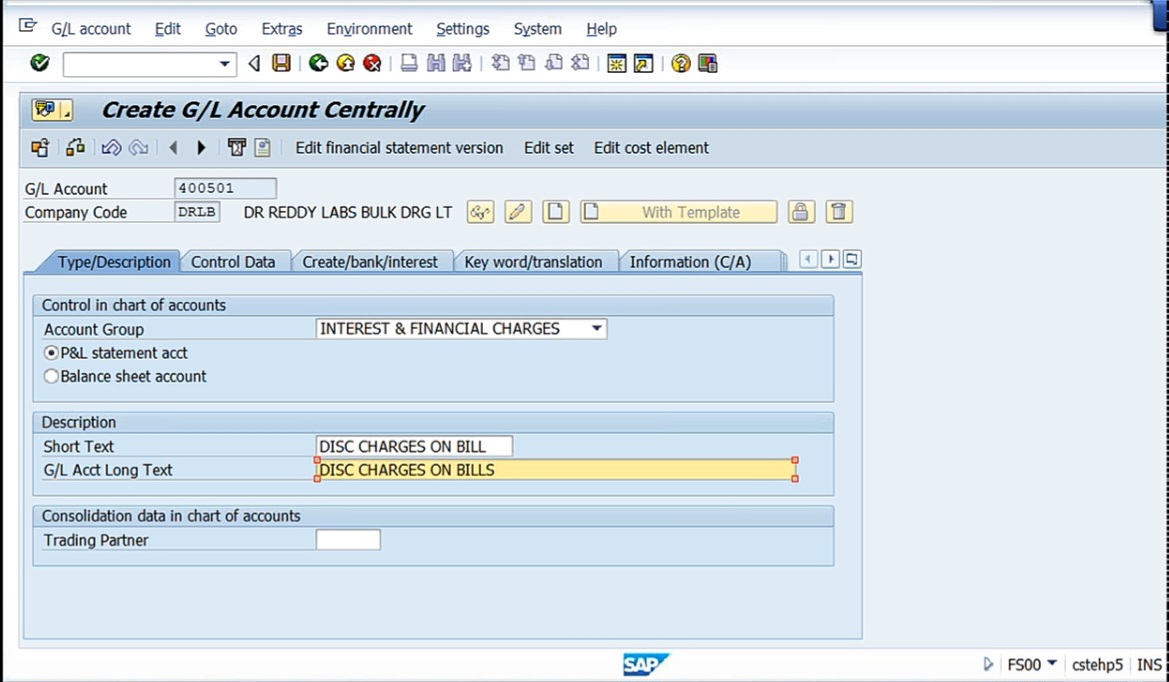

Discount charges on bills is a financial accounts financial charges. Here, we have here interest in financial charges. One thing is there here. I’m taking 40501. This is discount charges on bills.

Just take another expenditure account. 001 and G001. Create any number of expenditure account and capital bank account, other things.

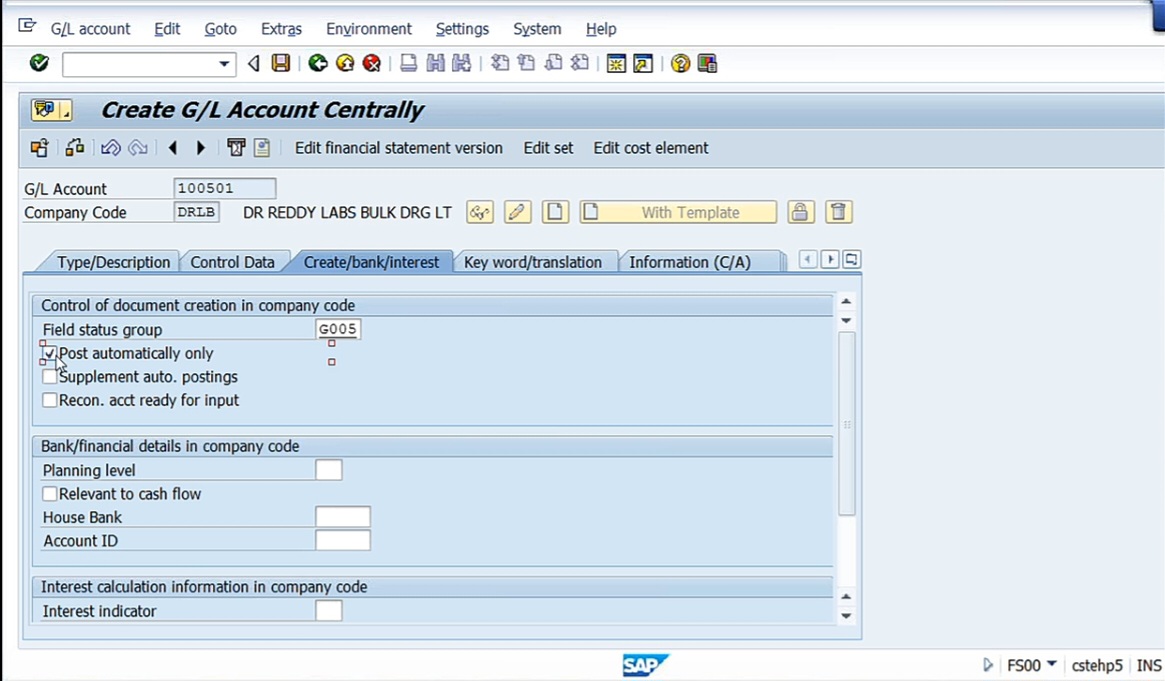

So the next is bank bills discounting account, and this has taken the other liability. Discount charges, bank bills discounting account, 100501. 100501 means Current liabilities. So current liabilities means okay, anyway, within 1 year, it is going to be cleared. That’s why we are creating in the current liabilities 100501. Click on create. And, here. Balance sheet account, bank bills discounting account.

There is some specialty for this account. Line item display, okay, 001. Apart from that, open item management, you have to check. In the Control Data tab, check the boxes open item management and line item display. What is open item management? Open item management is nothing but, see how to clear the open items we have seen. Open items clearing, we are manually doing it. In case of sundry debtors, whenever any amount is received, we clear the open item. But now, here open item management means here we are entrusting the job of clearing the open items to the system. By default, system will automatically clear the open items. Whenever the amount any amount is there, system will clear the open item with the exact amount if the amount matches etc., we’ll do it. Now let us see this. How it will clear open item and everything. And here, you can take G005 because it is equivalent to to bank.

And one more thing, post automatically only. For other accounts, we have not done this. Post automatically means we need not do anything. System posts automatically this one. So these are the certain specific requirements of this account. The special items what we have done for this is, here number one, operator management we have checked it and and post automatically only. These 2 are special here. So 3 accounts we have defined.

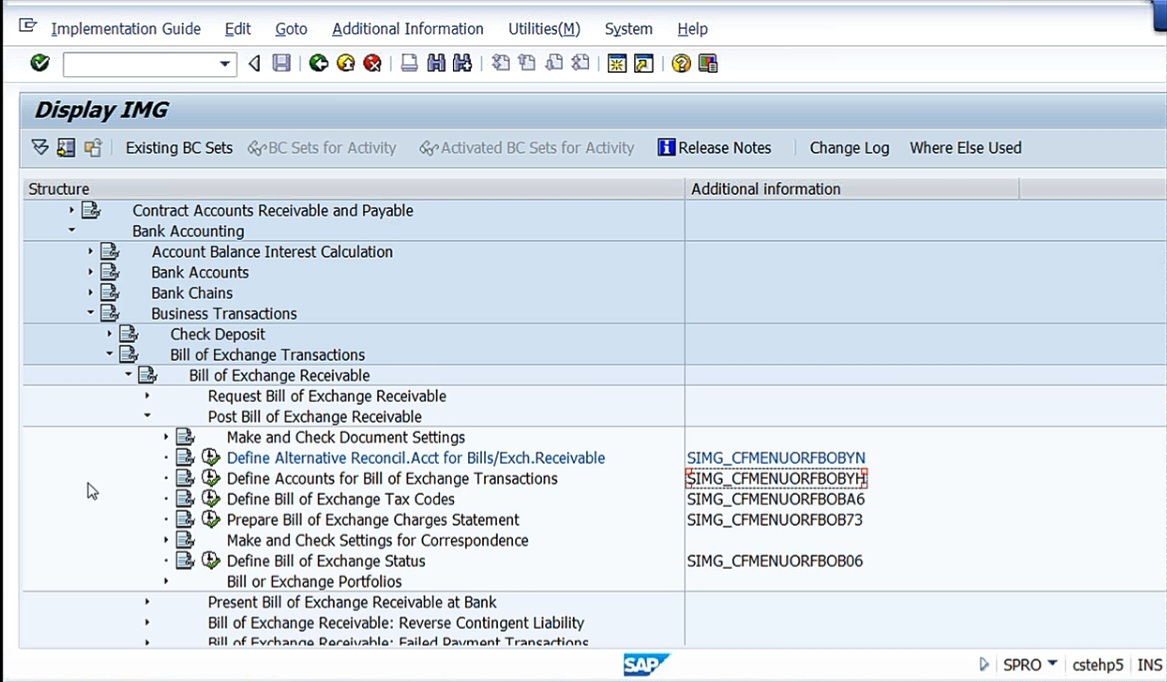

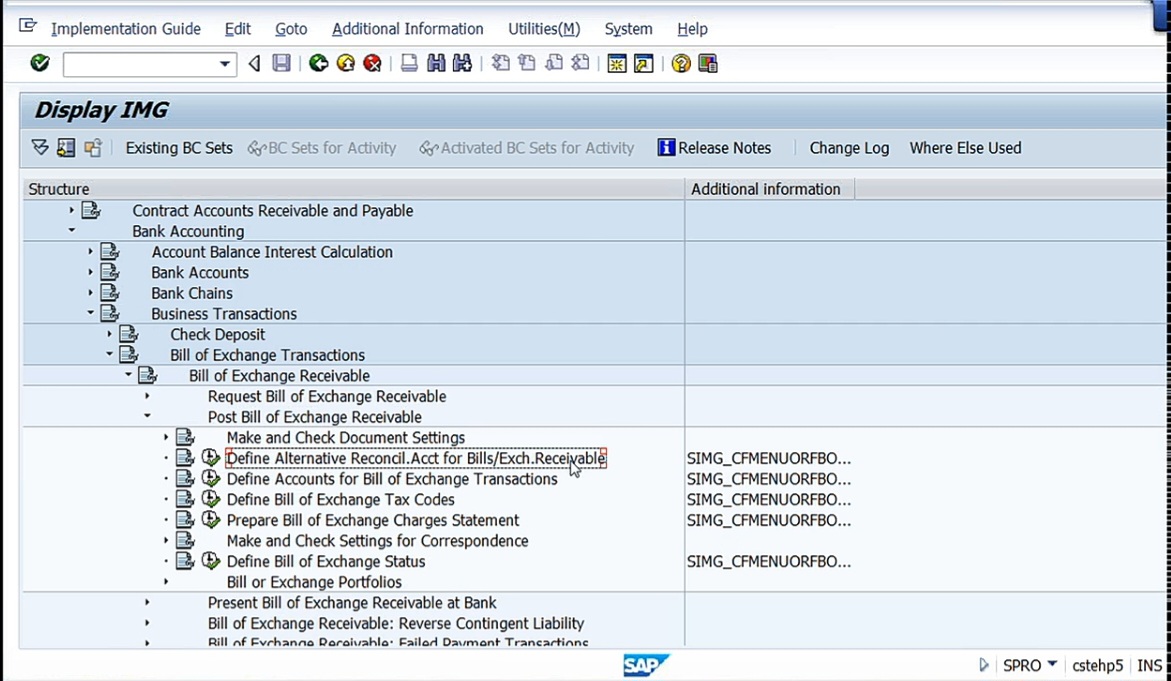

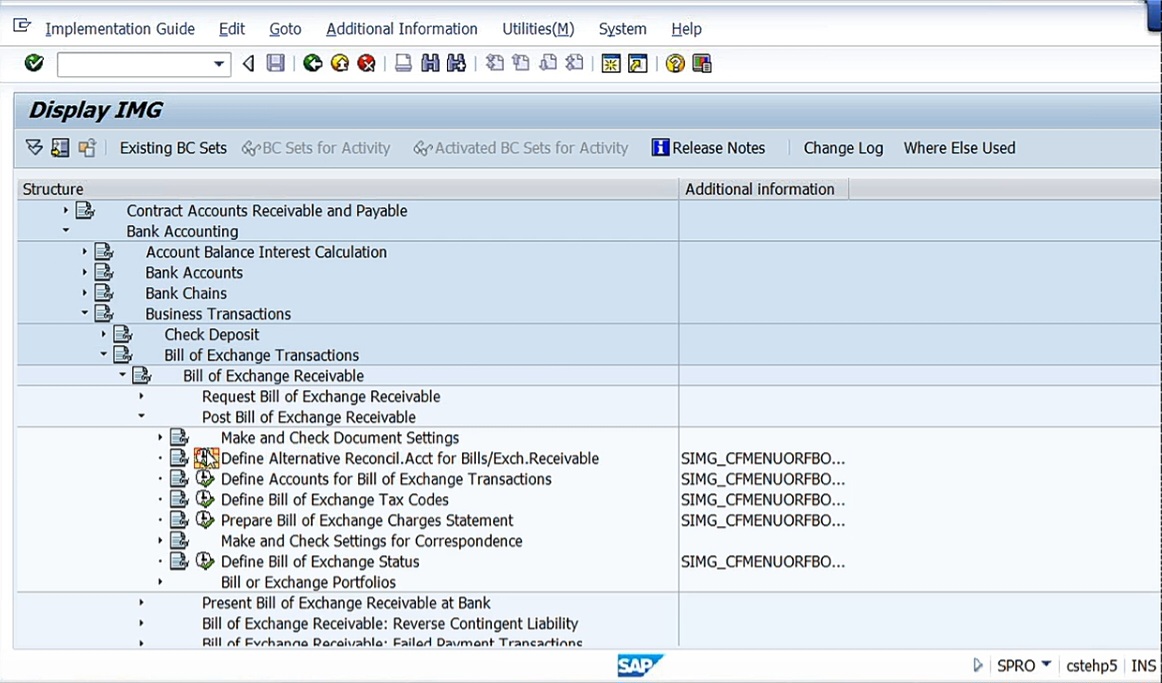

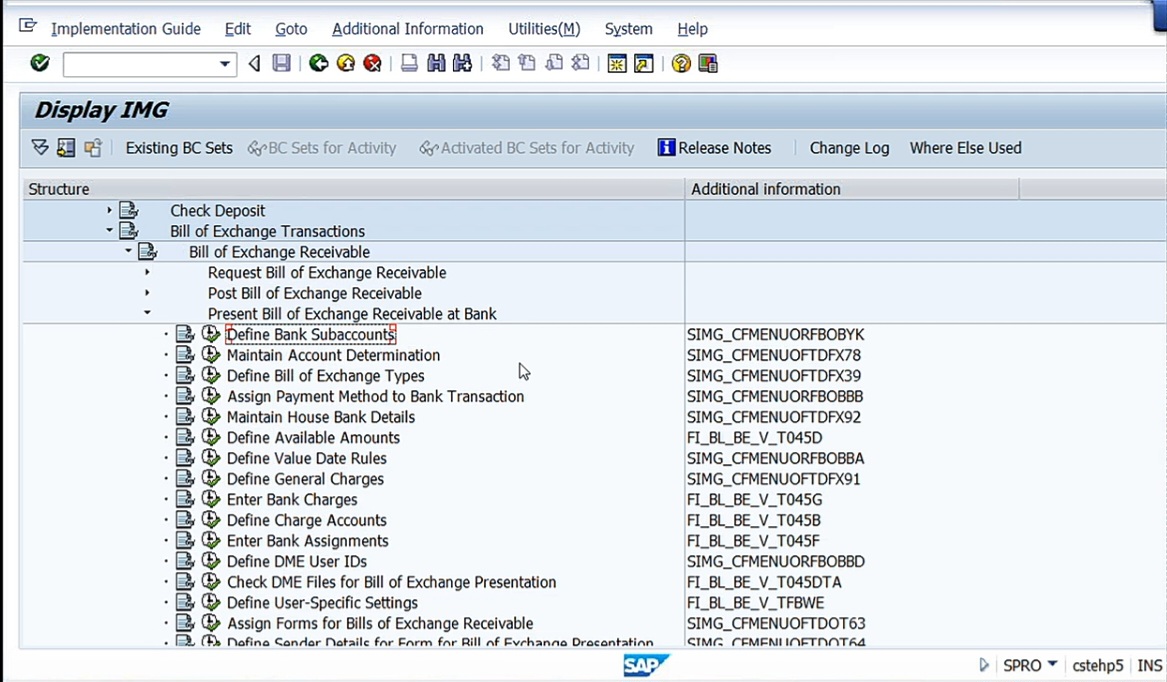

Now let us go for the configuration. Now here, step number 1, Financial accounting, (New), Bank Accounting, Business Transactions, Bills of exchange receivable, Post bills of exchange receivable, Define alternative reconciliation account for bill server exchange visible.

Now, here what we are doing, customer account return to bills of exchange. So now what we need to do, whenever we receive any bill of exchange, right, it should go to bills of exchange account not to sundry debtors. Here, because by default, whenever we post an entry to customer, it will go to sundry debtors, but in this case, I don’t want this to go to sundry debtors, I want it to go to bills of exchange account. So for that purpose, just like advanced account, how we have done that confluence one configuration step, so we told the system, in case if I choose A, you post not to this sundry debtors, rather it should go to advanced from customers. That’s what we have decided. Similarly here, now if I’m going to use special GL indicator W. Here the special GL indicator is going to be W. Then system will understand if W is used, system thinks this is bills of exchange. So then in such case, it will not post to sundry debtors, rather it will post to bits of exchange account. So this configuration step, we need to do it now.

Define alternative reconciliation account. Why alternative? Because original account is sundry debtors, by default, it will go to sundry debtors. Now alternatively, it should post to bills of exchange account.

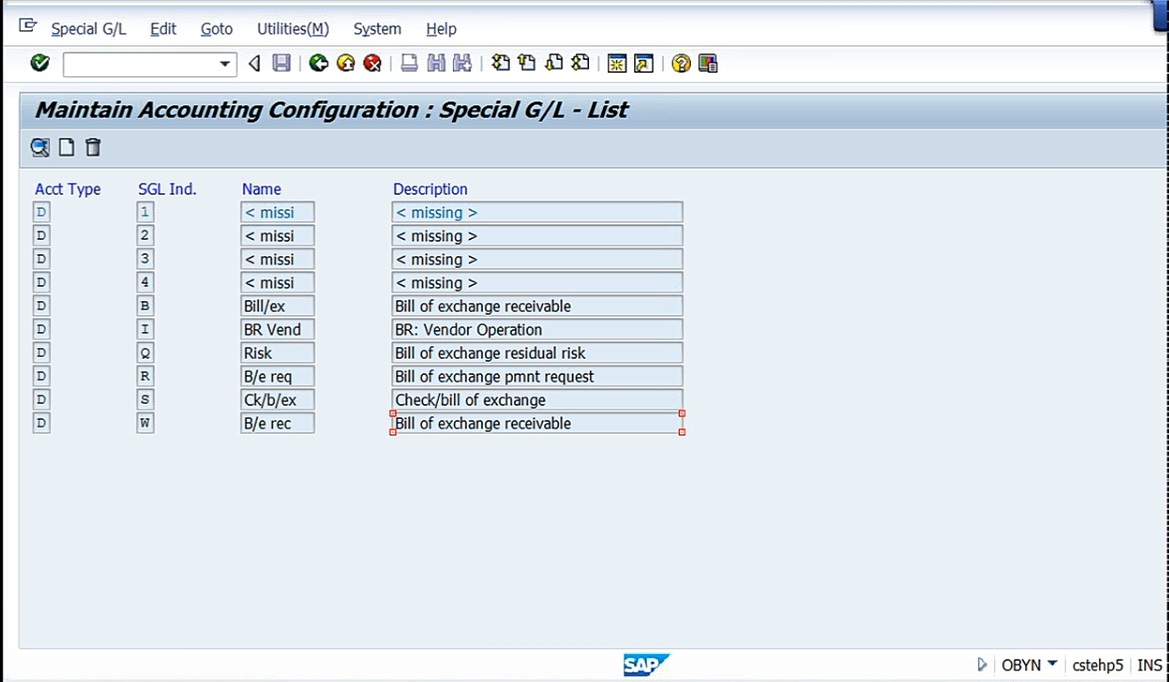

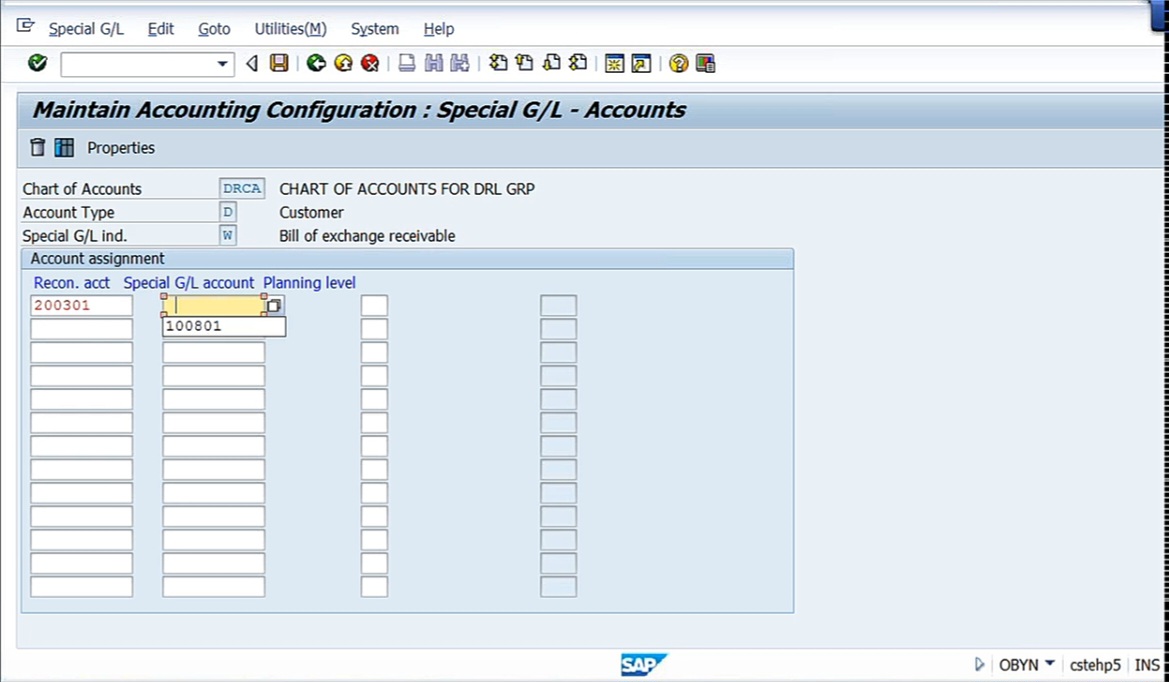

Right here, w d w, bills of exchange receivable. Right. There is a bill also here, b. But don’t post it here because by default system picks up W. If you want to use this, it also can be used. But you need to make certain changes at the time of posting. So that’s why what we do, bills of exchange receivable, double click here. DRCA is my chart of accounts. Recon account 200301, that is sundry debtors account.

In case if this is, 200301 sundry debtors, if W is used, 200305 bills of exchange. In case if Wis used, don’t post to sundry debtors, rather, it should post to bills of exchange account. Come back.

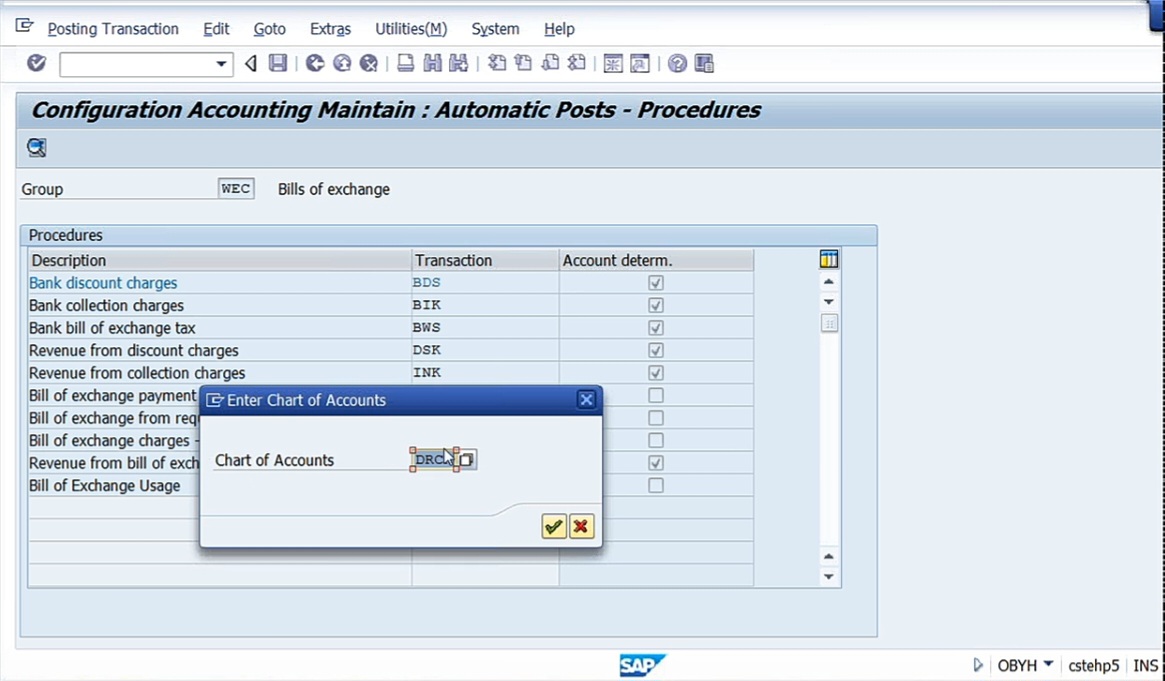

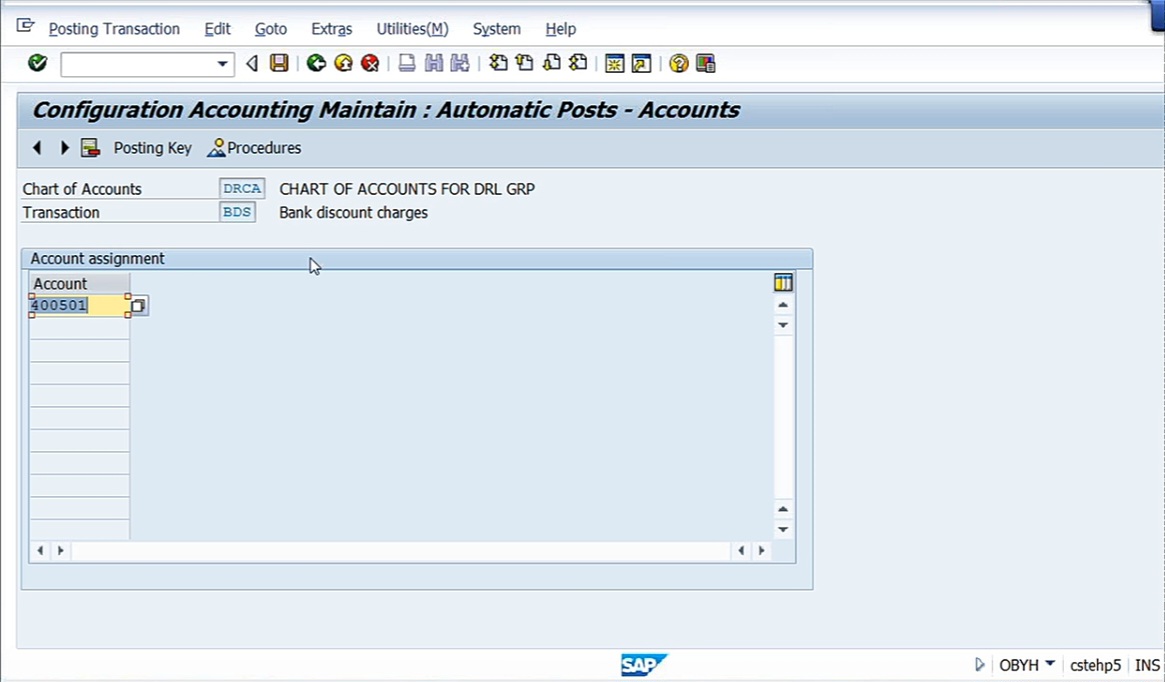

Define accounts for bills of exchange transactions. OBYH. This is for the purpose of bank discount charges. Whenever any discount has to be posted here, bank account return, discount charges on bills. System automatically post to that field. There is a one field, against that field, we’ll just put the amount. That’s all. Accounting entry will be generated by system. For that purpose, bank discount charges, BDS.

Double click on it. Chapter of accounts DRCA.

Here, that is discount charges on this. 400501, take here. Here everything is going to be automatically posted, accounting entries.

We’ll see now. Save it. See here BDS is nothing but a transaction key. We call it as a transaction key. For everywhere, wherever there is a transaction key, it should be linked to a GL account that will be automatically posted. Transaction key BDS. Come out.

Present bill affects a receivable at bank. One more confirmation step we need to make. Define subaccounts. Here define subaccounts means, see, this accounting entry posting to bill subaccount, bank bills discounting account And reversing of this entry, all these things will also will be posted automatically. All these entries will be generated by system. We need not post. For that purpose, we need to make certain automatic setting of these accounts.

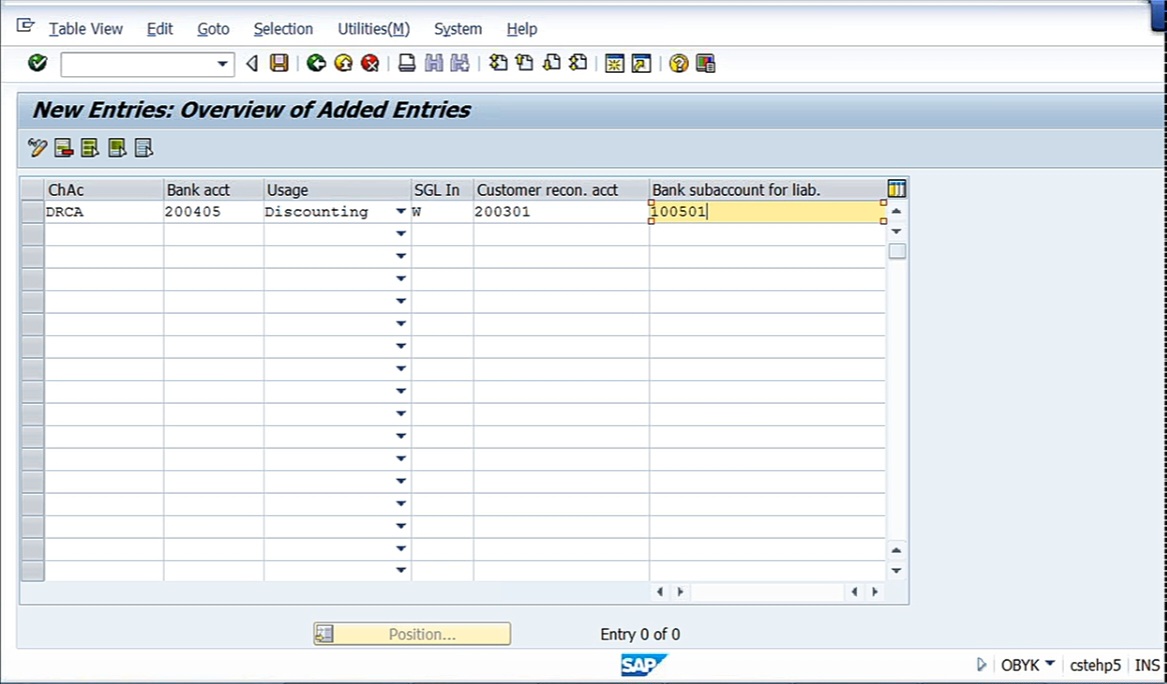

Define bank subaccounts. OBYK is the t code. Here, what we need to do, So here, go to new entries, chart of accounts, DRCA, My bank account, 200405. Usage, discounting. See bill of exchange, we are going to discount it. Discount and special GL indicator, W. Customer recon account that is 200301, is my sundry debtors account. And here bank subaccount for liability, that is 100801, that is bank bills a discounting account. Bank of 100801 advanced loan customers. Bank bills a discounting account.

Here in chart of accounts, DRCA, my bank account is this. Customer recon account is 200302, that is sundry debtors account. Customer recon account means always sundry debtors account and bank bills discounting account here. Why we are going to give all these accounts here means because I need to get these accounting entries. These are the accounting entries I require. This is my business requirement, not SAP requirement, this is purely business functionality. Business requirement, not SAP requirement. Forgetting this one, SAP has developed the program in such a way that, okay, you need not manually put all those I mean, pass all those entries. You do this confirmation in this chapter accounts. You assign bank account, and this is going to be used, the bill of exchange is going to be used for discounting purpose. In such case, it’ll be affected. What are the GL accounts that are going to be affected? Right. 200301 from sundry debtors and bank bills discounting account. Assign these accounts, and I’ll come back to this table again once I post the accounting entry and I’ll tell you how system has generated the accounting entry. But you need to follow this configuration. So 3 steps we have done. Bills of exchange receivable, post bills of exchange receivable. This is alternate reconciliation account. Instead of 200301, 200205, we have given that. Here, to post to the financial charges, discount charges, we have assigned the GL account here. And here, we have assigned that is the liability account, sundry debtors account and bank account. Why I need to assign? That we’ll see once we post the accounting address. So this is the 3 steps we have to do the configuration. First step is creation of GL accounts. Next 3 are configuration steps.

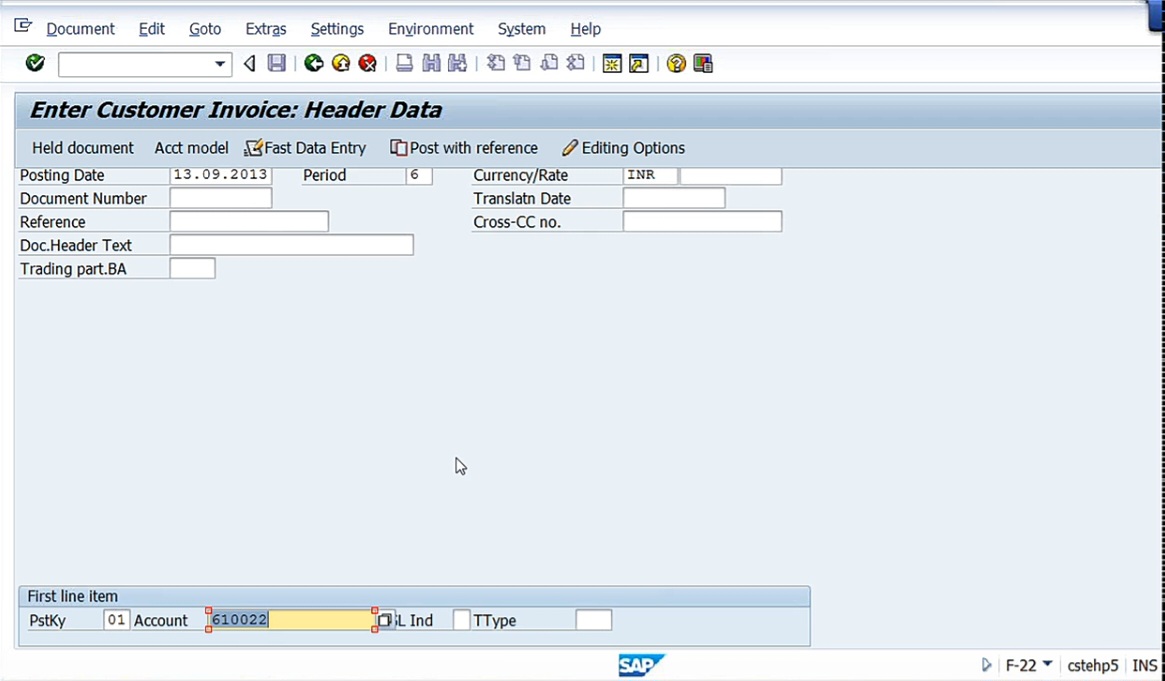

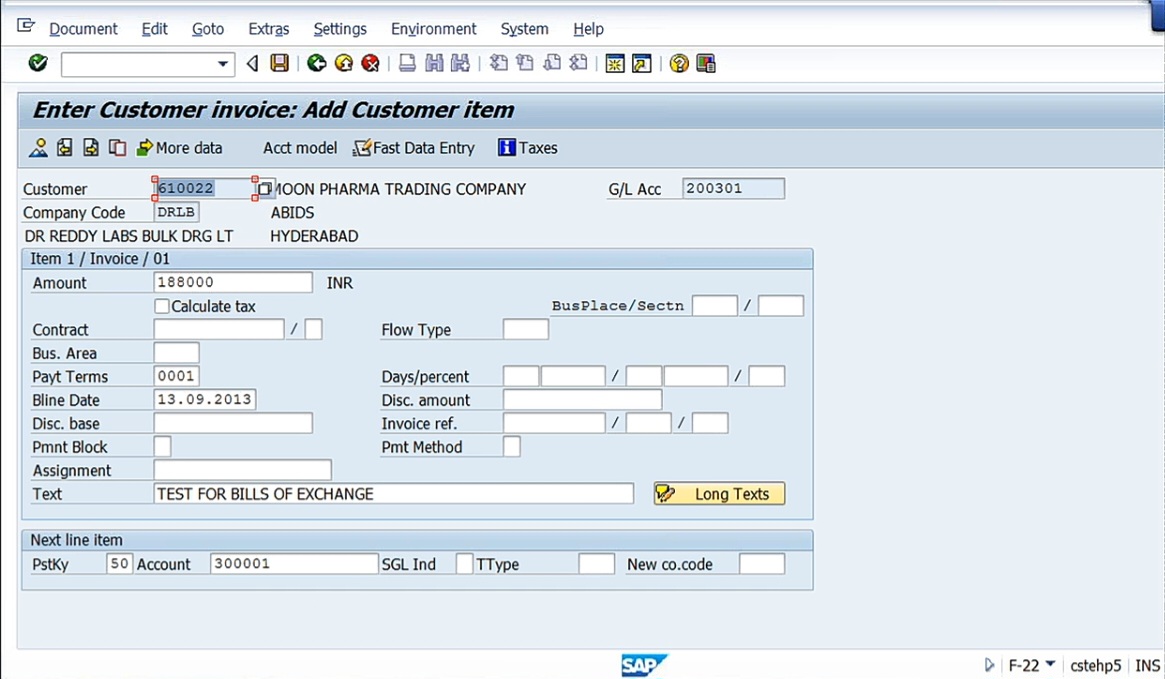

Let us go to the business process entries. So most of the SAP configuration is based on the client requirement. So first of all, we need to understand the client requirement. So that’s why I have explained to you, yeah, this is the business process scenario. And this process scenario is mapped that is configuration has been done like this. Understand the scenario, configure the steps, then follow the business process. So what is the business scenario? First of all, let’s post the entry for sales. So whatever the bills of exchange that everything is configured is done. Let us follow the process. Now I’m sitting in the position of, say, an accounts officer. First of all, what is that we do first? Number 1, make the sales, post the entry for sales. Then after the sale, we receive the bill of exchange. Afterwards, we discount it. Afterwards, we reverse the contingent liability. Say document entry. First invoice, F-22, I’m posting.

This is sale. Nothing is new here. Say, 1 lakh 88,000 I’m taking. Test for bills of exchange. 50 sales. And, 3 lakhs, one is sales account. Customer account data up to sales.

See, first, whenever I have taken by default, system will take 200301 from sundry debtors account. Save. Nothing new here. Once sale is made, so that fellow gives us bills of exchange. Instead of cash, I receive negotiable instrument.

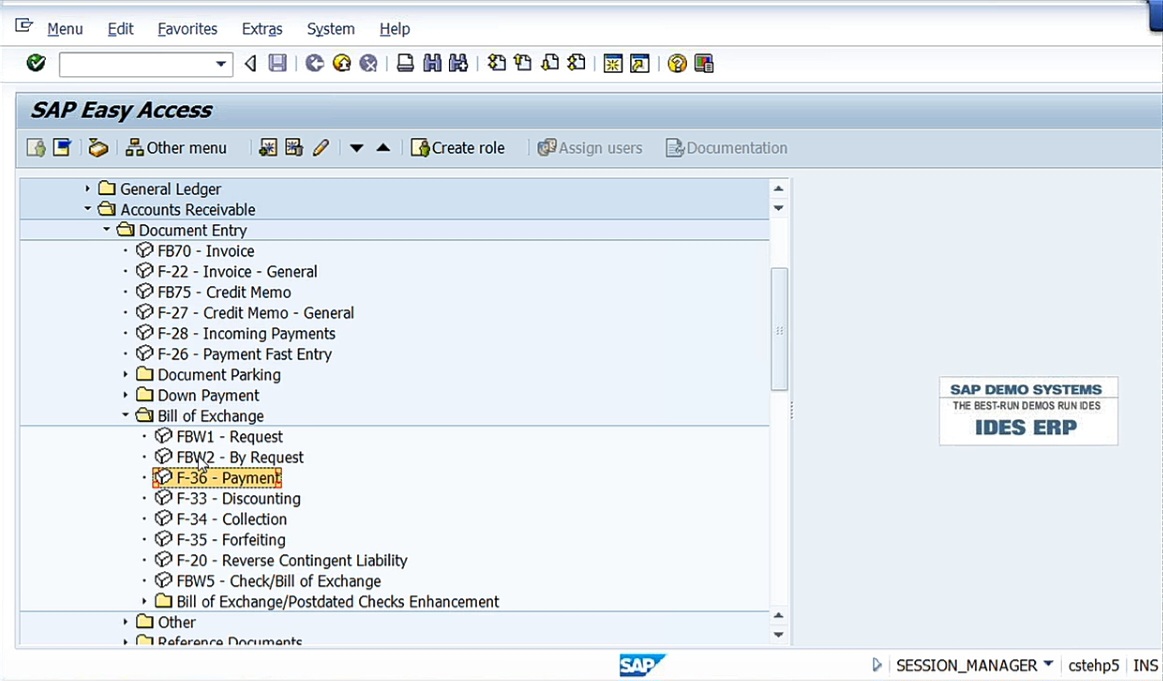

Go to bills of exchange here.

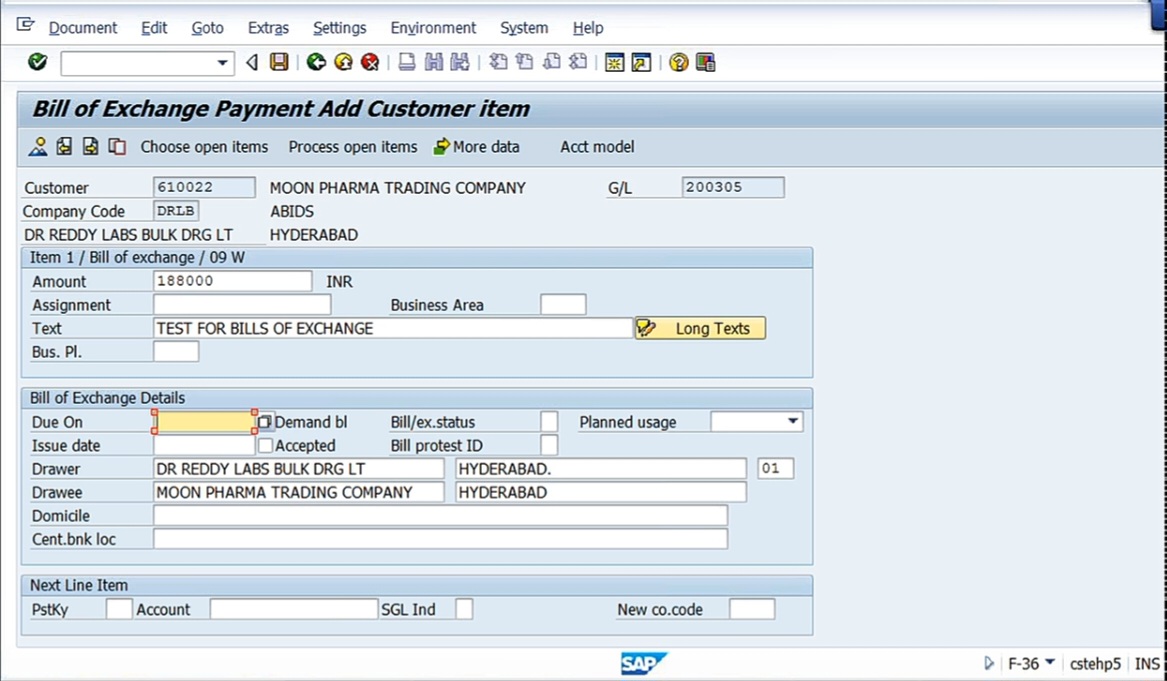

Payment. Payment means payment made by customer, F-36. Also I told you that in case of bills of exchange, there’ll be a drawee and drawer. The person on whom the bill has been drawn is called drawee, and the person who receives the bill is called the drawer. Right. Incoming transaction to be processed, incoming payment. Posting key 9. Special deal indicator by default, it is given as W.

That’s why I told you to take up W. That’s right, Moon Pharma. Because that fellow, we made the sales to Moon Pharma. That’s why we have. Now bills of exchange has been received from this Moon Pharma. Press enter.

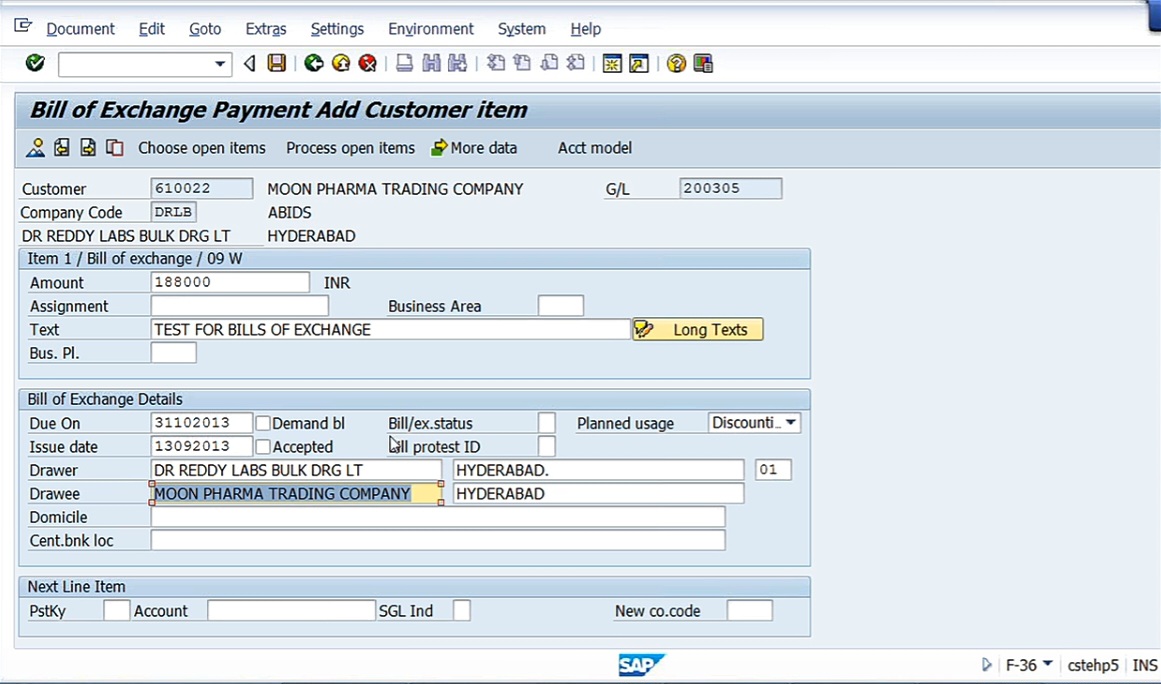

So here, amount. 1 lakh 88,000. Test for bills of exchange. This bill is due on, say, for example, today 13th, we have received it. And, let’s imagine that is a 45 days bill and this is September. October ending on 31st/10/2013, this is due. Issue date, today’s date 13/09/2013. Planned usage. We are going to discount it. Discount. Drawer DR Reddy Labs, Drawee Moon Pharma. By default, system has taken. We have not done anything. Because system knows that who is the drawee, who is the drawer. So because the company is the drawer and the bill has been drawn on Moon Pharma that’s why it is called drawee.

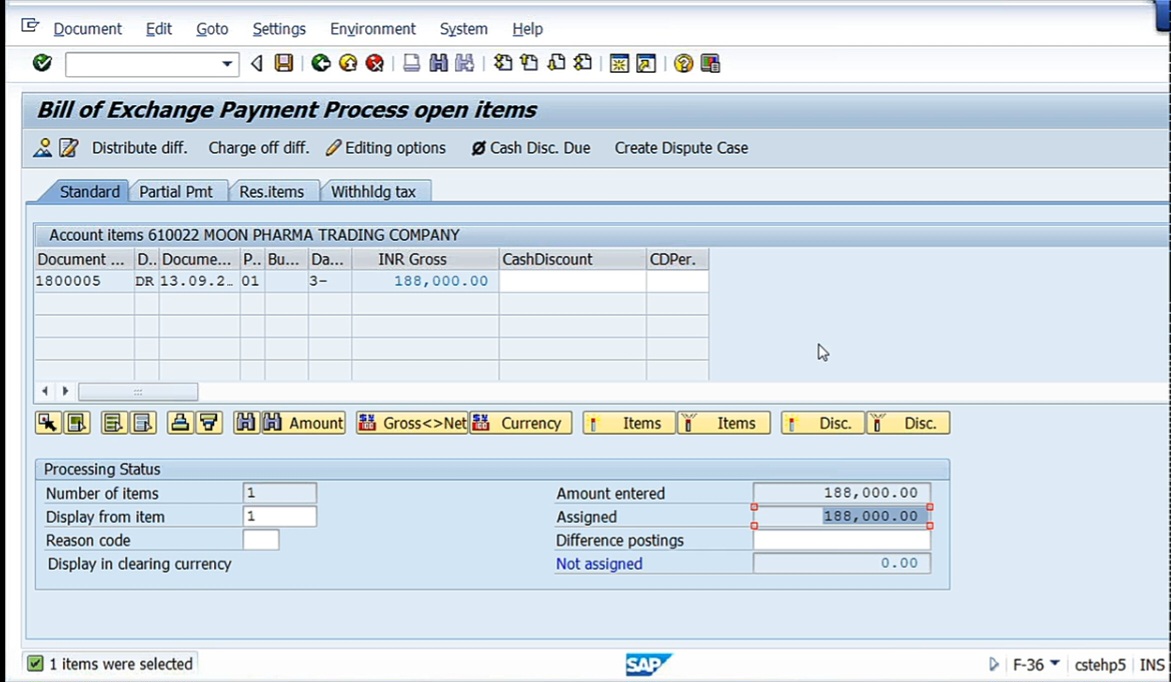

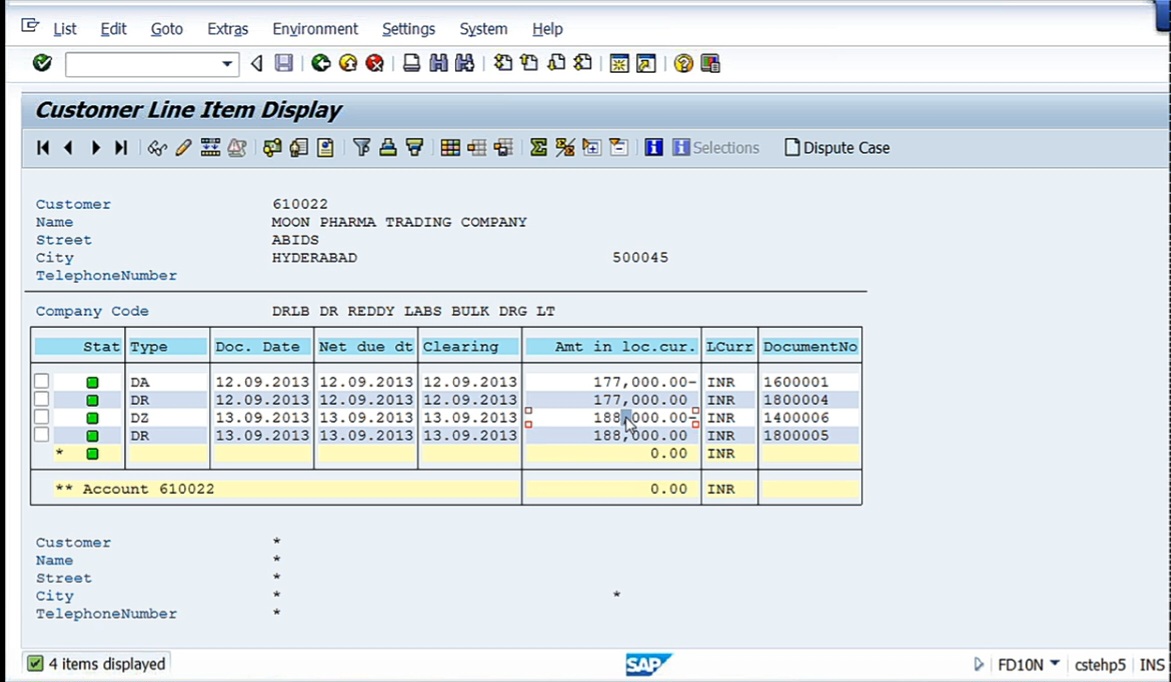

Once you complete this, how we have cleared the open items in case of F-26, the same way choose open items. First of all 1,88,000 we have received. I need to process the open item. I need to clear the open item. So for that purpose, let’s go to Choose the open item. Here, just click on process open item. 1 lakh 88,000, 1 lakh 88,000. If you have any other line items here, just double click deactivate.

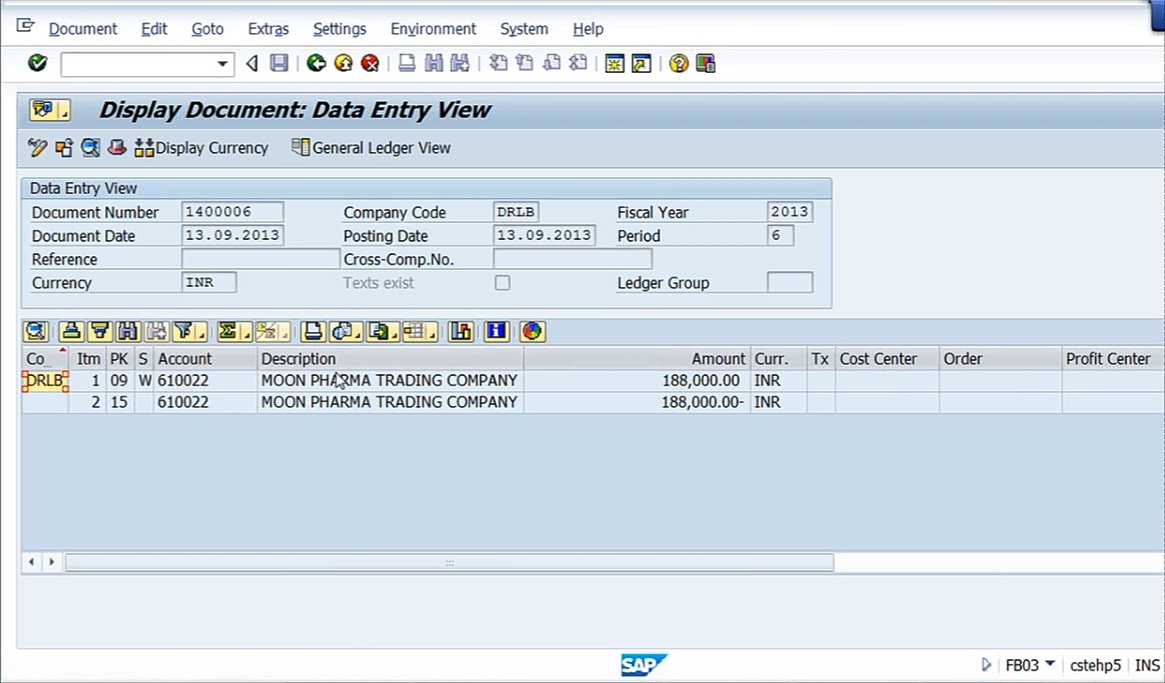

Now I can save it. Once we save, what is the accounting entry we expect as soon as bill is received here? When amount is received in the form of bill of exchange, customer account return to customer, but recon account will change. Save it. Document 14 lakh 6 has been posted.

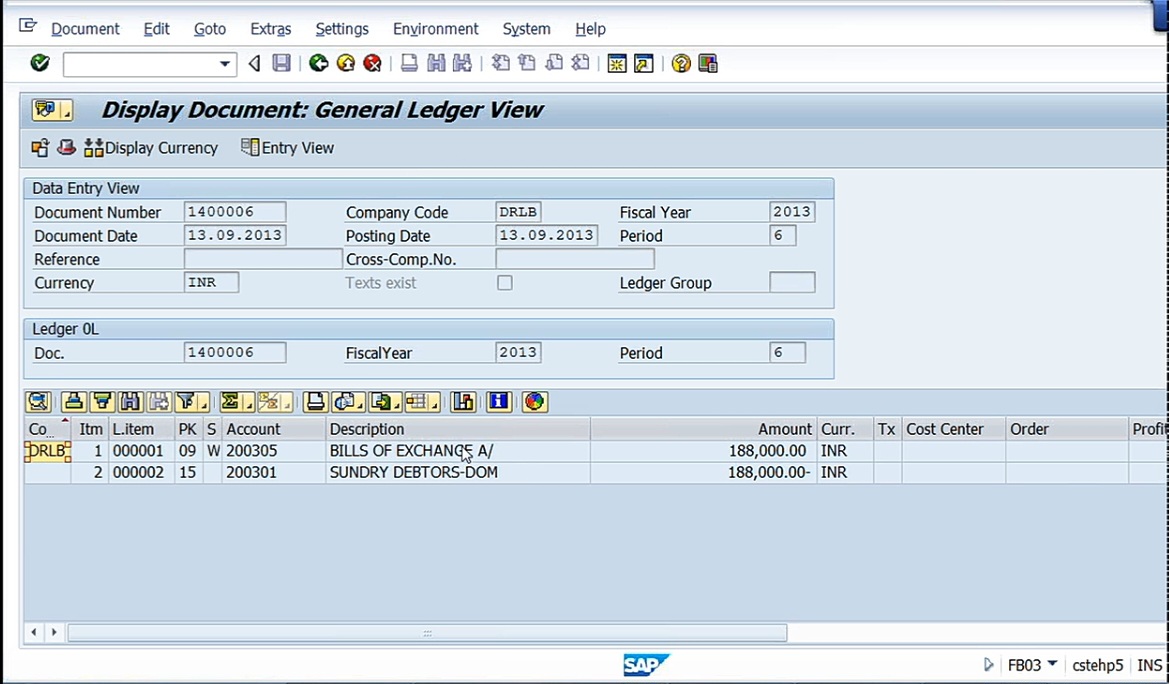

Look at the document. See. Customer account is debit. Customer account is credit. Then what is the respective GL account system has posted to? Look at the general ledger view.

Bills of exchange account is debited and sundry debtors domestic is created. This is what we wanted. Because bills of exchange is a current asset, that’s why it has to be debited. And Sundry debtors, we have received the payment, that’s why we have cleared the offer item.

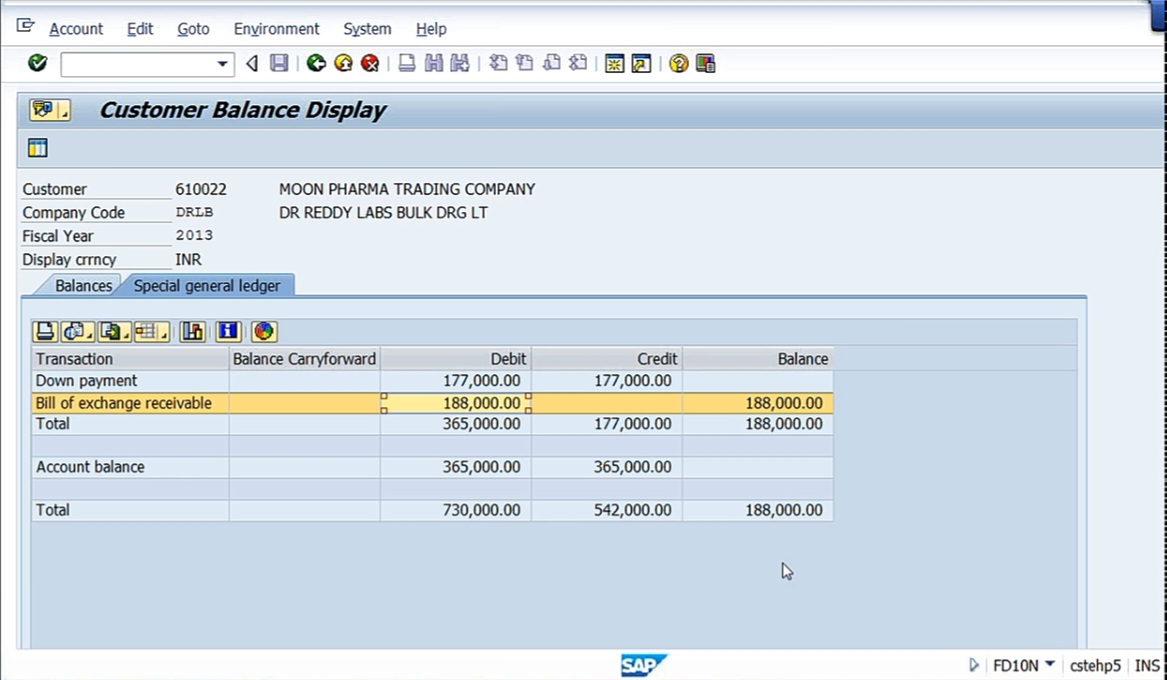

Now let us look at the party account. See here, we have all the posted advances that will not have an effect.

Special GL, see, 1 lakh 88,000. 1 lakh 88,000, it is showing the debit balance. 1 lakh 88 debit balance is being shown as minus. Debit side.

And here, 1 lakh 88,000 already cleared because we have cleared the open item with bills of exchange then the special gl account is showing debit.

When sale is made, customer account returned to sales. So customer account is showing here debit balance. With bills of exchange, we have created it, customer account, sundry debtors. So here this 100 this 100 gone, open item has been cleared. But system generates another line item with bills of exchange in the special GL as debit. So that’s why here in this case, this has been already created. So here, debit, 1 lakh 88. Credit, here, 1 lakh 88,000 also. So this has been cleared with bills of exchange, whatever is received. But one entry that, like bills of exchange account will continue to show as a debit balance in this special GL. Because this customer, he’s not relieved from his responsibility of making payment to bank, so that’s why his account continues to show as a debit balance. And, if you want to see what is the GL account? How can we see it in FS10N. GL account 200305.

See, debit balance. In the special GL there, it is showing 1 lakh 88. Here, debit balance is showing current asset. Bills of exchange is showing 1 lakh 88.

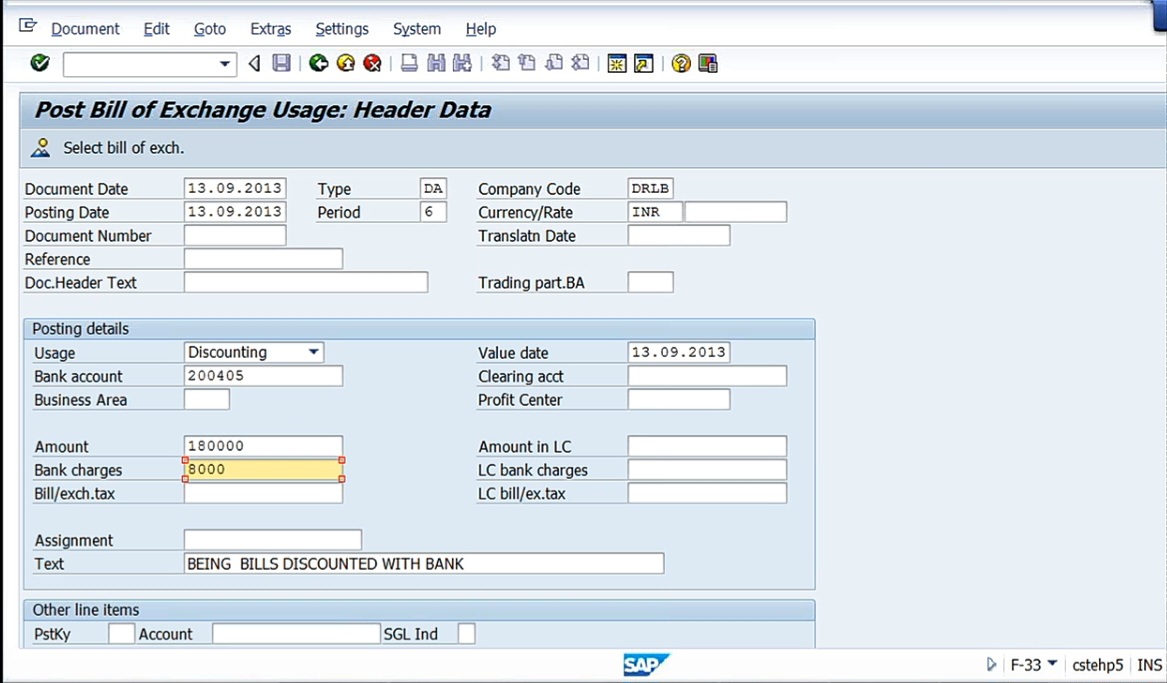

First one, we have made the sale. Second one, we have received bills of exchange. And third one, now what are the bill of exchange that I have received that I want to discount at the bank. Go here, F-33 discounting.

I’m going to discount it to the bank. Same date. Today’s date only, I’m discounting it with bank. Or I can do it tomorrow also. Now what we do, we ask the banker. We have a bill of rupees 1 lakh 88,000. Right? I want to discount it. How much you are going to charge? Say for our sake of this one, you say discounting, bank account, 20405 amount. So what that fellow will give us? Okay. You’re we are going to charge this much of discount charges. And he’ll communicate us or they’ll give a list to us so that we can take. Since for the sake of, say, a round figure, what I will do anyway, we have 1 lakh 88,000. Amount received is, say, 1 lakh 80,000 we have received and 8,000 8,000 we are, taking it as bank charges Being bills discounted with bank. Right? 1 lakh 80,000 amount received. 8,000 bank charges. Once you do this, select bills of exchange. And what is the bills of exchange document number? 14 lakh 6. So here, there is no question of drilling down and picking up. Here, we have to give externally the bills of exchange whatever the document number we have used for the purpose of receiving the bills of exchange, that document number you have to give here because that is the document through which we have received the bills of exchange. So that’s why this is the bill of exchange number. This I am going to discount it. Just queue it, that’s all, then save it or go to document, then simulate.

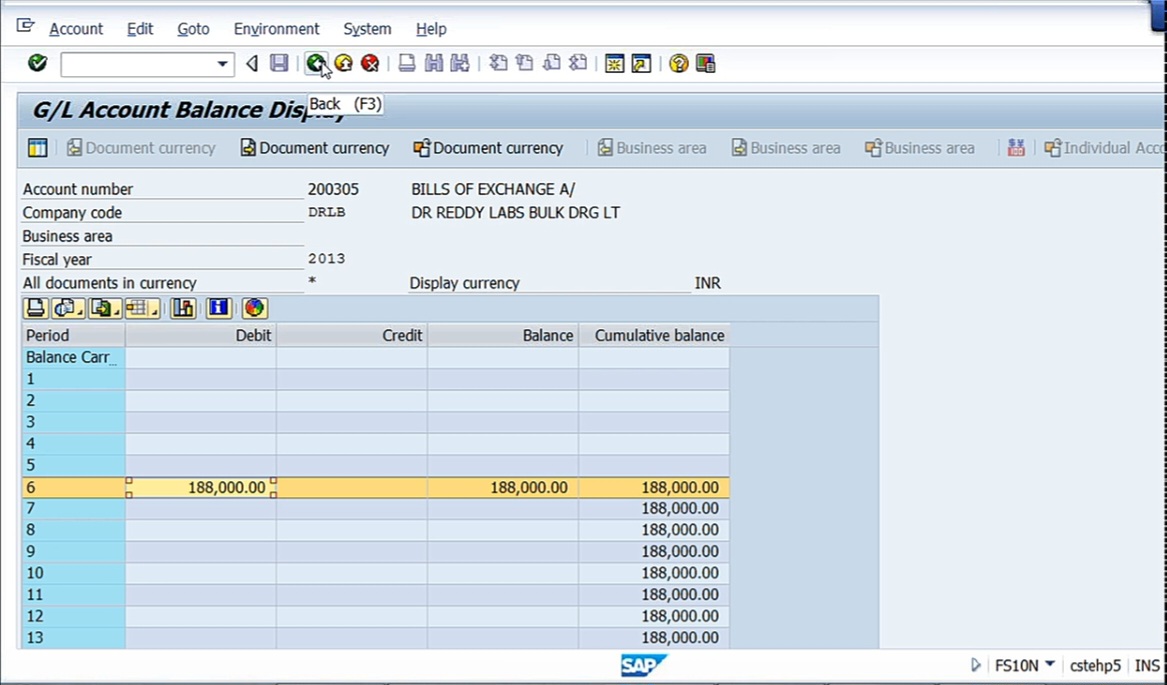

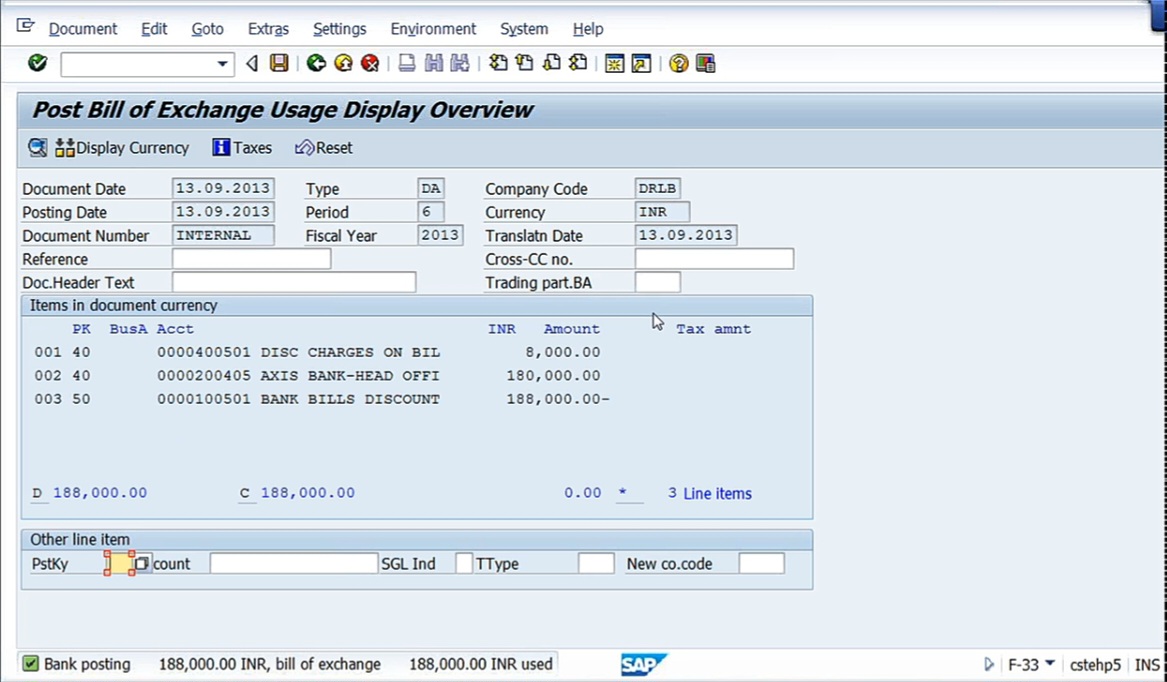

See. I have not posted any entry. What I have done, I have given only 8,000 bank charges and 1 lakh 80. I told the system I have received, that too I put it in the field.. System by default has taken discount charges, debit, 40. Axis Bank because amount received from the bank, debit, 40. Credit has gone to bank bills discount account. How this happened is because we have given the configuration in Define Bank Subaccounts, all the GL accounts have been linked here. So bank bills discounting account we have given. Bank account we have given. So everything system picks here. Now, previously, we have received bills of exchange account that is current asset that is showing as an asset. Now, equivalent amount we are showing liability. So now, even though, if the banker is going to receive the amount after 45 days, I need to continue until that bill has been honored by the customer and the banker is going to receive the payment. We have to continue to show that one side current asset, other side liability to bank. This is the shrewd way of making the accounting, because what are the liabilities that you have, that you have to show as a liability in the balance sheet. If you don’t show liability and simply subsequently at the end of the period that fellow dishonors. In such case, our reflection of accounting is wrong because any liability that is there, there may be continued liability everything, that should be reflected in your financial statements. Otherwise, even statutory auditors will not accept unless you show the liability. All this is nothing but as per the accounting principles. Now let me save it. So bank account is received, discount charges has been debited and, bank bills discounting account is showing liability. So go to FS10N. Say, 100501.

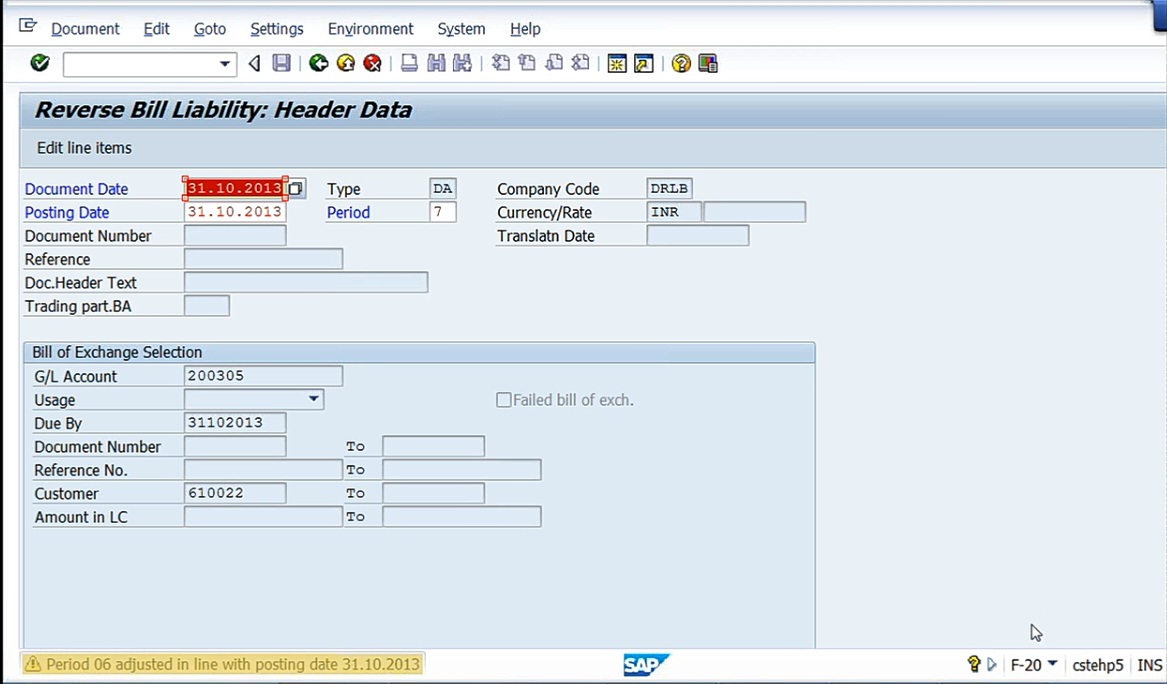

188,000 bank bills discounting account. It’s showing liability. So now the process is over. We have received amount from the bank and discount charges have been paid. So now I need to wait until 45 days on the due date that is 31st October. Right, what we do, we get a letter from the banker. There’s a standard format will be there. So that format will be sent by the banker to the company. So and so bill of exchange has been honored by the customer that we have received, this is for your information. In case it is dishonored, this amount has been the bill has been dishonored and we request you to make the payment arrangements. Like that, they’ll send it. So let us imagine that in our case, right amount has been paid by the customer to the bank, and we have received a communication stating that they have received it. In such a case, what I need to do is reverse the contingent liability.

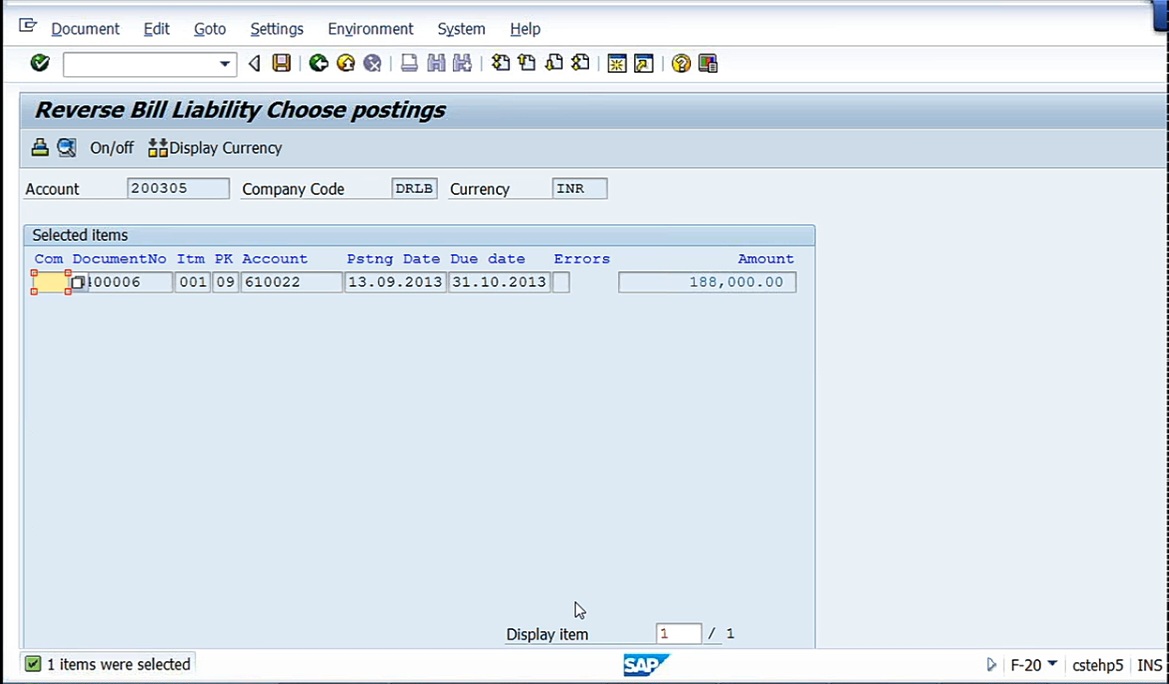

So on the due date, that is 31st October, Document DA, that’s customer document. Company code. GL account. So what is a GL account we are going to reverse the continued liability? Bills of exchange account. So bills of exchange is the account and nothing but 200305. System gives a message ‘Period 6 adjusted in line with posting date 31.10.2013’. No worries, press Enter. Second one, ‘Check – document date is in the future’. No worries, press Enter again. ‘“Due by” date is in future’, press Enter.

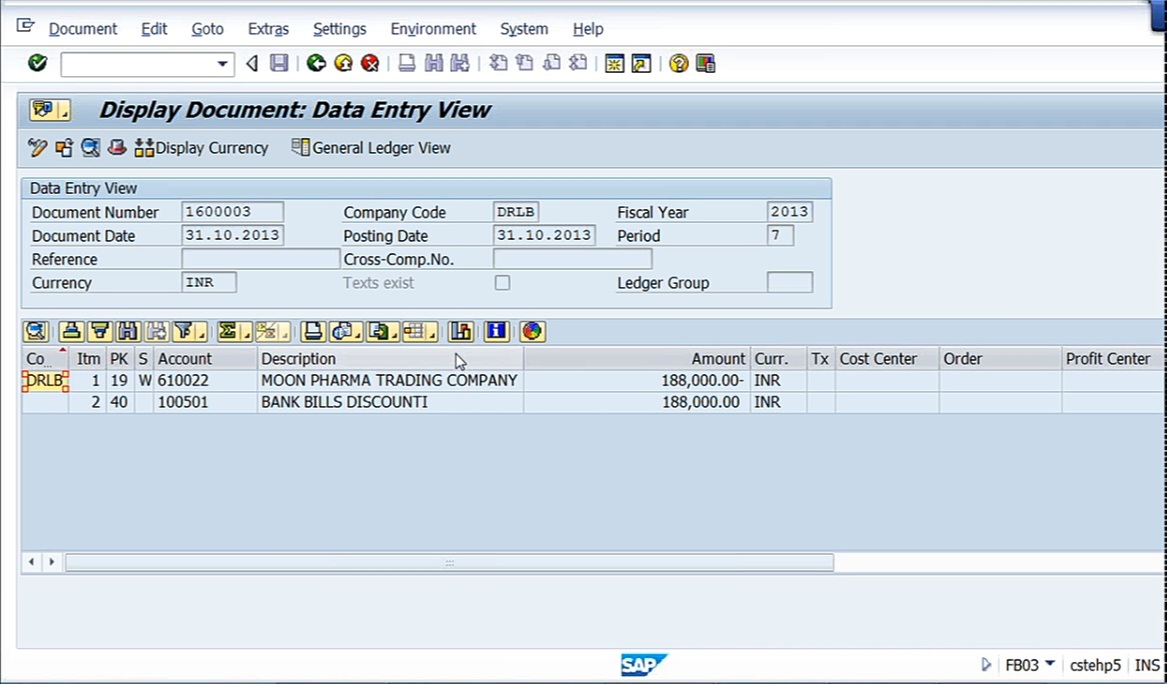

Right. So here system is showing 1 lakh 88,000, contingent liability is going to be reversed. Just save it now. Simply save. Document 16 lakhs3 has been posted. Now see the document.

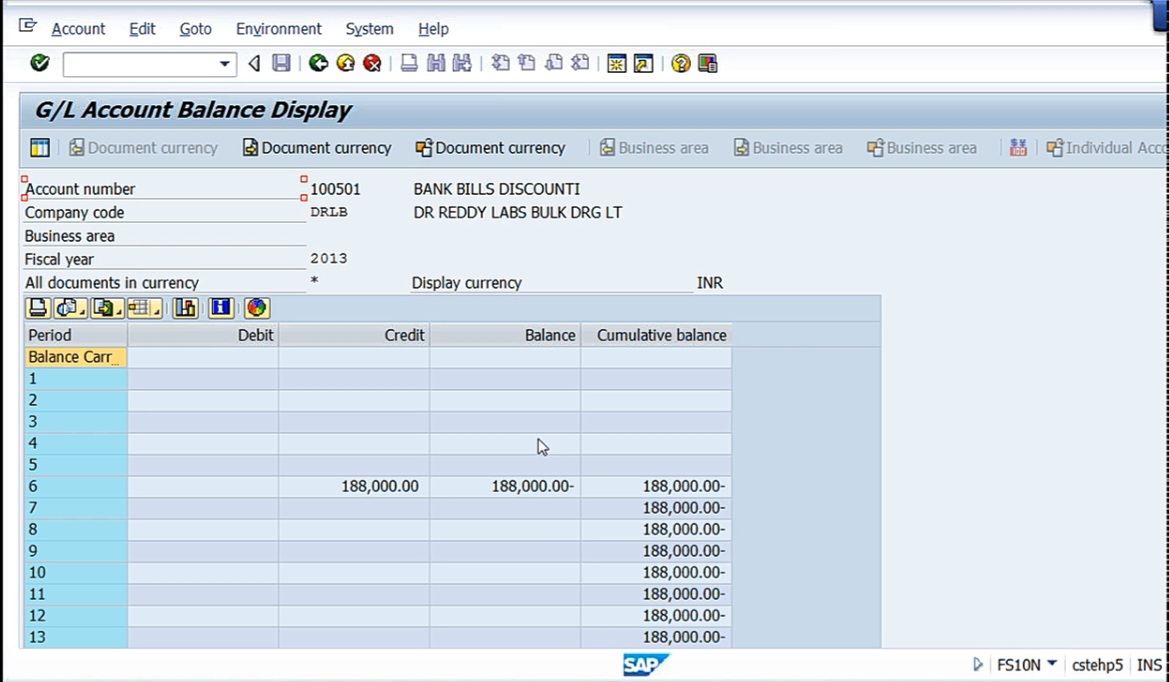

So here, Moon Pharma Trading Company account is credited, and bank bills discounting account is debited. Here, Moon Pharma account is credited why? Because Moon Pharma and here the recon account is going to be bills of exchange. See bills of exchange account, Recon account is bills of exchange, bank bills discounting account. Because when payment is received by the bank, we need to reverse the contingent liability entry. So bank bills discounting account is debited. So bank bills discounting account 1 lakh 88, Debit 40 and customer account with bills of exchange should be credited. Because that bill of exchange is showing as a current asset, now we have to nullify it, means credit it. Bank bills of discounting account we are showing as a liability. That’s why that is now reversed it, that is shown as credit. Now it is being debited. So now this account will get nullified. If you see the GL account, FS10N, 100501 is, on the due date. So we have posted on 31st on 31st, 1 lakh 88,000 we have posted. Ultimately, the balance is nil because outstanding amount by September 30th, it was this much and on 31st October, we have nullified it. Closed balance, cumulative balance is going to be nil now.

So like this, this is credit first debit. And similarly, bills of exchange you check. 200305. Same. Previous date was debit. now it is credited. Balance, cumulative balance is nil.

So like this, first, we need to understand the business scenario, then map the requirements into the SAP system for configuration, then follow the business process. That will give you the result. So to sum up configuration in the entries,. FS00, creation of GL accounts, OBYN, OBYH, OBYK. In OBYN, recon account and that is the bills of exchange account is linked to each other. OBYH, bank charges. OBYK, bank subaccounts we have linked. Then business process entries, F-22, generation of invoice, F-36, receipt of bills of exchange, F-33, we have discounted the bill, F-20, we reverse the contingent liability. So these are the entries and business processes. Again, if you have to, here the important points are nothing but you need to understand the accounting entries very clearly. Next coming is mapping of these requirements. The 3 configuration set whatever we have done, that you need to understand with reference to the resultant entries because the resultant entries we want like that. So that’s why that configuration has been done.

So next topic is dunning. Here, dunning is nothing but see, dunning is in fact a German word. To dun means to remind. So here what we’ll do is that, see every company whenever any outstanding amount is there, that will be sending the reminder letters to the customers. See, it is not our responsibility to send the reminder letters. But, anyway, unless you remind them, they may not be making payment. So that’s why what we do, we generate reminder letters. Generating reminder letters may not be that much difficult because you have an outstanding amount of the party shown with us in the customer account. And, anyway, we have the system, and we are going to generate a letter stating that since, ‘dear customer, your account in our books of accounts is showing an outstanding amount of so and so, which is overdue, we request you to make the payment at their least. In case, if you have already made the payment in the meantime, please disregard this letter.’ Like that, very courteously, we write a letter. First time, we have not received the payment for the letter which we have sent the first time. Second time, what we write, ‘dear customer, we have already sent a reminder letter to you. Please make the payment without any further delay.’ Third letter, ‘dear customer, in spite of 2 reminders, we did not get any payment from your side. We request you to make the payment immediately without fail. Otherwise, we are going to charge interest at the rate of, say, 18%.’ Like that. Fourth letter, you can imagine, it will be maybe very harsh letter. So like that, I can even generate a legal notice also from this. Since I’m generating this letter, I am incurring costs, time of my clerk, I’m going to send it by courier. So like that, so many things are there. I can even charge certain amount also for generating the letter, etc. So all these parameters, we can configure it. But system here, it picks up only the overdue items. All I say, if one party is having, say, around 10 line items, out of that only 5 line items are due, other things are not due. In such case, system will pick up only those amount that are due and generate the reminder letter. Once we generate the letter, we take a printout of reminder letter one plus one and send one of it to the customer, one to the sales officer. Like that. And sometimes you may charge even charges also. Since they are doing their late payment, I may be charging maybe some 1% or say 100 rupees or 500 rupees or 400 rupees, some fixed amount, we can keep it.